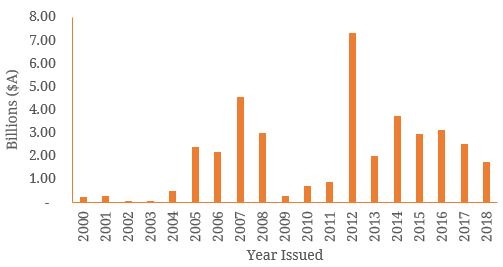

In Australia, there are two main forms of regulatory capital that financial institutions (FI’s) must hold to manage the risks inherent in their operations and ensure stability of the economy – Tier 2 and Tier 1 capital. Tier 2 capital securities rank below senior debt but above Tier 1 capital in the capital structure. Most commonly Tier 2 capital is referred to as “subordinated notes” and are more debt-like than the hybrid instruments common within (Additional) Tier 1 capital which show debt and equity features and reactions. Tier 2 ranks above equity whilst being junior to senior debt and term deposits. In essence, Tier 2 capital is “supplementary capital” whose main purpose is to absorb losses after a capital adequacy event whereby a financial institution enters liquidation, effectively acting as an additional layer of loss protection for FI’s. Since the announcement of Basel’s third pillar (Basel III), the popular reference often used by the Australian Prudential Regulatory Authority (APRA) and Basel Committee when discussing capital ratio benchmarks has been the Common Equity Tier 1 (CET1) ratio, whilst Tier 2 capital more often then not remained a subtopic despite having important implications for investors. Most notably, was the requirement of “non-viability trigger event” clauses in non-common equity instruments (such as hybrids and Tier 2 debt) for conversion to CET1 when a regulator deems a FI has reached a point of non-viability (PNV) and is no longer able to function. With Basel III coming into effect from January 2013, the listed Tier 2 capital market that had remained in relative obscurity post-GFC experienced a resurgence as Australian Banks scrambled to manage their liquidity and capital bases after witnessing the collapse and bailout of several foreign banks in overseas markets. Domestic FI’s rushed to raise T2 capital due to the uncertainty surrounding new regulations and lower costs of borrowing as investors sought higher premiums for new post-Basel III compliance structures. As a result, the listed T2 market issue size in the Australian domestic market ballooned by 829% YoY to above $7bn over the span of the next twelve months (Figure 1). Figure 1. Tier 2 Subordinated Debt Issuance by Year

Source: BondAdviser, Bloomberg

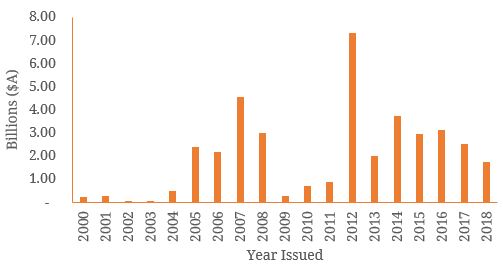

However, in the ensuing five years the market has contracted again with the dollar value of new issuances in both the listed and unlisted market falling to its lowest level since 2004, posing the question ‘why is the Listed Tier 2 Market dying’? A partial contributor could potentially be due to the previously aforementioned premiums sought by investors for the uncertainty surrounding the trigger point of PNV that APRA has not put a hard figure next to after the implementation of Basel III. This has seen an increasing trend in T2 capital instruments being offered directly to the wholesale market and institutional investors as they have become more difficult to accurately price as a consequence of such uncertainties. This culminated in a 3.5 year drought between the launch of Westpac’s Subordinated Notes II (WBCHB) in July 2013 and NAB Subordinated Notes 2 (NABPE), whilst during the same time frame, $6.5b of subordinated bonds were sold to wholesale investors around the globe. Perhaps a more significant function of the scarcity in supply to the ASX-listed market can be attributed to a lower cost of funds for banks and financial institutions when borrowing offshore due to favourable market conditions. Additionally, a shorter and less costly process through the elimination of listing fees and compliance issues has been a driving force behind the growth in issuance to wholesale investors. Another explanation for this phenomenon could simply be that many Australian FI’s have already met the reserve requirements set by regulators and are operating at or near their optimal regulatory capital settings. Lastly, a common trend by Australian banks has been to replace an existing issue of notes approaching maturity to allow holders to roll their position into a new offer. With the vast majority of subordinated notes issued with maturities of 10-years with optional calls occurring midway through the life of the security, this indicates the likeliness of the scarcity trend in the market to continue as seen below in Figure 2 below: Figure 2. Value of Subordinated Debt Maturing by Year

Source: BondAdviser, Bloomberg

Furthermore, with only three securities (AMPHA, SUNPD, WBCHB) set to expire in the next six months (Figure 3), it appears likely that the listed market for Tier 2 debt will slowly evaporate for the foreseeable future. Indeed, today Westpac announced the redemption of WBCHB with no new listed replacement. Figure 3. Value of Tier 2 Securities Maturing In The Short Term

Source: BondAdviser