With ~$4.7 billion of net issuance of ASX-listed debt and hybrid securities in 2016, investors have not been short of supply but with three large-scale hybrids due for redemption before years end, where will this maturing capital go? Figure 1. 2016 Transactions

| Date | Ticker | Issuance ($m) | Replaced ($m) | Net Issuance ($m) |

| 30-Mar-16 | CBAPE | $1,450 | PCAPA – $1166 | $284 |

| 7-Jun-16 | PPCHA | $100 | PPCG – $50 | $50 |

| 7-Jun-16 | NABPD | $1,500 | N/A | $1,500 |

| 30-Jun-16 | WBCPG | $1,700 | WCTPA – $763 | $937 |

| 5-Oct-16 | QUBHA | $305 | N/A | $305 |

| 27-Sep-16 | ANZPG | $1,622 | N/A | $1,622 |

| Total: $4,698 |

Figure 2. 2016 Scheduled Redemptions

| Date | Ticker | Redemption Amount ($m) |

| 24-Nov-16 | WOWHC | $700 |

| 15-Dec-16 | ANZPA | $1,969 |

| 22-Dec-16 | ORGHA | $900 |

| Total: $3,569 |

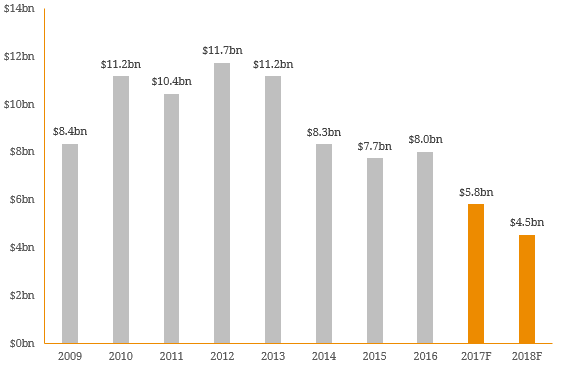

Source: BondAdviser Given hybrid investors have been spoilt by a new AT1 hybrid by each of the four major banks, we expect the market will easily absorb the redemptions in November and December 2016 (Note half of ANZPA has been rolled into the new ANZPG issue). However, with two of the larger non-financial corporate hybrids (namely WOWHC and ORGHA) being redeemed, investment options outside the Australian banking sector appear limited. Following these redemptions, the non-financial corporate hybrid market will be at its smallest since 2010. This market will contract further if there is no new issuance in 2017 as TAHHB, CTXHA and GMPPA are scheduled to reach their call/reset dates. Figure 3. Non-Financial Corporate Hybrid Market Size  Source: BondAdviser, ASX There is a positive argument for non-financial corporate hybrids at present as we expect a large proportion of redemptions will be reinvested in non-financial industries. Given the average trading margin has widened significantly since August, this may represent a potential buying opportunity. Although it is possible that the capital from ORGHA and WOWHC may be reinvested into bank hybrids, non-financial hybrids are becoming relatively cheaper (see Figure 4) and investors may choose to remain in these securities due to the lack of current and future corporate hybrid issuance. Figure 4. Non-Financial Corporate Hybrid v AT1 Bank Hybrid Average Trading Margin

Source: BondAdviser, ASX There is a positive argument for non-financial corporate hybrids at present as we expect a large proportion of redemptions will be reinvested in non-financial industries. Given the average trading margin has widened significantly since August, this may represent a potential buying opportunity. Although it is possible that the capital from ORGHA and WOWHC may be reinvested into bank hybrids, non-financial hybrids are becoming relatively cheaper (see Figure 4) and investors may choose to remain in these securities due to the lack of current and future corporate hybrid issuance. Figure 4. Non-Financial Corporate Hybrid v AT1 Bank Hybrid Average Trading Margin  Source: BondAdviser Overall, the ASX-listed debt and hybrid market continues to be well supported by the low interest rate environment. IPOs are being over-subscribed and scheduled redemptions are only intensifying demand in a relatively small market. The decisions made by Origin and Woolworths show there is no certainty any issuer will roll-over hybrids that reach their call date next year. For this reason we expect 2017 to be a year categorised by demand-side pressure rather than the supply-side pressure we have experienced in 2016.

Source: BondAdviser Overall, the ASX-listed debt and hybrid market continues to be well supported by the low interest rate environment. IPOs are being over-subscribed and scheduled redemptions are only intensifying demand in a relatively small market. The decisions made by Origin and Woolworths show there is no certainty any issuer will roll-over hybrids that reach their call date next year. For this reason we expect 2017 to be a year categorised by demand-side pressure rather than the supply-side pressure we have experienced in 2016.