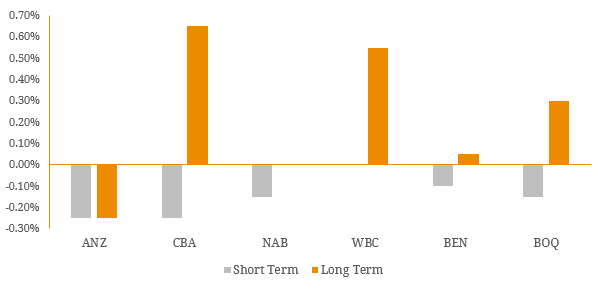

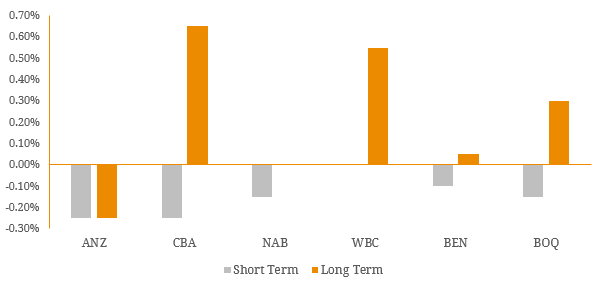

Last month, the Reserve Bank of Australia (RBA) cut the official cash rate by 0.25% to 1.50% with many Australian banks deciding not to pass on the full rate cut to mortgage holders and instead partially maintaining (and in some cases improving) some term deposit rates. In response to media criticism the banks cited regulatory reasons for these actions but what does this actually mean? During the Global Financial Crisis (GFC), several global banks suffered a liquidity crisis due to their over reliance on short-term wholesale funding and interbank lending markets. As confidence evaporated during this period, banks were unwilling to lend to each other and these credit markets effectively dried up forcing some financial institutions to collapse. As part of the banking regulation overhaul (known as Basel III), two primary liquidity measures were proposed, the Liquidity Coverage Ratio (LCR) which has been implemented (January 2016) and the Net Stable Funding Ratio (NSFR) which is yet to be implemented. The NSFR calculates the proportion of long-term assets which are funded by “stable funding”. This type of funding includes customer deposits, long term wholesale funding and equity and excludes short-term wholesale funding. As a result, the ratio allows regulators to measure individual banks reliance of short term interbank funding markets to prevent a similar liquidity crisis experienced during the GFC. The Australian Prudential Regulation Authority (APRA) has a planned implementation date of the 1st of January 2018 in which 15 of Australia’s largest banks will have to have a NSFR greater than 100%. As a result, many banks are beginning to work towards this regulatory hurdle and are maintaining/improving term deposit rates to remain attractive to investors in an already highly competitive market. However, this has mainly been applied to longer term deposits (i.e. 1 year and beyond) to ensure a greater degree of stability in deposit funding. As Figure 1 depicts below, the majority of Australian banks passed on most of rate cut to short term deposits rate (~3 months) but actually increased longer term rates (~12 months). Figure 1. Change in Term Deposit Rates After August’s Cash Rate Cut  Source: Company Reports, BondAdviser Note: Short Term ~1-3 months, Long Term ~9-12 months This is further reiterated by retail deposit data supplied by the RBA where 1 Year and 3 Year term deposit spreads have increased significantly relative to short term rates post the rate cut. This has resulted in a steepening of the term deposit curve as displayed in figure 4. We can expect this to continue if further cash rate cuts are made by the RBA in 2017 closer to the NSFR implementation date (1 January 2018). Figure 2. Term Deposit Rate Change in Credit Spread After August’s Cash Rate Cut

Source: Company Reports, BondAdviser Note: Short Term ~1-3 months, Long Term ~9-12 months This is further reiterated by retail deposit data supplied by the RBA where 1 Year and 3 Year term deposit spreads have increased significantly relative to short term rates post the rate cut. This has resulted in a steepening of the term deposit curve as displayed in figure 4. We can expect this to continue if further cash rate cuts are made by the RBA in 2017 closer to the NSFR implementation date (1 January 2018). Figure 2. Term Deposit Rate Change in Credit Spread After August’s Cash Rate Cut  Source: RBA, BondAdviser Figure 4. Term Deposit Rates Steepening

Source: RBA, BondAdviser Figure 4. Term Deposit Rates Steepening  Source: RBA, BondAdviser Ultimately, the current state of the deposit market is a result of growing regulatory pressure in the Australian banking system. APRA is continuing to push banks back into traditional funding sources (such as household deposits) in an attempt to reduce the major banks’ reliance on offshore channels. This is consistent with our view that the Australian banking system is in a transitional period regarding regulation and this should ultimately lead to less leverage and more risk controls. Overall, this is a positive for fixed income investors across the bank capital structure (including term deposit holders) and given the NSFR we believe term deposits should remain somewhat supported against the ‘lower for longer’ interest rate environment.

Source: RBA, BondAdviser Ultimately, the current state of the deposit market is a result of growing regulatory pressure in the Australian banking system. APRA is continuing to push banks back into traditional funding sources (such as household deposits) in an attempt to reduce the major banks’ reliance on offshore channels. This is consistent with our view that the Australian banking system is in a transitional period regarding regulation and this should ultimately lead to less leverage and more risk controls. Overall, this is a positive for fixed income investors across the bank capital structure (including term deposit holders) and given the NSFR we believe term deposits should remain somewhat supported against the ‘lower for longer’ interest rate environment.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.