In a short but positive week for markets the ASX200 was up 141 points (2.91%) while the Bloomberg AUSBond Composite Index was up 0.45%. The big news of the week was the surprise decision by the Bank of Japan (BOJ) on Friday to cut its benchmark interest rate to -0.1%. This is supposed to combat deflation with Governor Kuroda saying that ‘the minus interest rate combined with quantitative easing ….. can support companies and individuals in breaking their deflationary mindset’. The truth is the BOJ is actually introducing a tiering system, in which only a portion of deposits will be subject to negative rates and only a small balance of funds will fall into the affected tier. This is a one of the very few options the Japanese have to combat low inflation as the current bond buying program is facing some technical difficulties which arguably makes its purpose redundant. The move came 18 months after the European Central Bank became the first major central bank to venture below zero and is now expected to cut its rate further (already at -0.30%) in March 2016. This will only increase the pressure on the global central banks’ race to devalue currencies. In the listed market the volatility in corporate hybrids continues. Origin Energy Subordinated Notes (ASX Code: ORGHA) hit an an intraday low of $90 (~19% yield to call) and then jumped back up to a high of 96.30 (11.5% yield to call). This was following a series of announcements from the issuer, rating agencies and ongoing volatility in the underlying oil price. The big question with this security remains the confidence in the issuer executing its call option at the end of this year. Origin’s stance is that it remains committed to calling the security but this is subject to a number of factors beyond their control. The rating agencies (Moody’s likely to act first) are key and if they downgrade Origins’ credit rating to junk the ‘knock on’ effects to financiers and the Australian Energy Regulator will determine the internal capital planning of the group and in turn its commitment to calling the security. Crown Resorts Subordinated Notes (both I & II) also experienced some intraday volatility last week with CWNHB hitting intraday low of $69.50 (~15% yield to call) and highs of $76 (~12.8% yield to call). This volatility stemmed from the AFR article which suggested Packer was in discussions with Blackstone Real Estate about taking the company private (or some of its assets). The sell-off has been driven by which assets are potentially left in the listed entity if he does takes the better performing assets private. There are change of control clauses within the security documentation, but these are only partially protective for the investor (margin step up rather than a put option for holders) in the event that Packer sells his stake. The biggest issue remains the uncertainty surrounding credit metrics of the issuer (post any changes to assets) and whether or not this will cause a breach of mandatory deferral triggers (Max. Leverage Trigger 5.0x vs 2.8x Reported, Min Interest Cover Trigger 5.7x vs 2.5 Actual). In other corporate news, Standard and Poors (S&P) placed Asciano’s credit rating negative on CreditWatch last week after the Qube led consortium tabled an offer for the company. If the transaction proceeds as discussed Asciano’s business diversity will weaken as will its key credit metrics. Separately, NEXTDC also announced last week a further increase in its contracted utilisation with an existing customer taking a further 2MW of capacity for a term of five years.

Reporting Season Reporting season in Australia kicks off this week with Tabcorp, Macquarie and Genworth of interest to us. The focus remains squarely on asset quality, capital planning and outlook for the banks but we should also see some writedowns from oil producers. 4/02/2016 – Macquarie Group Trading Update 4/02/2016 – Tabcorp (1H16) 5/02/2016 – Genworth (FY15) 10/02/2016 – AGL (1H16) 10/02/2016 – Commonwealth Bank (1H16) 11/02/2016 – Goodman (1H16) 11/02/2016 – Mirvac (1H16) 11/02/2016 – Suncorp (1H16) 11/02/2016 – Transurban (1H16) The US reporting season continues to give us some insight into the upcoming results. Caterpillar demonstrated last week the difficult current operating environment with revenue down 23% on previous quarter as demand fell significantly across all divisions. The outlook for the group was also negative and this doesn’t bode well for Seven Group (WesTrac subsidiary) this reporting season. Click below for Interactive Charts Chart 1: Bloomberg AUSBond Composite Index (Monthly) Chart 2: Bonds vs Equities 2014/15 (Monthly)

