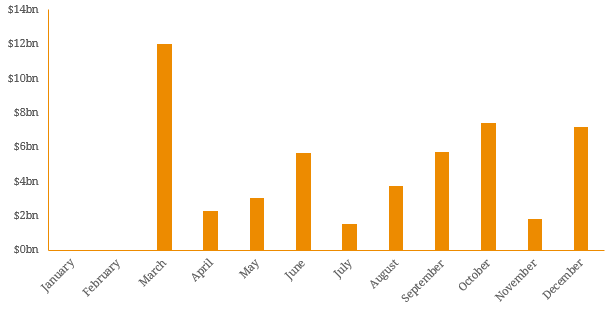

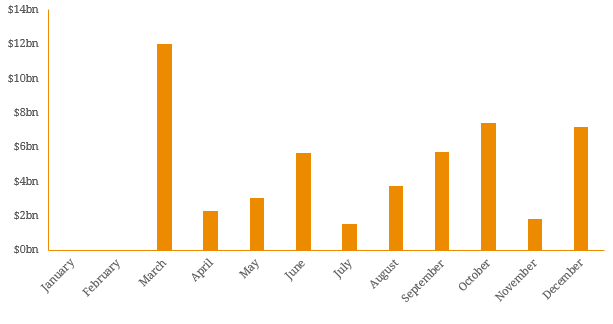

Last week we entered the holiday period which is generally categorised as quiet for all financial markets. So, what can we expect over the next two months before reporting season commences once again in February 2017? As many companies in Australia shut down for the majority of the holiday period, primary market activity is limited. This is especially prominent in the retail market which is considerably smaller than the wholesale over-the-counter market. While activity in the early half of December remains reasonably elevated, January and February are muted in terms of issuance. Given this 2-month issuance drought, it’s no surprise March is the most popular month to issue in. Figure 1. Total Issuance by month of Issue for all ASX-Listed Debt & Hybrid Securities over $50 million since 2009  Source: BondAdviser, ASX *Note: Issuers tend to announce securities to a market 1-2 months before the actual issue date. Utilising the same sample of securities, we can perform the same analysis from a redemption perspective. Notice that the December redemption value is much higher than the December issuance value above. Many ASX-listed debt and hybrid securities are issued with a first short interest period (i.e. less than 90 days or less than 180 days) which allows the underlying issuer to adjust the interest payments schedule for monthly cashflow purposes. This can typically follow the end of quarter schedule (i.e. March, July, September, December) and is one of the major reasons why large redemptions are usually experienced in December. This December is no exception with the Origin Subordinated Notes (ASX: ORGHA) and ANZ Convertible Preferences Shares 2 (ASX: ANZPA) scheduled to be redeemed. However, we note that ANZPA have been pre-funded by ANZ Capital Notes 4 (ASX: ANZPG) and ANZ’s recent USD-denominated hybrid. Figure 2. Total Redemption by month of redemption for all ASX-Listed Debt & Hybrid Securities over $50 million since 2009.

Source: BondAdviser, ASX *Note: Issuers tend to announce securities to a market 1-2 months before the actual issue date. Utilising the same sample of securities, we can perform the same analysis from a redemption perspective. Notice that the December redemption value is much higher than the December issuance value above. Many ASX-listed debt and hybrid securities are issued with a first short interest period (i.e. less than 90 days or less than 180 days) which allows the underlying issuer to adjust the interest payments schedule for monthly cashflow purposes. This can typically follow the end of quarter schedule (i.e. March, July, September, December) and is one of the major reasons why large redemptions are usually experienced in December. This December is no exception with the Origin Subordinated Notes (ASX: ORGHA) and ANZ Convertible Preferences Shares 2 (ASX: ANZPA) scheduled to be redeemed. However, we note that ANZPA have been pre-funded by ANZ Capital Notes 4 (ASX: ANZPG) and ANZ’s recent USD-denominated hybrid. Figure 2. Total Redemption by month of redemption for all ASX-Listed Debt & Hybrid Securities over $50 million since 2009.  Source: BondAdviser, ASX Over on the last 6-7 years’ redemptions have outweighed new issues in December while January has remained muted. But what about overall performance? Figure 3 shows monthly returns since 2009 for ASX-listed hybrid securities. As suspected, net negative supply in December has resulted in strong performance while January has remained flat or underperformed. This is then followed by February where companies tend to release credit sensitive announcements. This was demonstrated this year when hybrid trading margins surged on the back of equity market volatility following a margin compression in December (Figure 4). Figure 3. Monthly Hybrid Security Returns since 2009.

Source: BondAdviser, ASX Over on the last 6-7 years’ redemptions have outweighed new issues in December while January has remained muted. But what about overall performance? Figure 3 shows monthly returns since 2009 for ASX-listed hybrid securities. As suspected, net negative supply in December has resulted in strong performance while January has remained flat or underperformed. This is then followed by February where companies tend to release credit sensitive announcements. This was demonstrated this year when hybrid trading margins surged on the back of equity market volatility following a margin compression in December (Figure 4). Figure 3. Monthly Hybrid Security Returns since 2009.  Source: BondAdviser, Evans & Partners Figure 4. ASX-Listed Hybrid Historical Trading Margins

Source: BondAdviser, Evans & Partners Figure 4. ASX-Listed Hybrid Historical Trading Margins  Source: BondAdviser Based on historical data and current market conditions, we see no reason why trading margins will not compress throughout December and January. Given the data we have analysed, it appears issuers tend to hold back corporate announcements over the holiday period before releasing market sensitive information during reporting season in February. While we do not expect any major deteriorations in credit quality in any companies under our coverage, there can be unanticipated and unpredictable surprises. As a result, a number of undervalued securities can emerge during February and like in 2016 may translate into compelling buying opportunities. This highlights the importance of credit research and proper due diligence when investing in ASX-listed income securities. Overall, we expect history to repeat itself and securities to perform well over the holiday period until reporting season commences. Then it will become a matter of stringent credit research and due diligence to give investors concise investment recommendations going forward into 2017.

Source: BondAdviser Based on historical data and current market conditions, we see no reason why trading margins will not compress throughout December and January. Given the data we have analysed, it appears issuers tend to hold back corporate announcements over the holiday period before releasing market sensitive information during reporting season in February. While we do not expect any major deteriorations in credit quality in any companies under our coverage, there can be unanticipated and unpredictable surprises. As a result, a number of undervalued securities can emerge during February and like in 2016 may translate into compelling buying opportunities. This highlights the importance of credit research and proper due diligence when investing in ASX-listed income securities. Overall, we expect history to repeat itself and securities to perform well over the holiday period until reporting season commences. Then it will become a matter of stringent credit research and due diligence to give investors concise investment recommendations going forward into 2017.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.