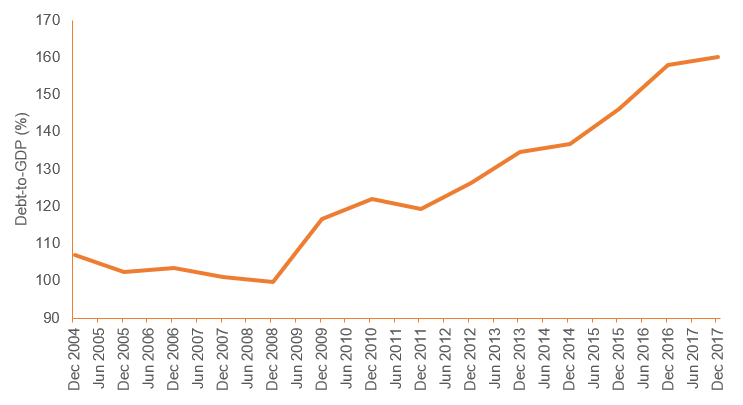

Too much is made of the Reserve Bank of Australia’s (RBA) overnight cash rate and the Federal Funds rate of the U.S Federal Reserve, with market observers not having to search far for diverse and divergent markets commentary and insights. There is comparatively little commentary however, to understanding what a Reserve Requirement Ratio (RRR) is and the arguably equally important function it serves within a country’s economy. The reserve ratio plays a similar role to a central banks interest rate policy – a lowering of the reserve ratio (interest rate) is an action of expansionary monetary policy. The RRR is the portion of depositor’s balances that banks must retain as cash as determined by the country’s central bank and is a useful tool for controlling liquidity in the financial system. Thus, when a countries central bank lowers the reserve ratio, this allows banks to make more loans to consumers and businesses, encouraging investment and providing stimulus to the economy. Saviour to the Chinese economy When the Peoples Bank of China (PBOC) latest RRR cut comes into effect on July 5th, this will mark the third time since the beginning of 2018 that the Central Bank of the world’s second largest economy has utilised this quantitative tool of monetary policy in an effort to deleverage the economy and ease concerns regarding slowing economic growth amid ongoing trade tensions with the US. With China’s credit boom being the primary factor driving global growth for the past decade, a systematic debt (or credit) crisis could have costly implications on both a domestic and global level. Recently, the PBOC announced that it would be lowering this requirement, which is currently 16% for large state-owned and joint-stock commercial banks and 14% for smaller banks including postal savings banks, city commercial banks, non-county rural banks and foreign banks by 50 basis points (0.5%). This decrease released RMB 500 billion ($77 billion USD) in reserves for large banks and RMB 200 billion ($31 billion USD) for their smaller counterparts. The PBOC has encouraged banks to use their newfound liquidity to engage in debt-for-equity swaps, which involves converting loans to corporate entities into equity stakes in the entity itself, serving the purpose of reducing the debt burden of enterprises in an effort to curb the problems arising from China’s unprecedented levels of corporate debt that poses a major threat to financial stability (Figure 1). Figure 1 – Chinese Corporate Debt as a % of GDP

Source: BondAdviser, Bloomberg

Whilst smaller banks may have received a lower dosage of liquidity then their larger counterparts, the use of this cash has the potential to cause greater implications to the economy. This is due to the newly available deposits being used by these smaller institutions to grant loans to small and micro enterprises which struggle to get credit access from mainstream banks as opposed to state-owned enterprises. This emphasises that the central banks’ mission is to make liquidity available to the real economy, not the zombie enterprises (companies that can repay the interest of their obligations, but not the principal) that clog up banking systems and drag on GDP growth. The above is in some contrast to the second RRR adjustment that saw banks benefit from an excess RMB 400 billion after repayments of RMB 900 billion worth of loans acquired through the PBOC’s Medium-term Lending Facility (MLF) pipeline – demonstrating the complexity of issues that the Chinese government faces to ensure financial stability in a rapidly changing population. Implications When delving into the PBOC’s reasoning for RRR adjustments, investors do not need to look too far. China is accelerating towards a record year of corporate bond defaults, with the current default rate of 20 privately owned enterprises (POEs) already comprising 75% of the previous high set in 2016, an alarming statistic given that an anticipated economic slowdown is yet to actually occur. Given the Chinese government’s crackdown on the $10 trillion shadow banking industry – in the form of lending and borrowing that sits outside the regulated banking sector that has greatly reduced property developers and local government financing vehicles to access credit funds, it becomes quite understandable that a reduction in RRRs was a necessary safety measure for the Chinese central bank to take. The cloud of uncertainty lingering over this issue remains – i.e. will this even be enough? With an estimated RMB 3 trillion worth of onshore corporate debt due for repayment next year and a considerable amount more due in the next two years in addition to the compounding effect of an escalating trade war with the US, it would be prudent to think that the PBOC is not done yet and that further RRR cuts are to be expected in the near future.