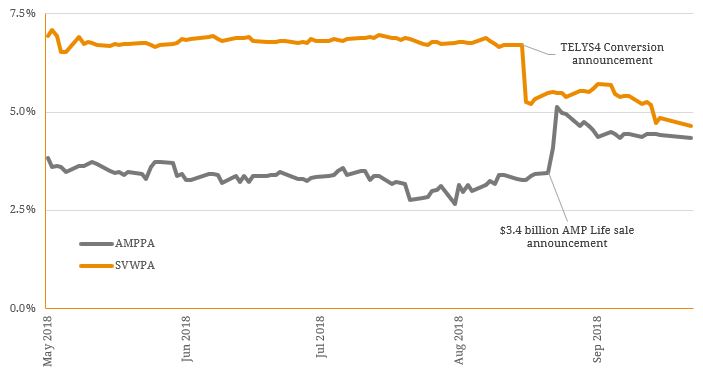

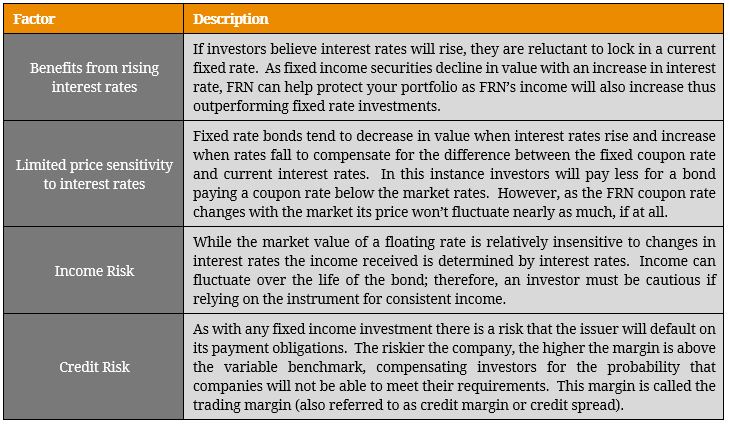

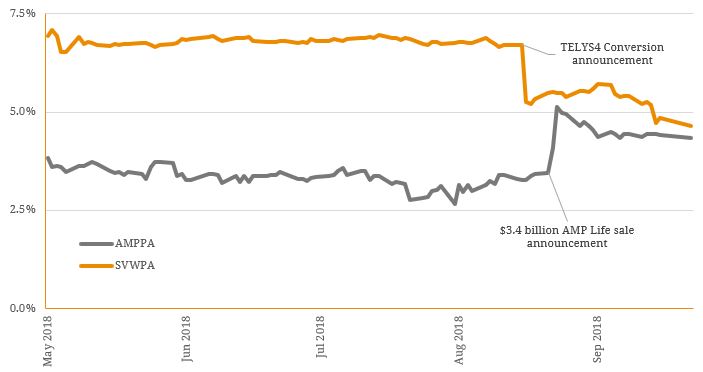

Fixed income instruments come in many different forms, with the most commonly seen in Australia being bonds. The variable and bespoke nature of bonds (by virtue of being traded over-the-counter) implies a great deal of flexibility in terms of seniority, security and income structure. The two most common types of bond payments seen in fixed income markets are fixed rate and floating rate. Investors in fixed rate bonds receive a periodic (i.e. quarterly, annual or semi-annual) payment at a fixed rate of interest (i.e. 7.00%). This interest payment does not ordinarily vary and is set by the issuer at launch date. The coupon rate is most often expressed as a percentage of the bond’s face value (i.e. 7% of $100). In contrast, floating rate notes (FRNs) pay a fixed spread over a chosen variable benchmark rate. In the domestic market, the chosen variable rate is most often the 90-Day Bank Bill Swap Rate (BBSW). Investors, therefore, receive a variable total income that depends on the movements in the underlying benchmark rate in addition to the fixed spread (i.e. BBSW + 1.01%). This income differential is important for portfolio construction and the relative benefits of each strategy will depend on investment goals, market conditions and idiosyncratic risks of each security. Some of the key benefits of FRNs relative to fixed rate bonds are shown in table 1 below. Table 1. Comparison of FRN vs. Fixed Rate Features  Source: BondAdviser The trading margin or credit spread on a bond refers to the difference between a bond’s yield versus a comparable benchmark yield of the same tenor. Whilst there are many different spreads used in fixed income markets, plain vanilla bonds in Australia are priced based on their interpolated spread or “I-spread”. The I-spread is simply the difference between the bond’s yield to maturity (YTM), being the income level that equates price to face value, and the linearly interpolated yield for the same tenor to the benchmark (i.e. BBSW / swaps curve). Trading margins are affected by a number of factors including supply and demand, market sentiment, changes in credit ratings, expectations of early redemption or increased default risk and move inversely to prices (as they reflect the spread between relative yields, which also move inversely). When bond prices are adversely affected by these factors spreads “widen” (increase) whilst positive implications for bondholders generally see a “tightening” (decrease) in the trading margin / spread. Figure 1 below demonstrates (extreme) cases of both of these scenarios. For context, the significant tightening in the Seven Group TELYS 4 (ASX Code: SVWPA) was largely due to the equity conversion announcement on 22 August 2018 whilst the AMP Capital Notes (ASX Code: AMPPA) saw significant widening following the 25 October 2018 announcement that the Group would be selling its $3.4 billion AMP Life business. Figure 1. Changes in Trading Margins

Source: BondAdviser The trading margin or credit spread on a bond refers to the difference between a bond’s yield versus a comparable benchmark yield of the same tenor. Whilst there are many different spreads used in fixed income markets, plain vanilla bonds in Australia are priced based on their interpolated spread or “I-spread”. The I-spread is simply the difference between the bond’s yield to maturity (YTM), being the income level that equates price to face value, and the linearly interpolated yield for the same tenor to the benchmark (i.e. BBSW / swaps curve). Trading margins are affected by a number of factors including supply and demand, market sentiment, changes in credit ratings, expectations of early redemption or increased default risk and move inversely to prices (as they reflect the spread between relative yields, which also move inversely). When bond prices are adversely affected by these factors spreads “widen” (increase) whilst positive implications for bondholders generally see a “tightening” (decrease) in the trading margin / spread. Figure 1 below demonstrates (extreme) cases of both of these scenarios. For context, the significant tightening in the Seven Group TELYS 4 (ASX Code: SVWPA) was largely due to the equity conversion announcement on 22 August 2018 whilst the AMP Capital Notes (ASX Code: AMPPA) saw significant widening following the 25 October 2018 announcement that the Group would be selling its $3.4 billion AMP Life business. Figure 1. Changes in Trading Margins  Source: BondAdviser, Bloomberg Understanding the mechanics of how and why trading margins tighten or widen can help investors understand the factors affecting their portfolios. It is also important to know what the relative benefits or limitations are of FRNs versus fixed rate bonds, and is often overlooked, but can assist with security selection decisions based on credit positive or negative factors over time.

Source: BondAdviser, Bloomberg Understanding the mechanics of how and why trading margins tighten or widen can help investors understand the factors affecting their portfolios. It is also important to know what the relative benefits or limitations are of FRNs versus fixed rate bonds, and is often overlooked, but can assist with security selection decisions based on credit positive or negative factors over time.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.