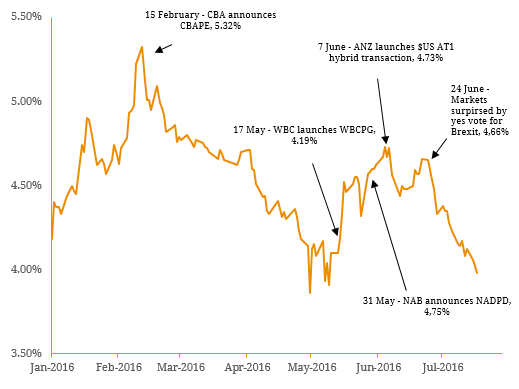

Over the first half of 2016 the four major Australian banks have issued ~A$4.65 billion of domestic and US$1 billion of offshore hybrids. In a globally low interest rate environment, these issues have been well supported by investors and this is reflected in the movement of the average hybrid trading margin over 2016. Figure 1. AT1 Average Trading Margin  Source: BondAdviser as at 20th July 2016 One of the key risks of investing in this class of security is the risk of conversion into ordinary shares upon a Loss Absorption Event. Whilst none of the four major banks have been forced to convert a hybrid into ordinary shares to date, uncertainty surrounding the conversion process was highlighted eight years ago during the Global Financial Crisis (GFC). On the 9th of July 2008 the ANZ issued a notice outlining the rights of ANZ Stapled Exchangeable Preferred Securities (ANZ StEPS) hybrid holders in the lead up to their first Reset Date of 15th of September 2008. This included that they were considering offering a replacement security. The ANZ StEPS were issued in August 2003 at a margin of 4.85% over the 90 day bank bill swap rate (90BBSW). In summary, upon receiving a legitimate Holder Exchange Notice the ANZ was obliged to do one or a combination of the following (at ANZ’s election) as outlined in the prospectus:

Source: BondAdviser as at 20th July 2016 One of the key risks of investing in this class of security is the risk of conversion into ordinary shares upon a Loss Absorption Event. Whilst none of the four major banks have been forced to convert a hybrid into ordinary shares to date, uncertainty surrounding the conversion process was highlighted eight years ago during the Global Financial Crisis (GFC). On the 9th of July 2008 the ANZ issued a notice outlining the rights of ANZ Stapled Exchangeable Preferred Securities (ANZ StEPS) hybrid holders in the lead up to their first Reset Date of 15th of September 2008. This included that they were considering offering a replacement security. The ANZ StEPS were issued in August 2003 at a margin of 4.85% over the 90 day bank bill swap rate (90BBSW). In summary, upon receiving a legitimate Holder Exchange Notice the ANZ was obliged to do one or a combination of the following (at ANZ’s election) as outlined in the prospectus:

- subject to APRA’s approval) repurchase them for $100 per each unit of ANZ StEPS;

- Arrange for a third party to purchase them for $100 per each unit of ANZ StEPS; or

- Convert them into ANZ ordinary shares in accordance with a formulae set out in the Issue Terms which broadly involves issuing ordinary shares to an equivalent market value less a 2.5% discount.

On the 29th of July 2008 ANZ advised StEPS holders of their decision to exchange all ANZ StEPS by way of conversion into ANZ ordinary shares at a 2.5% discount, meaning that the cash repurchase option was not available to ANZ StEPS holders. While we do not know for certain whether APRA declined to give approval to the ANZ to repurchase each ANZ StEP at face value or whether ANZ deliberately chose to convert the ANZ StEPS into equity, this was the safest option for the ANZ to take from a capital management point of view given the unfolding GFC event. The conversion of the ANZ StEPS into equity was one of the major contributors to the ANZ being able to increase their Tier 1 capital ratio from 6.9% (March 2008) to 7.7% (September 2008) as shown in Figure 2. Figure 2. ANZ Capital Management extract (September 2008)  Source: ANZ https://www.shareholder.anz.com/pages/financial-spreadsheets However, for those investors who were either unable to take delivery of ANZ shares in their portfolios upon conversion or who wished to reduce their exposure to movements in the ANZ share price during the conversion period, arrangements were made for these investors to sell their ANZ StEPS holding to a third party broker at face value. In this case it was the third party broker who took on the conversion risk and eventually placed the resulting ordinary shares derived from the conversion process of the ANZ StEPS back to the equity market. Subsequently on the 27th of August 2008 ANZ lodged the replacement hybrid prospectus and eventually were able to issue $1.08 billion of the ANZ Convertible Preference Shares (CPS) on the 30th of September 2008 at a margin of 2.50% over 90BBSW. Conclusion: Bank hybrids are complex instruments and there is no guarantee that investor will receive cash back at the first or any other optional call date. ANZ StEPS is a prime example of what an issuer (namely a bank) can and will do if required. Hybrid investors need to understand they are not 100% guaranteed to be paid out in cash at the first reset date despite having the expectation that they will be.

Source: ANZ https://www.shareholder.anz.com/pages/financial-spreadsheets However, for those investors who were either unable to take delivery of ANZ shares in their portfolios upon conversion or who wished to reduce their exposure to movements in the ANZ share price during the conversion period, arrangements were made for these investors to sell their ANZ StEPS holding to a third party broker at face value. In this case it was the third party broker who took on the conversion risk and eventually placed the resulting ordinary shares derived from the conversion process of the ANZ StEPS back to the equity market. Subsequently on the 27th of August 2008 ANZ lodged the replacement hybrid prospectus and eventually were able to issue $1.08 billion of the ANZ Convertible Preference Shares (CPS) on the 30th of September 2008 at a margin of 2.50% over 90BBSW. Conclusion: Bank hybrids are complex instruments and there is no guarantee that investor will receive cash back at the first or any other optional call date. ANZ StEPS is a prime example of what an issuer (namely a bank) can and will do if required. Hybrid investors need to understand they are not 100% guaranteed to be paid out in cash at the first reset date despite having the expectation that they will be.