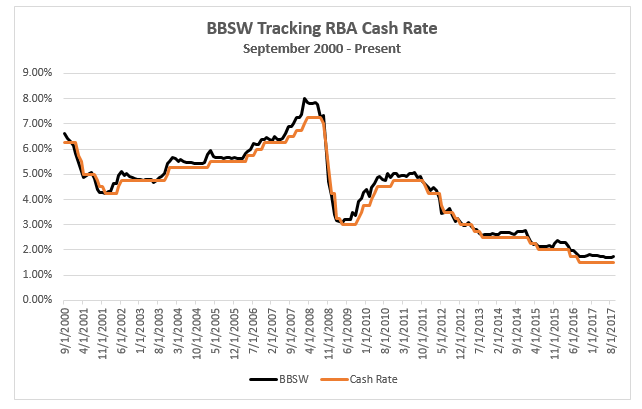

In July 2017, the UK financial regulator, the Financial Conduct Authority (FCA), which regulates LIBOR, announced that the global base rate would be phased out over the next four years, ending in 2021. Although it is unclear what will replace it. The London Interbank Offer Rate, LIBOR, is the benchmark interest rate that many of the largest banks in the world charge one another for loans. It underlies an estimated $350 trillion in debt and debt-related derivatives worldwide, including everything from mortgages to corporate loans to student debt. Two main developments since the crisis of 2008–09 motivated the FCA to end LIBOR’s use. The first was a scandal revealed in 2014 in which traders at several large banks were found to be manipulating LIBOR rates to benefit their own trading positions and therefore, their bonuses. This resulted in regulators in the US and UK fining the banks involved billions of dollars and securing a jail sentence for one former trader. The second was the decline in wholesale interbank lending in the post-crisis years with fewer real transactions on which to evidence the benchmark rate (i.e. less observable real market data points). As a result, LIBOR becomes more and more dependent on expert guidance — that is, submissions by bank traders. This is not sustainable in the long run since, in practice, only some of the returns are derived on real underlying transactions, and the rest are left up to traders’ estimates. In 2015, for example, only around 30% of submissions were from genuine contracts. In Australia, the equivalent of LIBOR is the Bank Bill Swap Rate (BBSW) which is the primary short-term rate used in domestic financial markets for the pricing and valuation of Australian dollar securities including floating rate bonds and other financial floating rate instruments, such as hybrids. The BBSW typically tracks close to the official RBA cash rate (Figure 1), although it can also be impacted by many other factors, including alleged manipulation by some major banks in Australia – ASIC is still pursuing ANZ, Westpac and NAB in the Federal Court over alleged rigging of the BBSW in 2010, similar to the LIBOR case. Figure 1. BBSW v RBA Cash Rate  Source: RBA, Bloomberg Following the BBSW-rigging scandal, reforms to the way the BBSW is calculated were first implemented in 2013 and under the current method the rate is based on actual trades of negotiable certificates of deposit and bank accepted bills during a daily trading “window’’. However, despite an increase in the amount of paper on issue, trading has dried up significantly and there are days where none actually occurs. This low turnover raises the risk that market players would be less willing to use the reference rate in other transactions. Among the changes being considered by the Council of Financial Regulators is broadening the market for transactions beyond the banks to include investment funds and treasury corporations, and shifting to a volume-weighted average price for trades to set the market price. Effective 1 January 2017, the ASX became the new BBSW rate administrator, replacing AFMA. In late 2017, the ASX intends to introduce a new BBSW calculation methodology utilising a volume weighted average price (VWAP) calculation as the primary calculation method. The change in methodology implements the recommendation of the Council of Financial Regulators and reflects a needed evolution of market practice. In the future, could we possibly use a rate based on an overnight secured lending (against Commonwealth Treasuries) rate similar to the US (being used by a panel of 15 US banks) or some other benchmark entirely? Whichever is chosen, we are almost certain that the benchmark rate will offer greater visibility and transparency, with less room for manipulation. This of course benefits end investors most of all.

Source: RBA, Bloomberg Following the BBSW-rigging scandal, reforms to the way the BBSW is calculated were first implemented in 2013 and under the current method the rate is based on actual trades of negotiable certificates of deposit and bank accepted bills during a daily trading “window’’. However, despite an increase in the amount of paper on issue, trading has dried up significantly and there are days where none actually occurs. This low turnover raises the risk that market players would be less willing to use the reference rate in other transactions. Among the changes being considered by the Council of Financial Regulators is broadening the market for transactions beyond the banks to include investment funds and treasury corporations, and shifting to a volume-weighted average price for trades to set the market price. Effective 1 January 2017, the ASX became the new BBSW rate administrator, replacing AFMA. In late 2017, the ASX intends to introduce a new BBSW calculation methodology utilising a volume weighted average price (VWAP) calculation as the primary calculation method. The change in methodology implements the recommendation of the Council of Financial Regulators and reflects a needed evolution of market practice. In the future, could we possibly use a rate based on an overnight secured lending (against Commonwealth Treasuries) rate similar to the US (being used by a panel of 15 US banks) or some other benchmark entirely? Whichever is chosen, we are almost certain that the benchmark rate will offer greater visibility and transparency, with less room for manipulation. This of course benefits end investors most of all.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.