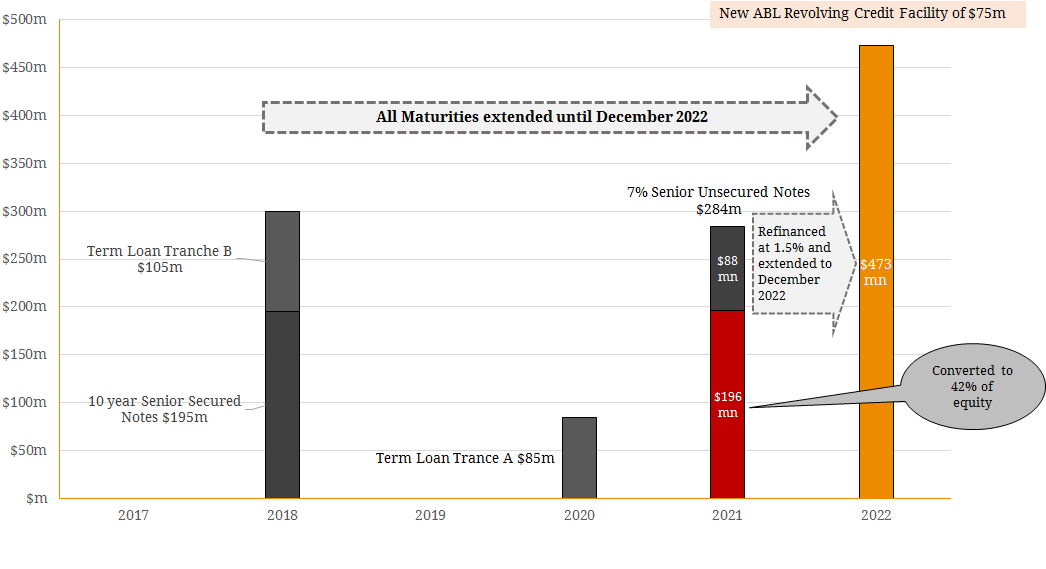

Amidst a global downturn in the resources sector, drilling company Boart Longyear (ASX: BLY) has suffered a challenging trading environment resulting in weak liquidity and profitability. In a bid to stay afloat and meet existing debt obligations, the company announced its intention to restructure its debt and capital last year. Earlier this month, BLY indicated that the recapitalisation plan had been agreed upon with its key creditors, Centrebridge, Ares and Ascibe to reduce debt and interest costs, improve liquidity and extend debt repayment deadlines. As a part of this plan, the company will:

- Exchange $US196 million of its 7.00% Senior Unsecured notes for 42% of the company’s equity and the remaining $US88 million will be reinstated with a 1.5% interest rate.

- The term for its bank loans will be extended until to December 2022.

- In order to provide additional liquidity, a new US$75 million ABL revolving credit facility fully backstopped by lenders which will provide US$35 million of additional debt capacity.

- Centrebridge, Ares and Ascribe will provide a short-term $US15 million loan for additional working capital.

Figure 1: BLY Proposed Capital Restructure Plan  Source: BondAdviser, Company Reports Following its recent poor performance, S&P downgraded the issuer’s corporate credit rating and notes and lowered its outlook to “Credit Watch Negative”. This is not the first time Boart Longyear has recapitalised its balance sheet. In 2014, hedge fund Centrebridge took part in a $400 million recapitalisation giving them a stake of just under 50% of the business. Boart Longyear has both secured and unsecured lenders, and requires 75% approval from both groups in order to proceed. US-based secured bond holders hold $US190m ($250m) of the company’s debt while Centrebridge holds two loans that are also secured. BLY wants Centrebridge to be included with the secured bondholders to ensure the recapitalisation plan progresses. However, this has faced opposition by other secured bondholders who seek more favourable terms. Their argument is that the plan would give Centrebridge 52% of equity in the company, a right that was not available to the other secured bondholders (who receive no equity). Subject to shareholder and other approvals, the recapitalisation was scheduled to be completed in June 2017. However, the restructure is unlikely to proceed without Centrebridge approval, and the decision as to its creditor standing will now be determined by the court. Boart Longyear follows a string of corporate debt restructuring in the resources sector over the past few years. While we believe the worst is now behind us, credit investors are now more vigilant of mining and mining services companies. Overall, these recent events highlight that even secured debt investors can face dire circumstances following a significant deterioration in the underlying issuer’s operations. Although investors associate secured assets as a meaningful risk mitigant, the Boart Longyear story illustrates this is not always the case. As a result, in-depth due diligence and credit research is warranted to avoid a messy recapitalisation with multiple parties and full repayment of capital is ensured.

Source: BondAdviser, Company Reports Following its recent poor performance, S&P downgraded the issuer’s corporate credit rating and notes and lowered its outlook to “Credit Watch Negative”. This is not the first time Boart Longyear has recapitalised its balance sheet. In 2014, hedge fund Centrebridge took part in a $400 million recapitalisation giving them a stake of just under 50% of the business. Boart Longyear has both secured and unsecured lenders, and requires 75% approval from both groups in order to proceed. US-based secured bond holders hold $US190m ($250m) of the company’s debt while Centrebridge holds two loans that are also secured. BLY wants Centrebridge to be included with the secured bondholders to ensure the recapitalisation plan progresses. However, this has faced opposition by other secured bondholders who seek more favourable terms. Their argument is that the plan would give Centrebridge 52% of equity in the company, a right that was not available to the other secured bondholders (who receive no equity). Subject to shareholder and other approvals, the recapitalisation was scheduled to be completed in June 2017. However, the restructure is unlikely to proceed without Centrebridge approval, and the decision as to its creditor standing will now be determined by the court. Boart Longyear follows a string of corporate debt restructuring in the resources sector over the past few years. While we believe the worst is now behind us, credit investors are now more vigilant of mining and mining services companies. Overall, these recent events highlight that even secured debt investors can face dire circumstances following a significant deterioration in the underlying issuer’s operations. Although investors associate secured assets as a meaningful risk mitigant, the Boart Longyear story illustrates this is not always the case. As a result, in-depth due diligence and credit research is warranted to avoid a messy recapitalisation with multiple parties and full repayment of capital is ensured.