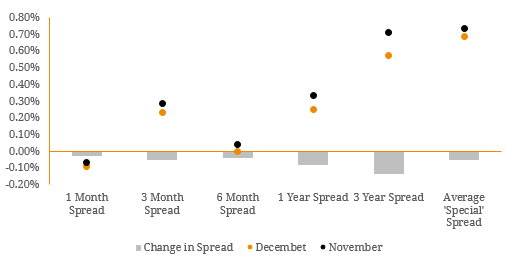

At the end of February, we published “Term Deposits – Past, Current and Future Trends” outlining our expectation that term deposit margins would increase due to competitive pressures between Authorised Depository Institutions (ADIs). Since the commentary was written, term deposit margins have indeed risen by ~0.20%. Figure 1. Term Deposit Spreads  Source: RBA, AFMA, BondAdviser As shown in Figure 2 below, the Bank Bill Swap Rate (BBSW) across different terms are highly correlated to changes in the RBA cash rate. This effectively means that term deposit yields are tied to the decisions of the RBA and the state of the wider economy. Figure 2. Average Term Deposit Spread Vs Average BBSW Rate

Source: RBA, AFMA, BondAdviser As shown in Figure 2 below, the Bank Bill Swap Rate (BBSW) across different terms are highly correlated to changes in the RBA cash rate. This effectively means that term deposit yields are tied to the decisions of the RBA and the state of the wider economy. Figure 2. Average Term Deposit Spread Vs Average BBSW Rate Source: RBA, AFMA, BondAdviser Note: Average BBSW is made up of 1M, 3M, 6M, 1Y and 3Y BBSW Rates. The Reserve Bank of Australia’s (RBA) decision to cut the cash rate by 0.25% to 1.75% in May showed that monetary easing is still on the agenda. As a result, term deposit yields remain under pressure. While we still believe this could be offset by modest increases in term deposit margins (as seen with the May rate cut), it is uncertain if these increases will keep up with further cash rate cuts. Markets are currently pricing in a 60% probability of rate cut in August which would result in a cash rate of 1.50% and further rate cuts in 2017 are expected if global market volatility continues. Figure 3. Average Term Deposit Spread Vs Average BBSW Rate

Source: RBA, AFMA, BondAdviser Note: Average BBSW is made up of 1M, 3M, 6M, 1Y and 3Y BBSW Rates. The Reserve Bank of Australia’s (RBA) decision to cut the cash rate by 0.25% to 1.75% in May showed that monetary easing is still on the agenda. As a result, term deposit yields remain under pressure. While we still believe this could be offset by modest increases in term deposit margins (as seen with the May rate cut), it is uncertain if these increases will keep up with further cash rate cuts. Markets are currently pricing in a 60% probability of rate cut in August which would result in a cash rate of 1.50% and further rate cuts in 2017 are expected if global market volatility continues. Figure 3. Average Term Deposit Spread Vs Average BBSW Rate  Source: RBA, AFMA, BondAdviser Note: Average BBSW is made up of 1M, 3M, 6M, 1Y and 3Y While many Australians will accept lower term deposit returns off the back of further rate cuts in order to maintain capital preservation, we expect there will be some investors that will reallocate capital further up the risk spectrum in search for yield. Figure 4 depicts this risk-return relationship across the bank capital structure. This, in addition to growing deposit competition for funding and liquidity requirements, is a major reason why the RBA’s May rate cut was not passed on to term deposit investors. As shown in Figure 3 above, the average BBSW rate fell but the average term deposit margin increased. As a result, term deposit yields remained broadly unchanged ensuring deposits remained an attractive investment option on a risk-return basis. Figure 4. Average Trading Margin of Different Bank Securities of the Risk Spectrum

Source: RBA, AFMA, BondAdviser Note: Average BBSW is made up of 1M, 3M, 6M, 1Y and 3Y While many Australians will accept lower term deposit returns off the back of further rate cuts in order to maintain capital preservation, we expect there will be some investors that will reallocate capital further up the risk spectrum in search for yield. Figure 4 depicts this risk-return relationship across the bank capital structure. This, in addition to growing deposit competition for funding and liquidity requirements, is a major reason why the RBA’s May rate cut was not passed on to term deposit investors. As shown in Figure 3 above, the average BBSW rate fell but the average term deposit margin increased. As a result, term deposit yields remained broadly unchanged ensuring deposits remained an attractive investment option on a risk-return basis. Figure 4. Average Trading Margin of Different Bank Securities of the Risk Spectrum  Source: BondAdviser, Westpac, RBA Ultimately, the current state of the deposit market is a result of growing regulatory pressure in the Australian banking system. The Australian Prudential Regulatory Authority (APRA) is continuing to push banks back into traditional funding sources (such as household deposits) in an attempt to reduce the major banks’ reliance on offshore channels. This will be measured by a new global metric known as the Net Stable Funding Ratio (NSFR) which is expected to be introduced in 2018. As a result, banks will need to keep deposit holders content in an intensifying competitive landscape (see Figure 5). For this reason, we believe term deposit margins remain skewed to the upside to remain attractive. Figure 5. Average Major Bank Retail Deposit Growth (Y/Y)

