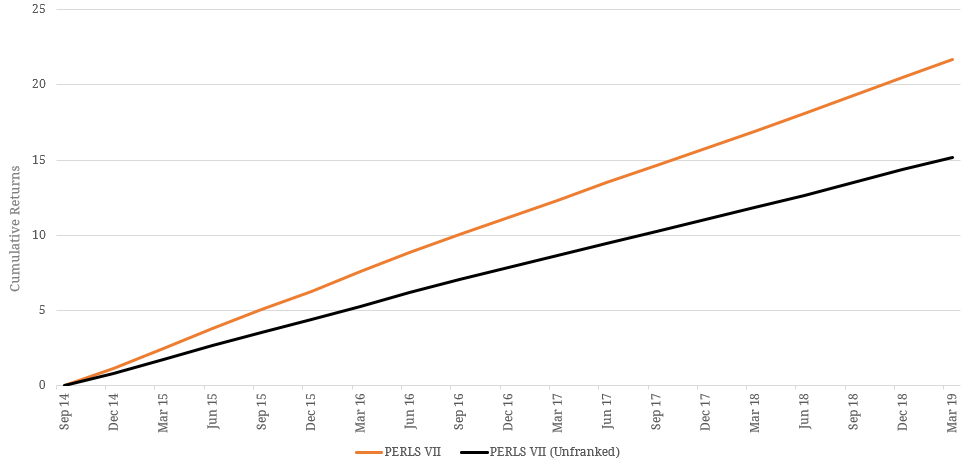

It would be safe to assume that popular search engines have witnessed a dramatic increase in ‘franking credits’ inquiries since the Leader of the Opposition divulged his party’s proposed changes to the scheme a year ago. Whilst there is still water to go under the bridge on that front, the popularity of Australia’s dividend imputation system as a discussion point has demonstrated just how poorly it is understood. This includes its application to Australian bank hybrid securities. Generally, for investors of Australian shares, dividends paid to them by Australian resident companies are taxed under an imputation system. Tax paid by a company may be attributed to qualifying shareholders by way of franking credits attached to the dividends they receive. This means that dividends paid include a franking credit, at the current company tax rate (generally 30%), to avoid double taxation for investors. To qualify, an investor need only hold shares continuously ‘at risk’ for at least 45 days (ATO’s ‘Holding Period Rule’). For investors in Australian bank hybrid securities, distributions may be subject to the same imputation system, and up to 30% of the gross distribution may be passed on to investors in the form of franking credits similar to the mechanism of dividends on shares. An important difference is that under the ATO’s rule, investors in these securities must continuously hold the instrument ‘at risk’ for at least 90 days. A key side point for investors is that they should generally not be purchasing hybrid securities within the final 90 days period prior to redemption. This is because, assuming a grossed-up yield, the investor would not be eligible for franking credit offset. Of course, an investor could still buy the securities on a cash / net yield basis. Whilst this is a small tax factor in the hybrid market, there is an important distinction in pricing for existing investors rather than new investors. Excepting pensioners, the proposed changes are limited to excess imputation credit refunds. These apply to investors whose total imputation credits attached to franked dividends paid exceed their basic income tax liability for the year. However, given the positive correlation between those investing for income through hybrids and those with reduced working incomes, we feel it may be particularly relevant to some of our readership. Figure 1 below shows the income effect that would have been felt by holders of the PERLS VII (ASX: CBAPD), should the policy have been introduced at its issuance. Figure 1. Franking Credit Comparison: PERLS VII Cumulative Distribution Returns  Source: BondAdviser Exact price impacts from the possible removal of franking credits are difficult to predict, so for the purposes of this discussion the premise that each instrument issues and will redeem at par will suffice – i.e. ignore pricing. It is therefore only the distribution component which provides relevance. Those investors most affected may need to look elsewhere for higher returns should they wish to maintain income levels, although they would be moving up the risk curve to do so. Other investors may trade out of their Tier 1 (franked) securities for more secure Tier 2 securities or higher yielding non-bank corporate bonds (each unfranked). By way of an example, NAB Capital Notes 2 (ASX: NABPD), a Tier 1 instrument, was issued in June 2016 at an attractive margin of 4.95% p.a. above 90-Day BBSW, fully franked. It is scheduled to pay a quarterly cash distribution of $1.22 on 8 April 2019, but under the proposed changes, some may not be able to fully utilise the $0.52 franking credit (tax already paid by NAB). As a comparison, NAB Subordinated Notes 2 (ASX: NABPE), a Tier 2 security, offers a margin of 2.20% p.a. above 90-Day BBSW, unfranked. It is scheduled to pay a quarterly cash distribution $1.05 on 20 March 2019. We chart the cumulative distributions for three scenarios below. Figure 2. Franking Credit Comparison: NAB Cumulative Distribution Returns

Source: BondAdviser Exact price impacts from the possible removal of franking credits are difficult to predict, so for the purposes of this discussion the premise that each instrument issues and will redeem at par will suffice – i.e. ignore pricing. It is therefore only the distribution component which provides relevance. Those investors most affected may need to look elsewhere for higher returns should they wish to maintain income levels, although they would be moving up the risk curve to do so. Other investors may trade out of their Tier 1 (franked) securities for more secure Tier 2 securities or higher yielding non-bank corporate bonds (each unfranked). By way of an example, NAB Capital Notes 2 (ASX: NABPD), a Tier 1 instrument, was issued in June 2016 at an attractive margin of 4.95% p.a. above 90-Day BBSW, fully franked. It is scheduled to pay a quarterly cash distribution of $1.22 on 8 April 2019, but under the proposed changes, some may not be able to fully utilise the $0.52 franking credit (tax already paid by NAB). As a comparison, NAB Subordinated Notes 2 (ASX: NABPE), a Tier 2 security, offers a margin of 2.20% p.a. above 90-Day BBSW, unfranked. It is scheduled to pay a quarterly cash distribution $1.05 on 20 March 2019. We chart the cumulative distributions for three scenarios below. Figure 2. Franking Credit Comparison: NAB Cumulative Distribution Returns  Source: BondAdviser Effectively, certain investors could move up the capital stack, improving the credit quality of their investment whilst sacrificing only ~68bps p.a. in distributions. It should be noted that wholesale investors will have a greater scope of choice in the Tier 2 market, but greater options could be available to all investors through APRA’s TLAC proposals if this sees a return of listed Tier 2 issuance. Regardless of investor class, should the proposed changes come to fruition, those affected will need to restructure their portfolios in order to maintain returns and unfortunately, not everyone will have the same post-tax approach.

Source: BondAdviser Effectively, certain investors could move up the capital stack, improving the credit quality of their investment whilst sacrificing only ~68bps p.a. in distributions. It should be noted that wholesale investors will have a greater scope of choice in the Tier 2 market, but greater options could be available to all investors through APRA’s TLAC proposals if this sees a return of listed Tier 2 issuance. Regardless of investor class, should the proposed changes come to fruition, those affected will need to restructure their portfolios in order to maintain returns and unfortunately, not everyone will have the same post-tax approach.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.