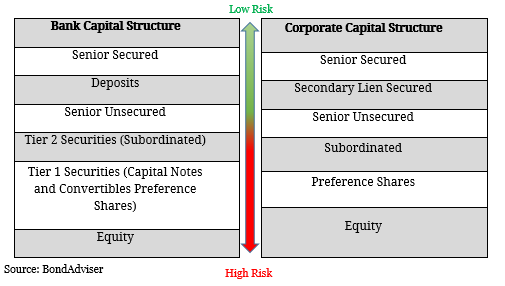

In Australia, financial institutions continually use debt capital markets as source of funding. But what about other companies? The majority of ASX200 non-financial groups tend to issue overseas in larger markets such as the UK, the Eurozone, Singapore and the US. From our findings, we discovered on average 44% of borrowings for ASX200 companies that have marketable debt in Australia is domiciled outside Australia (i.e. in the form of Foreign Bonds, US Private Placements and Euro-dollar debt). This is primarily of function of funding diversification, allowing these companies to tap different funding sources when needed. In Australian debt markets, most of these companies issue in the over-the-counter (OTC) market which is generally out of reach to retail investors. However, how analysis has uncovered 146 different securities that meet special eligibility requirements to be transmuted into listed Chess Depository Interests (CDIs). This enables the holder to receive coupon payments and principal repayment at maturity from the security over which the CDI has been issued without holding the security directly (similar to Australian Government Bonds trading on the ASX currently). This would significantly improve retail access into the fixed income asset class and allow investors to lower the risk of their portfolios by allocating funds further up the capital structure.  At present, ASX-Listed bank hybrids fit into the Tier 2 and Tier 1 categories while Corporate issued securities tend to be either Subordinated or Preference Shares. If transmutation were to occur, retail investors would gain greater access to the Senior Unsecured level of the capital structure. Senior Unsecured debt investors ranked ahead of all the levels mentioned in the priority of payments and are investors are essentially at lower risk of default. As a result, these types of securities are less volatile than most instruments currently trading on the ASX. As a result, the transmutation process would improve access, increase demand and make ASX200 companies think twice before issuing debt abroad. Alternatively, retail investors can access these types of securities through investment vehicles known as Exchange Traded Bonds (XTBs). There are currently 39 XTBs on issue and can be accessed through the ASX.

At present, ASX-Listed bank hybrids fit into the Tier 2 and Tier 1 categories while Corporate issued securities tend to be either Subordinated or Preference Shares. If transmutation were to occur, retail investors would gain greater access to the Senior Unsecured level of the capital structure. Senior Unsecured debt investors ranked ahead of all the levels mentioned in the priority of payments and are investors are essentially at lower risk of default. As a result, these types of securities are less volatile than most instruments currently trading on the ASX. As a result, the transmutation process would improve access, increase demand and make ASX200 companies think twice before issuing debt abroad. Alternatively, retail investors can access these types of securities through investment vehicles known as Exchange Traded Bonds (XTBs). There are currently 39 XTBs on issue and can be accessed through the ASX.

| Group | Ticker | Rated | Debt ($Am) | Bank Debt% | ASX Listed Debt% | Aus OTC Debt% | Overseas Debt% |

| AGL Energy | AGL | Yes | $3,129 | 46% | 21% | 19% | 14% |

| Alumina | AWC | Yes | $152 | 18% | 0% | 82% | 0% |

| APA Group | APA | Yes | $9,366 | 11% | 5% | 3% | 80% |

| Asciano | AIO | Yes | $3,839 | 16% | 0% | 9% | 75% |

| Ausnet Services | AST | Yes | $6,898 | 0% | 0% | 22% | 78% |

| BHP Billiton | BHP | Yes | $50,153 | 6% | 0% | 5% | 89% |

| BWP Trust | BWP | Yes | $480 | 58% | 0% | 42% | 0% |

| Caltex Australia | CTX | Yes | $694 | 0% | 78% | 22% | 0% |

| Coca Cola Limited | CCL | Yes | $2,536 | 8% | 0% | 6% | 86% |

| Crown Resorts | CWN | Yes | $3,064 | 25% | 37% | 24% | 14% |

| Dexus Property | DXS | Yes | $3,286 | 37% | 0% | 18% | 45% |

| Downer Edi | DOW | No | $646 | 6% | 0% | 72% | 23% |

| Duet Group | DUE | No | $6,201 | 56% | 0% | 31% | 13% |

| G8 Education | GEM | No | $535 | 0% | 0% | 22% | 78% |

| Goodman Group | GMG | Yes | $2,873 | 13% | 0% | 0% | 87% |

| GPT Group | GPT | Yes | $2,958 | 59% | 0% | 21% | 20% |

| Incitec Pivot | IPL | Yes | $2,252 | 45% | 0% | 9% | 46% |

| Investa Office Fund | IOF | Yes | $1,098 | 48% | 0% | 11% | 41% |

| Lendlease | LLC | Yes | $2,593 | 47% | 0% | 18% | 35% |

| Mirvac Group | MGR | Yes | $3,243 | 39% | 0% | 19% | 42% |

| Nufarm | NUF | Yes | $1,204 | 62% | 0% | 0% | 38% |

| Origin Energy | ORG | Yes | $9,488 | 7% | 9% | 0% | 84% |

| Qantas Airways | QAN | Yes | $5,244 | 77% | 0% | 18% | 5% |

| Ramsay Health Care | RHC | No | $3,367 | 92% | 8% | 0% | 0% |

| Scentre Group | SCG | Yes | $11,103 | 13% | 0% | 21% | 67% |

| Seven Group Holdings | SVW | No | $2,210 | 43% | 22% | 0% | 34% |

| Shopping Centres Australasia | SCP | No | $762 | 44% | 0% | 23% | 34% |

| Stockland | SGP | Yes | $3,677 | 4% | 0% | 19% | 77% |

| Sydney Airport | SYD | Yes | $8,181 | 18% | 0% | 35% | 47% |

| Tabcorp Holdings | TAH | Yes | $1,411 | 67% | 18% | 0% | 15% |

| Tatts Group | TTS | No | $933 | 45% | 21% | 0% | 34% |

| Telstra | TLS | Yes | $14,434 | 6% | 0% | 19% | 75% |

| Transurban | TCL | No | $12,194 | 27% | 0% | 10% | 63% |

| Vicinity | VCX | No | $4,717 | 56% | 0% | 22% | 23% |

| Wesfarmers | WES | Yes | $6,282 | 11% | 0% | 29% | 60% |

| Woolworths | WOW | Yes | $4,715 | 1% | 15% | 21% | 64% |

Source: Company Reports (last reporting date), BondAdviser Estimates