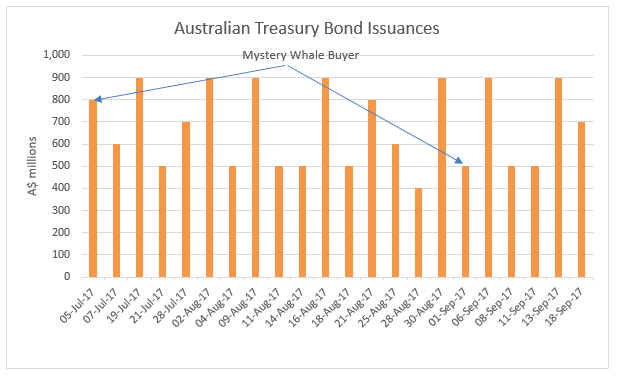

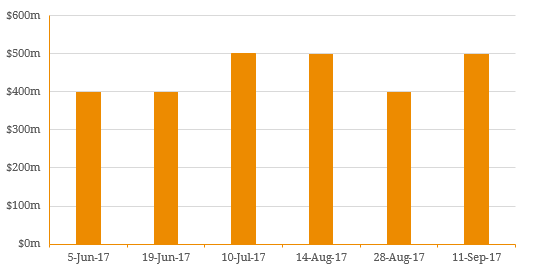

In early July, a sole bidder purchased the entirety of the $800 million primary issue of new Australian government bonds with a 2029 maturity (12-years). This was the highest ever for a single bidder since official statistics started in 1982. In early September, another lone buyer purchased the entire $500 million issuance of government bonds in a single bid. To see how such large trades could occur, we first need to look into the government bond primary issuance process – a fundamental mechanism for the fixed income market since government bond valuation partially determines the risk-free yield curve, which in turn underpins the pricing of trillions of dollars of other instruments in the market. Figure 1. Australian Commonwealth Government Bond (AGCB) Issuance  Source: AOFM Australian Government Securities are issued by competitive tender and occasionally via syndicated offerings. The tenders are conducted by The Australian Office of Financial Management (AOFM) using the AOFM Tender System, which is accessed via the Yieldbroker DEBTS System. Bids for stock offered for sale via the Tender System may only be submitted by parties that are registered with the AOFM. Before an auction date, the AOFM will make available to the public a Tender Announcement, which provides full details of the tender, including details of the stock that is being offered. Once bids are made on the auction date, acceptance of bids will be made in ascending order of the Yield bidded, that is, from the lowest Yield bid to the highest Yield accepted. Contingent of the issue size, allotments will be made at the Yields bid. The Commonwealth reserves the right to accept any bid for the full amount of a tender or any part thereof and to reject any bid or part thereof. The above process is why it may be possible for a single bidder to place a bid competitive enough for it to receive the entire offer amount. This is in contrast to Treasury bond auctions in the US, where small investors or individuals who have submitted bids (called non-competitive bids) are always guaranteed to receive some allocation, and bigger investors such as institutions or foreign central banks (called competitive bidders) are each restricted to receiving no more than 35% of the total amount of bonds available to the public. The AOFM also regularly conducts treasury bond buybacks, through a similar auction process. Bond holders who wish to sell their holdings back to the Commonwealth submit their offers and the acceptance of offers will be made in descending order of Yield offered, that is, from the highest Yield offered to the lowest Yield accepted. Repurchases will be made at the Yields offered. Similarly to issuance auctions, the Commonwealth reserves the right to accept any offer for the full amount of a tender or any part thereof and to reject any offer or part thereof. Figure 2. Australian Commonwealth Government Bond (AGCB) Buy-Backs

Source: AOFM Australian Government Securities are issued by competitive tender and occasionally via syndicated offerings. The tenders are conducted by The Australian Office of Financial Management (AOFM) using the AOFM Tender System, which is accessed via the Yieldbroker DEBTS System. Bids for stock offered for sale via the Tender System may only be submitted by parties that are registered with the AOFM. Before an auction date, the AOFM will make available to the public a Tender Announcement, which provides full details of the tender, including details of the stock that is being offered. Once bids are made on the auction date, acceptance of bids will be made in ascending order of the Yield bidded, that is, from the lowest Yield bid to the highest Yield accepted. Contingent of the issue size, allotments will be made at the Yields bid. The Commonwealth reserves the right to accept any bid for the full amount of a tender or any part thereof and to reject any bid or part thereof. The above process is why it may be possible for a single bidder to place a bid competitive enough for it to receive the entire offer amount. This is in contrast to Treasury bond auctions in the US, where small investors or individuals who have submitted bids (called non-competitive bids) are always guaranteed to receive some allocation, and bigger investors such as institutions or foreign central banks (called competitive bidders) are each restricted to receiving no more than 35% of the total amount of bonds available to the public. The AOFM also regularly conducts treasury bond buybacks, through a similar auction process. Bond holders who wish to sell their holdings back to the Commonwealth submit their offers and the acceptance of offers will be made in descending order of Yield offered, that is, from the highest Yield offered to the lowest Yield accepted. Repurchases will be made at the Yields offered. Similarly to issuance auctions, the Commonwealth reserves the right to accept any offer for the full amount of a tender or any part thereof and to reject any offer or part thereof. Figure 2. Australian Commonwealth Government Bond (AGCB) Buy-Backs  Source: AOFM

Source: AOFM

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.