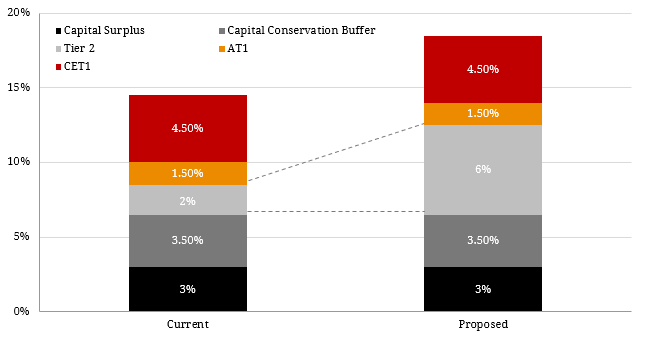

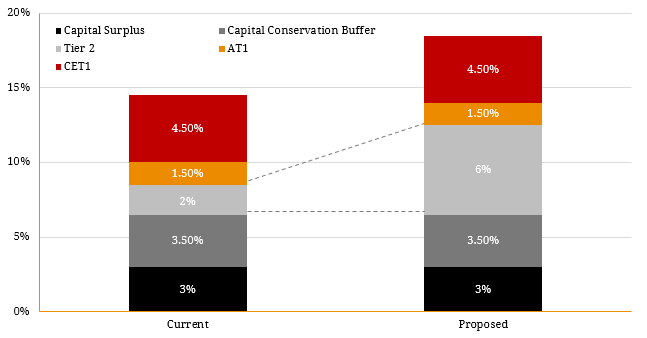

On 8 November 2018, the Australian Prudential Regulatory Authority (APRA) announced its long-awaited proposal (a discussion paper) on Increasing the loss-absorbing capacity of ADIs to support orderly resolution. We previously discussed what the proposed changes could be as far back as April 2017, when we looked at the potential for “Tier 3” regulatory capital introduction in Australia. To the rest of the world and most domestic credit analysts, the topics covered in APRA’s latest release constitute the local implementation of the (G20) Financial Stability Board’s (FSB) Total Loss-absorbing Capacity (TLAC) standard. The November 2015 FSB standard applies to global systemically important banks (G-SIBs) only, although many regulatory authorities have either adopted it without having any G-SIBs or have additionally applied the principles through to domestic SIBs (D-SIBs). As we discussed in June 2018, and as directed by the Financial System Inquiry’s (FSI) recommendation (December 2014), APRA has finally found the time to look to “implement a framework for minimum loss-absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions (ADIs) and minimise taxpayer support”. This was recommendation #3 of 44, highlighting how important it is and with the first two already done. Without going into too much detail, APRA’s discussion paper outlined its proposed or preferred approach to be for the major banks (ANZ, CBA, NAB & WBC) to hold a Total Capital ratio of around 19% (see figure 1) by 2023. Figure 1. Proposed Regulatory Capital for Domestic Systematically-Important Banks (D-SIBs)  Source: BondAdviser, APRA This follows a lot of the heavy-lifting that local banks have already done to meet the regulator’s 10.50% CET1 (Common Equity Tier 1) target to become “unquestionably strong”. This was FSI recommendation #1. As figure 1 shows, a major (one of the four Australian D-SIB) bank’s capital structure is rather complex and APRA did not wish to further complicate it with the addition of a third debt class (Tier 3), nor did it want to legislate or change senior unsecured bonds to bail-in status. This is a marked divergence to other regulatory regimes, but somewhat understandable given Australia’s large and critical dependence on foreign capital, channelled through the banks. Given the proposal, APRA expects each bank to increase its Total Capital ratio by 4-5% with the majority of funding assumed to be via new Tier 2 issuance but noting that any loss-absorbing capital (CET1 and Additional Tier 1 [AT1 or hybrids]) will qualify. This clearly means that senior unsecured debt will not qualify (which was an option if a statutory route was chosen). We believe that APRA has just laid the icing on the cake that is Australian hybrids and we outline some of the key reasons why in table 1 below. Figure 2. Why APRA’s Proposed Changes are Supportive to Australian Hybrids

Source: BondAdviser, APRA This follows a lot of the heavy-lifting that local banks have already done to meet the regulator’s 10.50% CET1 (Common Equity Tier 1) target to become “unquestionably strong”. This was FSI recommendation #1. As figure 1 shows, a major (one of the four Australian D-SIB) bank’s capital structure is rather complex and APRA did not wish to further complicate it with the addition of a third debt class (Tier 3), nor did it want to legislate or change senior unsecured bonds to bail-in status. This is a marked divergence to other regulatory regimes, but somewhat understandable given Australia’s large and critical dependence on foreign capital, channelled through the banks. Given the proposal, APRA expects each bank to increase its Total Capital ratio by 4-5% with the majority of funding assumed to be via new Tier 2 issuance but noting that any loss-absorbing capital (CET1 and Additional Tier 1 [AT1 or hybrids]) will qualify. This clearly means that senior unsecured debt will not qualify (which was an option if a statutory route was chosen). We believe that APRA has just laid the icing on the cake that is Australian hybrids and we outline some of the key reasons why in table 1 below. Figure 2. Why APRA’s Proposed Changes are Supportive to Australian Hybrids  Overall, we believe APRA is still trying to do the right thing but may not perhaps be doing it quite right in preferencing a Tier 2 solution. Whilst the proposed reforms are likely to require some tweaking following expected pushback from key stakeholders (i.e. the banks) and we still anticipate that we may see Tier 3 capital as the preferred method in the final legislation. However, APRA’s proposal would certainly provide benefits to Australian retirees holding hybrids in their portfolios. Strategic and tactical analysis of the TLAC reforms is covered within our November 2018 BondAdviser Monthly Market Review for BondAdviser subscribers. Users can always contact us for more detailed impacts and relative value analysis on a pre- and post-tax basis.

Overall, we believe APRA is still trying to do the right thing but may not perhaps be doing it quite right in preferencing a Tier 2 solution. Whilst the proposed reforms are likely to require some tweaking following expected pushback from key stakeholders (i.e. the banks) and we still anticipate that we may see Tier 3 capital as the preferred method in the final legislation. However, APRA’s proposal would certainly provide benefits to Australian retirees holding hybrids in their portfolios. Strategic and tactical analysis of the TLAC reforms is covered within our November 2018 BondAdviser Monthly Market Review for BondAdviser subscribers. Users can always contact us for more detailed impacts and relative value analysis on a pre- and post-tax basis.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.