In 2017, there are a number of major scheduled call dates and final redemptions in the ASX-listed Debt & Hybrid Market. While it is important to ensure that capital is paid back, many investors require a new investment vehicle to reinvest the repaid funds. For this reason, we have given our thoughts on potential refinancing for major securities scheduled to reach their first call date in the first half of 2017. Although speculative, we hope these views give investors some insight into potential reinvestment options in 2017.

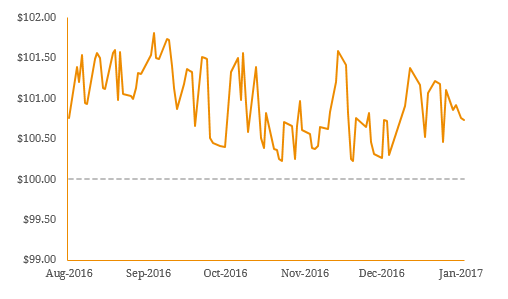

Tabcorp Subordinated Notes (ASX: TAHHB) Call Date: 22nd of March 2017 In October 2016, Tabcorp Holdings (ASX: TAH) and Tatts Group (ASX: TTS) announced they will combine to form a $11.3 billion gambling entertainment group. The transaction has been approved by both boards and is expected to be completed by mid-2017 following shareholder, government and regulatory approvals (ACCC set to announce decision on 23rd of February 2017). The combined group will target a gross debt to EBITDA ratio of 3.0x – 3.5x which implies $3.0 – $3.5 billion of gross debt. As at 30 June 2016, combined gross debt of TAH and TTS equated to ~$2.2 billion and we expect an additional ~$600 – 700 million of debt will be utilised to fund the merger. The merged company intends to maintain an investment grade credit rating. Post implementation, the combined group expects to undertake a $500 million share buyback. Given total cash between the two groups equates to ~$320 million, we expect this will be partially debt funded. As a result, our view is fairly binary as to whether the merger goes ahead or not. As a standalone entity, Tabcorp has sufficient capacity to call the notes from cash and bank facilities ($536 million as at 30 June 2016). However, given the additional debt funding implied to fund the transaction, the proposed share buyback post-merger and the fact that Tabcorp’s credit rating is only one notch above investment-grade, the group may roll the notes into a new hybrid to retain the 50% equity credit treatment if the merger goes ahead. In 2016 a number of new corporate issues were significantly oversubscribed and investors were scaled back to match supply. Given that TAHHB is trading above par value so close to the call date (Figure 1), one explanation could be that investors have the expectation that the notes will be refinanced to support the merged company’s capital management strategy and are getting in early. Figure 1. Tabcorp Capital Price History  Source: BondAdviser

Source: BondAdviser

Colonial Subordinated Notes (ASX: CNGHA) Call Date: 31st of March 2017 In March 2016, APRA announced it had deferred finalising the capital components of the Level 3 framework for conglomerates with industry consultation not expected to occur until mid-2017 at the earliest and implementation no earlier than 2019. The non-capital components were finalised in August 2016 and will take effect on the 1st of July 2017. The Colonial Holding Company Limited (CNG) falls under this framework (wealth management subsidiary of CBA) and therefore, the regulatory capital value of CNGHA is subject to framework adjustments. Given APRA’s implementation time frame (and the March 2017 call date), we now consider the probability of an early redemption (through the trigger of a regulatory event) as improbable. We note that under this condition CNG has the right to redeem the notes for $101.50 plus accrued if APRA implements the proposal. Under the Conglomerate framework, CNGHA will cease to qualify as Level 3 regulatory capital for the consolidated group (Commonwealth Bank of Australia). As the issue size for this security is significant (1 billion), we believe these funds will be refinanced by CBA level to ensure capital levels are maintained. The question is will the new security be refinanced into the over-the-counter (OTC) wholesale market or the ASX-listed retail market? The upfront costs to issue new hybrid capital into the listed market are high relative to the wholesale market. However, these costs are lowered through a reinvestment offer from one security to another. As a result, CBA may preserve the $1 billion in the retail market (for diversity) through the issuance of a new listed security.

NAB & ANZ Subordinated Notes (ASX: ANZHA, NABHB) Call Dates: 18th and 20th of June 2017 While the listed Tier 2 market increased post the Global Financial Crisis (GFC), the ASX has seen limited new issuance in recent years. Due record low interest rates globally, many institutional investors have been forced to invest further down (higher risk) the capital structure into Tier 2 capital securities to meet target returns. As a result of this increased demand, many Australian banks have elected the wholesale (over-the-counter) market as their primary Tier 2 capital funding channel as it subject to lower funding costs and is easier to facilitate. For this reason, wholesale Tier 2 security issuance has increased over the past two years, while the listed Tier 2 market has remained flat. Given this trend, NABHB and ANZHA may be refinanced into new wholesale Tier 2 securities out of reach of retail investors. However, for the same reasons outlined for CNGHA, the banks’ may choose to retain the funds in the retail market (due to upfront costs, funding diversity etc.). Figure 2. Major Bank Tier 2 Market Size: Retail v Wholesale  Source: BondAdviser, Company Reports

Source: BondAdviser, Company Reports