Source: BondAdviser, Westpac, RBA Ultimately, the current state of the deposit market is a result of growing regulatory pressure in the Australian banking system. The Australian Prudential Regulatory Authority (APRA) is continuing to push banks back into traditional funding sources (such as household deposits) in an attempt to reduce the major banks’ reliance on offshore channels. This will be measured by a new global metric known as the Net Stable Funding Ratio (NSFR) which is expected to be introduced in 2018. As a result, banks will need to keep deposit holders content in an intensifying competitive landscape (see Figure 5). For this reason, we believe term deposit margins remain skewed to the upside to remain attractive. Figure 5. Average Major Bank Retail Deposit Growth (Y/Y)  Source: APRA Although increased term deposit margins will reduce the net interest margins (NIM) of banks, we do not believe this will impact bank capital levels (given recent capital raising initiatives) and instead, will affect profitability. This is consistent with our view that the Australian banking system is in a transitional period regarding regulation and this should ultimately lead to less leverage and more risk controls. Overall, this is a positive for fixed income investors across the bank capital structure. While term deposit margins are likely to increase, overall term deposit yield stability will be dependent on RBA monetary policy and the speed of the current interest rate cycle. At this point it is almost impossible to predict when the cash rate will bottom out given the current state of the global economy. However, we believe competitive pressures between ADIs and transitory regulation will offer investors some protection against the ‘lower for longer’ interest rate environment. Current Term Deposit Offerings: Figure 6. Short Term Term Deposit Rates (~3M)

Source: APRA Although increased term deposit margins will reduce the net interest margins (NIM) of banks, we do not believe this will impact bank capital levels (given recent capital raising initiatives) and instead, will affect profitability. This is consistent with our view that the Australian banking system is in a transitional period regarding regulation and this should ultimately lead to less leverage and more risk controls. Overall, this is a positive for fixed income investors across the bank capital structure. While term deposit margins are likely to increase, overall term deposit yield stability will be dependent on RBA monetary policy and the speed of the current interest rate cycle. At this point it is almost impossible to predict when the cash rate will bottom out given the current state of the global economy. However, we believe competitive pressures between ADIs and transitory regulation will offer investors some protection against the ‘lower for longer’ interest rate environment. Current Term Deposit Offerings: Figure 6. Short Term Term Deposit Rates (~3M)  Source: Company Data, BondAdviser Figure 7. Medium Term Term Deposit Rates (~6M)

Source: Company Data, BondAdviser Figure 7. Medium Term Term Deposit Rates (~6M)  Source: Company Data, BondAdviser Figure 8. Long Term Term Deposit Rates (~12M)

Source: Company Data, BondAdviser Figure 8. Long Term Term Deposit Rates (~12M)  Source: Company Data, BondAdviser Background of Deposits Deposits offer investors a range of benefits over other types of investments. The diverse offering in Australia allows for investment flexibility. Depositors are able to choose their investment term and deposit type. This allows the investors to effectively express their view on interest rates. Additionally, deposits offer certainty of returns. The type of deposit and level of base rate on the transaction date remains unchanged during the duration of the investment. This allows the investor avoid market volatility. The fixed margin or spread (the difference between the advertised deposit rate and benchmark swap rate) of the deposit will depend on prevailing market conditions on the transaction date. On the negative side, term deposits can only be liquidated early with the issuing institution (i.e. there is no open market). Although deposits offer a certain return, there is no capital upside as there is in bonds if interest rates fall.

Source: Company Data, BondAdviser Background of Deposits Deposits offer investors a range of benefits over other types of investments. The diverse offering in Australia allows for investment flexibility. Depositors are able to choose their investment term and deposit type. This allows the investors to effectively express their view on interest rates. Additionally, deposits offer certainty of returns. The type of deposit and level of base rate on the transaction date remains unchanged during the duration of the investment. This allows the investor avoid market volatility. The fixed margin or spread (the difference between the advertised deposit rate and benchmark swap rate) of the deposit will depend on prevailing market conditions on the transaction date. On the negative side, term deposits can only be liquidated early with the issuing institution (i.e. there is no open market). Although deposits offer a certain return, there is no capital upside as there is in bonds if interest rates fall.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.