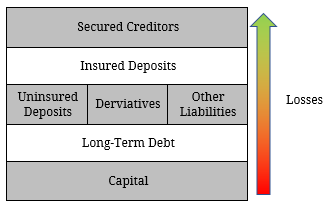

Over the past decade, banking regulation has evolved immensely. In response to the Global Financial Crisis (GFC), the Financial Stability Board (FSB – an international body that monitors and makes recommendations about the global financial system) fine-tuned the criteria for what constitutes a Global Systemically Important Bank (G-SIBs) to avoid the severe moral hazard (i.e. too big to fail) that resulted in some of the largest tax-payer bailouts ever seen. As part of these reforms, the FSB established minimum requirements for Total Loss-Absorbing Capacity (TLAC) in an attempt to reduce the global banking system’s reliance on government assistance. Figure 1. Bank Loss Absorbency  Source: BondAdviser Under these guidelines, capital is to be held in addition to requirements set by the Basel Committee on Banking Supervision (BCBS). Basel III Rules require banks to meet a minimum total capital ratio of 10.5% by 2019 (though in some jurisdictions the minimum ratio is far higher) and is proposed to increase to 16 – 20% under TLAC. The phase-in period will begin in 2019 at 16% and increase to 18% by 2022. TLAC qualifying instruments comprise essentially all capital instruments and other long-term debt that can be written down or converted into equity (bail-in). Debt must be unsecured, have a tenor longer than 1 year, contractual and subordinated to ineligible obligations (typically liabilities that cannot be written down or converted without resulting in significant legal implications). As a result, there has been obvious funding implications for G-SIBs with a clear incentive to work towards the new requirements in the most cost-efficient manner. For example, US banks have been issuing senior debt with call features one year before maturity. This allows for early redemption before the instruments lose their TLAC eligibility and as a result, the bank can cut interest costs for debt with no regulatory value. On the other hand, European countries such as France and Spain have legally adopted a lower-cost Tier 3 debt class option known as “Non-Preferred Senior Debt” late last year. While no Australian bank has been designated as a G-SIB, the four major banks have been classified as being domestic systemically important banks (D-SIB). If APRA adopts the current Basel Committee proposal for the minimum level of TLAC to be 16% (from 1 Jan 2019) of RWA and that the 2.5% Capital Conservation Buffer and the 1.0% D-SIB surcharge will mean that the D-SIBS will be required to hold a minimum of 19.5% of eligible capital. Similarly, from 1 Jan 2022 the minimum eligible capital is currently being proposed to increase to 21.5% of RWA. As a result, if the four major banks were to comply with the proposed comparable standards under a TLAC scenario, additional loss absorbing capital of ~$15 billion would have to be raised by each of the four major banks annually to be compliant by the start of 2019. This is mathematically within reach considering the major banks currently issue around $30 billion of debt p.a. What is not clear, at the moment, is how the banks would (either be required by APRA or determined internally) ‘tweak’ their funding requirements to make up for this shortfall. Domestically, 2017 is shaping up as a low-level issuance year in the ASX listed AT1 market but there is a reasonably high probability that the banks issue out of cycle (potentially to raise additional loss absorbing capital ahead of TLAC implementation). Of the major banks, Only the $1.3 billion ANZ Convertible Preference Shares 3 (ASX: ANZPC) are expected to be called on 1 September (Figure 3). Similarly, among the regional banks only the $268.9 million Bendigo Convertible Preference Shares (ASX: BENPD) and $560 million Suncorp Convertible preference Shares II (ASX: SUNPC) are due to be called on 13 and 17 December 2017. At present, the four major banks have a combined loss absorbing AT1 hybrid and Tier 2 capital amount of ~$60 billion, so it is unlikely capital markets would be able to absorb the required additional TLAC issuance solely via the AT1 & Tier 2 markets over the next 3-5 years. With its US$1 billion issue in May 2016, ANZ opened up the offshore AT1 market for Australian banks. Another source of funding may also present itself to the major banks if APRA were to follow the lead of France & Spain by opening up the Tier 3 debt class option. Figure 2. New European Bank Creditor Hierarchy

