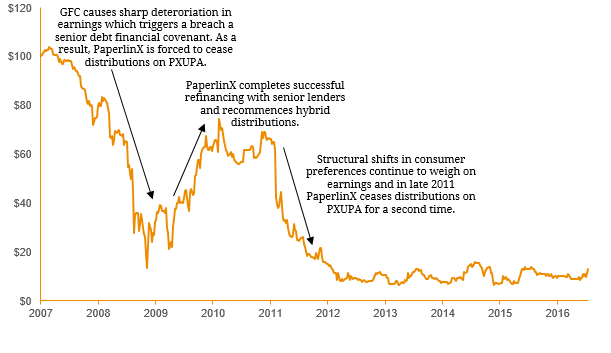

The PaperlinX story never ends and continues to find its way into the media. For those who do not know, the PaperLinX Step-Up Preference Securities (ASX: PXUPA) initially listed in March 2007 and has been one of the worst performing securities in the ASX-listed debt and hybrid market over the past decade. The underlying entity, PaperlinX Limited, was hit hard by the Global Financial Crisis and at the end of 2008 the company breached one of its financial covenants set by its senior lenders. As part of the waiver, PaperlinX was forced to cease distributions on PXUPA which recommenced a year later in 2010 following a successful refinancing. However, ongoing structural shifts in customer preferences (i.e. physical print to digital print) continued to weigh on earnings which forced management to book significant impairments. As many hybrids have option to defer distributions, issuers can decide to cease payments to solidify their financial positions in periods of distress. While this does not constitute default, it typically triggers a substantial sell-off in the underlying hybrid security, especially if payments are deferred for a prolonged timeframe. In 2011, PaperlinX ceased distributions on PXUPA for a second time which resulted in a significant fall in price. Figure 1. PXUPA Price History  Source: Bloomberg Figure 2. PaperlinX Limited (Spicers) Annual Revenue

Source: Bloomberg Figure 2. PaperlinX Limited (Spicers) Annual Revenue  Source: Company Reports While the hybrids are in place the company cannot issue new ordinary equity or pay dividends to existing shareholders. To resolve these complications and restructure the company, PaperlinX attempted to merge the company with the hybrid trust and simplify its capital structure but independent directors recommended against the transaction for the following reasons:

Source: Company Reports While the hybrids are in place the company cannot issue new ordinary equity or pay dividends to existing shareholders. To resolve these complications and restructure the company, PaperlinX attempted to merge the company with the hybrid trust and simplify its capital structure but independent directors recommended against the transaction for the following reasons:

- Continuing uncertainty relating to PaperlinX’s financial and operational positon

- The offer appears to be materially inadequate and the offer ratio is too low and unfair

- The offer does not compensate unitholders for unpaid distributions

- Value may be better reflected in the trust if and when PaperlinX delivers on turnaround strategy

- Offer unlikely to generate benefits unless there is high level of acceptances

As a result, only 7.8% of unitholders accepted PaperlinX’s takeover offer and over the next year, a number of international PaperlinX subsidiaries were either sold or b placed into voluntary administration. To avoid further reputational damage, shareholders of PaperlinX voted to change the company’s name to Spicers in October 2015. Last week, the newly named entity put forward a revised takeover offer to unitholders for 545 Spicers shares for every 1 PXUPA unit. This implies a valuation of $13.63 per hybrid (51.4% premium to the last closing price). Following this announcement, PXUPA has rallied significantly but by no means will unitholders agree to this proposal. Figure 2. PXUPA 2016 Price History  The ongoing battle between PaperlinX/Spicers shareholders and hybrid investors seems to keep going around in circles. The new deal will allow unitholders to receive 68.3% of the merged entity but will this be enough for shareholders to finally get hybrid investors over the line. Ultimately there are just too many parties with different interests and overall highlights the potential negative outcomes of a complicated and fragmented ownership structures due to restrictive conditions and clauses.

The ongoing battle between PaperlinX/Spicers shareholders and hybrid investors seems to keep going around in circles. The new deal will allow unitholders to receive 68.3% of the merged entity but will this be enough for shareholders to finally get hybrid investors over the line. Ultimately there are just too many parties with different interests and overall highlights the potential negative outcomes of a complicated and fragmented ownership structures due to restrictive conditions and clauses.