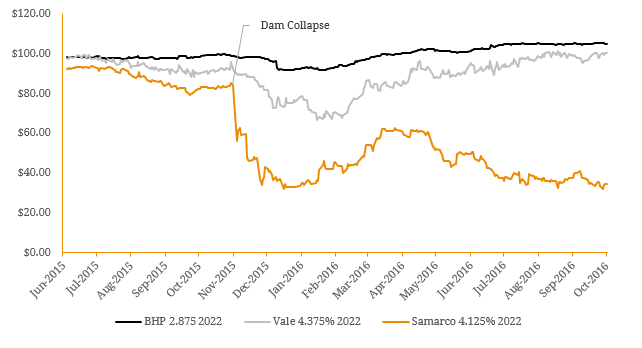

Back in November 2015, news came too light that a Brazilian dam owned by a BHP joint-venture had collapsed, fatally injuring a number of employees and damaging nearby communities. This was followed by extensive legal proceedings brought forward by Brazilian government regarding clean-up costs and compensation of BRL155 billion (~AUD $62.5 million). Samarco is a joint-venture between BHP Billiton and Vale with a 50/50 ownership split. As a result of the ongoing costs and suspended operations, Samarco has had virtually no cashflow in 2016 and on the 26th of September the joint-venture missed an interest payment ($US13.5 billion) on a $US500 million bond. The inaction reflects BHP and Vale’s reluctance to provide the venture with additional funding and with $US54 million in interest payments on three separate bonds scheduled in November, bondholders may be forced into a complicated bankruptcy and subsequent debt restructuring process. Combined, BHP and Vale boast revenues of ~$US60 billion and total assets are valued around ~$US180 billion. It would appear that Samarco’s interest payments are easily manageable for both companies so why has the money not been paid? When subsidiaries of large corporate companies issue debt securities, they can elect to provide a guarantee. This essentially means that if the entity fails (Samarco), the parent company(s) (BHP, Vale) are legally obliged to pay forthcoming interest payments and the principal at maturity. However, Samarco bonds do not have any guarantee and as a result, both BHP and Vale are subject to no such obligation. While BHP and Vale remain committed to reparatory/rehabilitation costs, they have maintained their stance on not supporting the joint venture’s non‑recourse debt. Figure 1. BHP, Vale and Samarco Comparable US Dollar Denominated Bond Performance  Source: Bloomberg According to the contractual terms of the security, Samarco now has 30 days to make the payment or else investors holding at least 25% of the aggregate market value could declare the principal due immediately. As there is still growing uncertainty as to when mines will resume operations, it is unlikely this obligation will be met and creditor negotiations will commence. At the end of 2015, Samarco had approximately ~$7 billion of total assets on balance sheet and Net Debt to EBITDA came in at 3.05 times. Given the covenant maximum of 4.0x, this has now been breached. In these financial statements, a guarantee was made in the Liquidity Risk section regarding its clean-up/compensatory obligations: “According to the Transaction and Conduct Adjustment Term (TTAC), Vale and BHP are obliged at the proportion of 50% each to cover the contributions Samarco is obliged to make under the settlement, if Samarco does not have sufficient funds to honor its obligations.” Given this agreement, we can expect BHP and Vale to hold this commitment and creditor payments will need to paid out of Samarco operations entirely. Both companies have written Samarco’s value down to zero, and are battling through an era of lower commodity prices. For this reason, we expect the owners to remain avoidant. For the joint-venture to be viable, we believe it will need to reduce costs, restructure its debts and provide transparency regarding regulatory approvals. As none of these have been done yet, there seems to be a long journey ahead for bondholders. Overall, these recent events highlight the importance of understanding a security’s documentation and structure. While some companies attempt to avoid reputational damage, the same cannot be said for BHP and Vale which have left Samarco debt investors in limbo. Samarco bonds would have been issued a higher coupon to those that had not been backed by the parent companies, but investors have now paid the price of with ~65% capital losses across the Samarco bond curve. Although the dam collapse was an extreme and unpredictable event, they can occur and investors need to ensure they do not get caught out yield-chasing.

Source: Bloomberg According to the contractual terms of the security, Samarco now has 30 days to make the payment or else investors holding at least 25% of the aggregate market value could declare the principal due immediately. As there is still growing uncertainty as to when mines will resume operations, it is unlikely this obligation will be met and creditor negotiations will commence. At the end of 2015, Samarco had approximately ~$7 billion of total assets on balance sheet and Net Debt to EBITDA came in at 3.05 times. Given the covenant maximum of 4.0x, this has now been breached. In these financial statements, a guarantee was made in the Liquidity Risk section regarding its clean-up/compensatory obligations: “According to the Transaction and Conduct Adjustment Term (TTAC), Vale and BHP are obliged at the proportion of 50% each to cover the contributions Samarco is obliged to make under the settlement, if Samarco does not have sufficient funds to honor its obligations.” Given this agreement, we can expect BHP and Vale to hold this commitment and creditor payments will need to paid out of Samarco operations entirely. Both companies have written Samarco’s value down to zero, and are battling through an era of lower commodity prices. For this reason, we expect the owners to remain avoidant. For the joint-venture to be viable, we believe it will need to reduce costs, restructure its debts and provide transparency regarding regulatory approvals. As none of these have been done yet, there seems to be a long journey ahead for bondholders. Overall, these recent events highlight the importance of understanding a security’s documentation and structure. While some companies attempt to avoid reputational damage, the same cannot be said for BHP and Vale which have left Samarco debt investors in limbo. Samarco bonds would have been issued a higher coupon to those that had not been backed by the parent companies, but investors have now paid the price of with ~65% capital losses across the Samarco bond curve. Although the dam collapse was an extreme and unpredictable event, they can occur and investors need to ensure they do not get caught out yield-chasing.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.