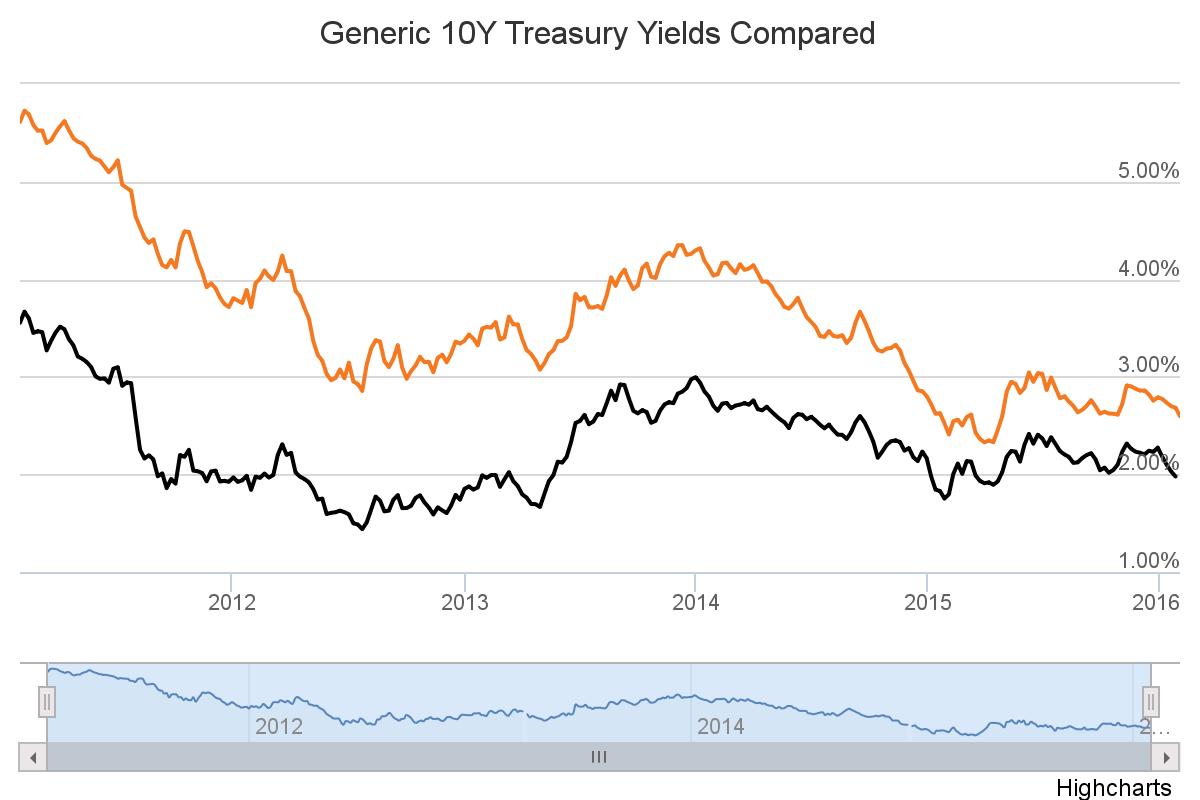

Interest Rates Last week equity markets in the US jumped on the bond market bandwagon and became confident interest rate rises by the Federal Reserve in 2016 and 2017 will be more restrained than the Fed had originally predicted in December 2015. Yellen’s change of tact is seemingly in response to market movements and she is no longer as definitive about predictions of higher interest rates, despite nothing really changing in the base US economy. This news (in combination with further QE) also suggests that the yield curve is likley to remain fairly flat in 2016 with broad market stability being a precedent to any steepening. Last week in Australia the inflation data was released and although the headline rate (1.7%) was still below the RBA target range it was above expectations and sign of improvement were beginning to rise with the rise in the prices of tradable goods accelerating to 0.8% year on year from -0.3% in the third quarter. The pickup is primarily related to the drop in the Australian dollar and further benefits should be seen in coming quarters due to a 26% drop in oil prices since the end of November (this is a timing effect of inflation data). In our opinion this should mean the Reserve Bank maintains its current position at tomorrows meeting. We will get further insight into the RBA’s thinking on Friday when the quarterly Statement on Monetary Policy is released as it will include updated forecasts on economic growth and inflation. In February, the 10-year bond yield hit an all-time low of 2.27% before lifting to highs near 3.15% on June 11. In early November 2015 there was a progressive increase in yield from ~2.60% to a high of 2.99%. However, since mid December the flight to quality has meant the 10Y yield has given back the changes in Q4 2015 and is now right back to 2.61%. The 3-year bond has followed a similar pattern and broke out of its recent yield range (1.90 – 2.1%) in November/December 2015 reaching a high of 2.18% on 7 December 2015 but is now back to 1.85%. On 29 January 2016, the ASX 30 Day Interbank Cash Rate Futures February 2016 contract was trading at 98.015 indicating a 6% expectation of an interest rate decrease to 1.75% at the next RBA Board meeting (down from 19% the previous week).

Interactive Charts Below

Interactive Charts Below