Source: BondAdviser Under these guidelines, capital is to be held in addition to requirements set by the Basel Committee on Banking Supervision (BCBS). Basel III Rules require banks to meet a minimum total capital ratio of 10.5% by 2019 (though in some jurisdictions the minimum ratio is far higher) and is proposed to increase to 16 – 20% under TLAC. The phase-in period will begin in 2019 at 16% and increase to 18% by 2022. TLAC qualifying instruments comprise essentially all capital instruments and other long-term debt that can be written down or converted into equity (bail-in). Debt must be unsecured, have a tenor longer than 1 year, contractual and subordinated to ineligible obligations (typically liabilities that cannot be written down or converted without resulting in significant legal implications). As a result, there has been obvious funding implications for G-SIBs with a clear incentive to work towards the new requirements in the most cost-efficient manner. For example, US banks have been issuing senior debt with call features one year before maturity. This allows for early redemption before the instruments lose their TLAC eligibility and as a result, the bank can cut interest costs for debt with no regulatory value. On the other hand, European countries such as France and Spain have legally adopted a lower-cost Tier 3 debt class option known as “Non-Preferred Senior Debt” late last year. While no Australian bank has been designated as a G-SIB, the four major banks have been classified as being domestic systemically important banks (D-SIB). If APRA adopts the current Basel Committee proposal for the minimum level of TLAC to be 16% (from 1 Jan 2019) of RWA and that the 2.5% Capital Conservation Buffer and the 1.0% D-SIB surcharge will mean that the D-SIBS will be required to hold a minimum of 19.5% of eligible capital. Similarly, from 1 Jan 2022 the minimum eligible capital is currently being proposed to increase to 21.5% of RWA. As a result, if the four major banks were to comply with the proposed comparable standards under a TLAC scenario, additional loss absorbing capital of ~$15 billion would have to be raised by each of the four major banks annually to be compliant by the start of 2019. This is mathematically within reach considering the major banks currently issue around $30 billion of debt p.a. What is not clear, at the moment, is how the banks would (either be required by APRA or determined internally) ‘tweak’ their funding requirements to make up for this shortfall. Domestically, 2017 is shaping up as a low-level issuance year in the ASX listed AT1 market but there is a reasonably high probability that the banks issue out of cycle (potentially to raise additional loss absorbing capital ahead of TLAC implementation). Of the major banks, Only the $1.3 billion ANZ Convertible Preference Shares 3 (ASX: ANZPC) are expected to be called on 1 September (Figure 3). Similarly, among the regional banks only the $268.9 million Bendigo Convertible Preference Shares (ASX: BENPD) and $560 million Suncorp Convertible preference Shares II (ASX: SUNPC) are due to be called on 13 and 17 December 2017. At present, the four major banks have a combined loss absorbing AT1 hybrid and Tier 2 capital amount of ~$60 billion, so it is unlikely capital markets would be able to absorb the required additional TLAC issuance solely via the AT1 & Tier 2 markets over the next 3-5 years. With its US$1 billion issue in May 2016, ANZ opened up the offshore AT1 market for Australian banks. Another source of funding may also present itself to the major banks if APRA were to follow the lead of France & Spain by opening up the Tier 3 debt class option. Figure 2. New European Bank Creditor Hierarchy  Source: BondAdviser In theory, Tier 3 debt would sit between traditional senior debt and Tier 2 (subordinated) debt in the capital structure. The issue with Tier 3 debt would be whether there is sufficient institutional demand to meet supply. The more conservative buyers of traditional senior debt would be reluctant to move down the capital structure even for the yield pick-up, and even if some did it would not be in the same volume as that for senior debt. The fact that total Tier 2 debt of the major banks is ~$20 billion clearly shows this as Tier 3 debt will most likely be bought by the same group of investors that currently buy Tier 2 securities. With limited issuance in the listed hybrid market, investors still remain starved for new product and has resulted in most new issues being oversubscribed. This suggests that if implemented, markets could have the appetite to absorb more debt subject to the technicalities of the new asset class.

Source: BondAdviser In theory, Tier 3 debt would sit between traditional senior debt and Tier 2 (subordinated) debt in the capital structure. The issue with Tier 3 debt would be whether there is sufficient institutional demand to meet supply. The more conservative buyers of traditional senior debt would be reluctant to move down the capital structure even for the yield pick-up, and even if some did it would not be in the same volume as that for senior debt. The fact that total Tier 2 debt of the major banks is ~$20 billion clearly shows this as Tier 3 debt will most likely be bought by the same group of investors that currently buy Tier 2 securities. With limited issuance in the listed hybrid market, investors still remain starved for new product and has resulted in most new issues being oversubscribed. This suggests that if implemented, markets could have the appetite to absorb more debt subject to the technicalities of the new asset class.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.