In our second half outlook, “Where to from here?”, we expected Australian companies to report slightly weaker headline results (revenue) with profits remaining relatively stable for period ending June 2016. We also expected an increasing number of them to favour shareholder friendly measures or turn to acquisitions for growth as organic revenue growth will be difficult during a period sustained low global growth. So what did we learn from reporting season?

- Organic growth is hard to come by

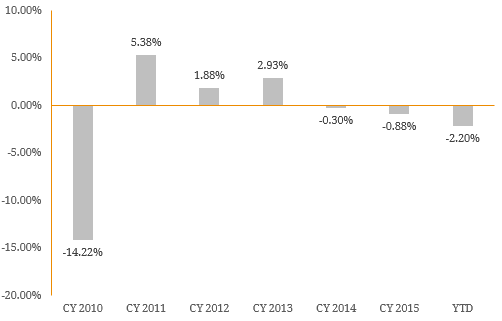

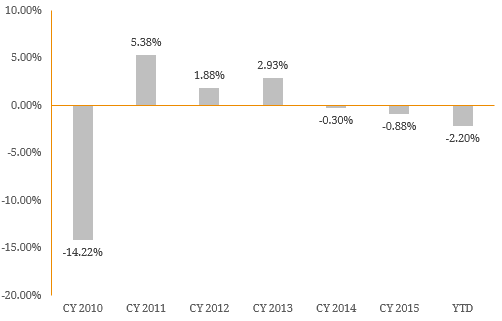

Management used the phrase “challenging trading conditions” many times during reporting season with many expecting a poor operating environment in 2017. As a result, revenue was noticeably weaker across the board and this forced some corporates to seek acquisitions as a source of earnings growth. Figure 1. ASX 200 Revenue Growth (per share basis)  Source: Bloomberg

Source: Bloomberg

- Cost management is in trend

With revenue figures broadly flat, cost management was the common strategy utilised by companies over 2016 to improve the bottom line and cash flow. With low economic growth domestically and abroad, corporates embarked on extensive cost saving activities to ensure profits were maintained or improved. This is allowed many corporates to maintain dividend payments. Figure 2. ASX 200 Cash Flow (per share basis)  Source: Bloomberg

Source: Bloomberg

- Management are more cautious

With diverging global monetary policies, uncertainty in Australia’s economic future and the GFC nostalgia triggered by Brexit, management have become much more risk adverse regarding the balance sheet. Broadly speaking, leverage remains low (relative to pre-GFC) and liquidity is strong.

- Shareholder friendly activities

In the current economic environment, growth opportunities are limited and shareholder friendly measures are being chosen as the alternative. While this is a credit negative, excess cash is usually returned back to equity investors at this point in the cycle. A number of corporates implemented share buy-back programs, increased their payout ratios or distributed special dividends in 2016. Figure 3. ASX 200 Dividend Payout Ratio  Source: Bloomberg

Source: Bloomberg

- Overall, broadly credit neutral

In reporting season, we broadly found results to be credit neutral. This was driven primarily by steady earnings growth, stable credit metrics and strong cashflow across the corporate spectrum. The credit rating agencies shared this view with minimal rating movements across August. Given the uncertainty in global markets, we expect management to retain conservative strategies in 2017 and overall credit should be well supported through the cycle. The primary risk to this thesis is the appetite for asset sales, mergers and acquisitions is high due to the low cost of accessible capital but given what has been revealed in reporting season, we believe this risk is manageable. Figure 4. ASX 200 Return on Capital  Source: Bloomberg

Source: Bloomberg