Suncorp issued a new Tier 2 capital instrument earlier this week with the wholesale 10 year, non-call 5 year security issued at a margin of 2.30%. Issued into the wholesale market with Austraclear settlement, the bond is generally bought and traded by Institutional investors or investors that qualify as wholesale sophisticated investors. These investors typically mark their portfolios to market prices on a frequent basis, and as a consequence, they can be reasonably sensitive to events that influence market prices like geo-political events in Ukraine, or more predictable things like inflationary risk, which can build more slowly but is generally seen in advance.

Had Suncorp issued its 5-year callable subordinated bond (Tier 2 bond) just three months ago, the margin would have been materially under the 2% mark as market influences from inflationary pressures stemming from the US market, the Ukraine events, and the likelihood of rate rises in Australia were (while developing) less prominent.

Historically, a reasonable guide to margin predictability were ratios between senior bonds and Tier 2 capital instruments as well as ratios between Tier 2 and Tier 1 capital instruments. While the senior/Tier 2 ratio has been more stable, albeit with heightened volatility lately, the difference in margins between Tier 2 and Tier 1 securities for banks has significantly converged. This convergence has been consistent over the last 6 months and ultimately driven by fundamental differences in investor behaviour participating in Tier 2 and Tier 1 markets.

As Suncorp issued its new Tier 2 security this week with first call at 5 years and an issue margin of 2.30%, Suncorp’s listed Tier 1 securities tightened through the end of Quarter on 31 March to the following trading margins:

- SUNPI: 79% (6.2 years to call)

- SUNPH: 2.52% (4.2 years to call)

- SUNPG: 2.39% (2.2 years to call)

Using SUNPH as the closest comparison term to the new Tier 2 issue and extrapolating SUNPH’s trading margin to match a 5-year call, the margin differential would be as follows:

Suncorp Tier 2: 2.30% (5-year call) vs SUNPH @ 2.63% (extrapolated 5 years to call).

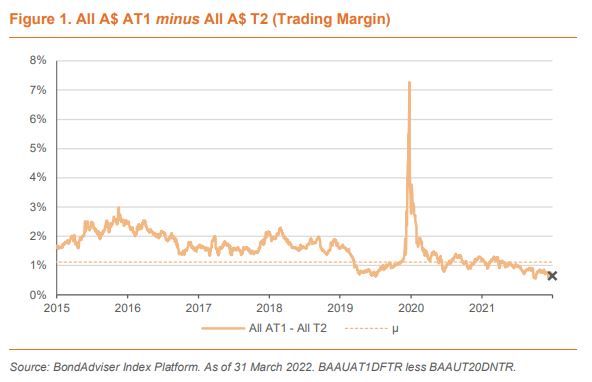

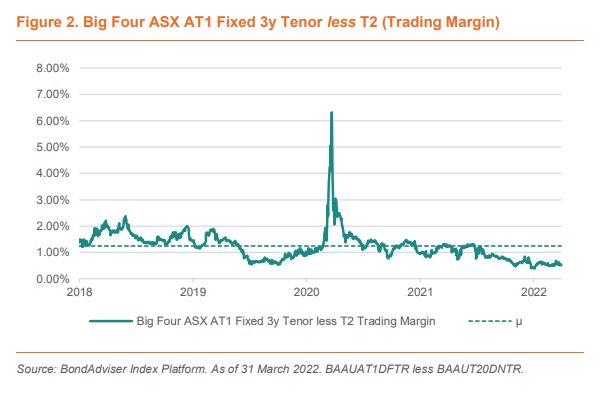

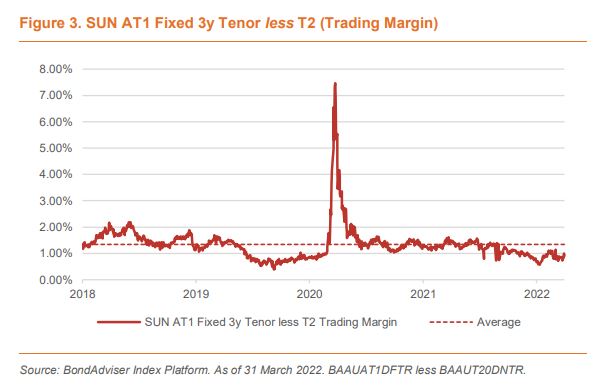

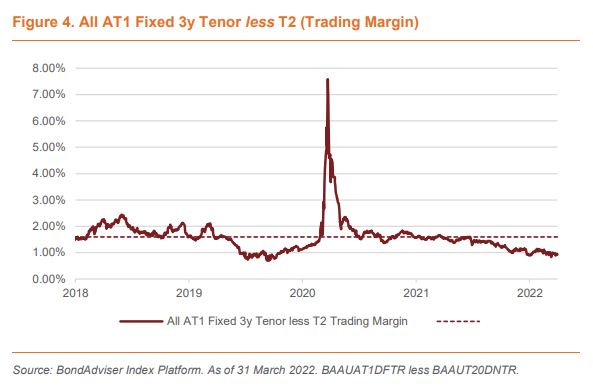

This represents a 33-basis point premium from Tier 2 to Tier 1. Over the last 7 years, this premium for all issuers has averaged a materially larger 158 basis points (see Figures 1). The trend for more broader contraction in the market’s Tier 2 to Tier 1 margin differential over the last 12 months is also shown as follows in Figures 2 to 4.

A key reason for the contraction has been the vastly more sensitive wholesale investor market for Tier 2 securities, which has in recent months seen Tier 2 widen substantially, yet we have not seen the same move at all within the listed Tier 1 market, where investors are much more comfortable holding their investments to the call date without a need to mark its value daily. i.e., events in Ukraine and the threat of rate rises doesn’t generally bother the listed investor. Hybrids are generally floating rate instruments, and so rate risk is not a major consideration for most investors.

Normally, these sorts of differentials work themselves out over time, and it would be expected to happen here too, however a number of other issues have exacerbated the situation at present and maintained an abnormally small differential between Tier 2 and Tier 1 trading margins.

Firstly, capital requirements expected by the prudential regulator over the next few years are expected to be resolved by more issuance of Tier 2. This will increase supply comparative to Tier 1 and be a margin expanding input for Tier 2 performance. Additionally, the recently implemented Design and Distribution Obligations legislation (DDO) impacting on listed security issues, such as Tier 1 issues has meant that non-wholesale investors have to wait until the issues list before buying. This creates a material amount of demand on the first day of listing (as we have seen with the recent issues of ANZPJ and CBAPK) and undergirds the strength of Tier 1 trading margins over the short term – particularly at times of new issuance. Again, this happens without any concerns for events that remain the daily focus of Tier 2 capital investors.

We expect to see continued weakness in Tier 2 margins over the medium term meaning that this contracted differential between Tier 1 and Tier 2 should continue for some time. Any correction in the meantime is likely to be seen in the Tier 1 market once investor demand is sated with new issues and domestic rates begin to rise as early as mid-year.