In a recent independent report written by the Australian Centre of Financial Studies and Monash Business School, investment options for those close to retirement were examined against the backdrop of a low-return investment environment. As the ‘baby boomers’ approach the end of their working lives, there is growing concern current low rates of return will be insufficient in providing retirement income. We note a number of key assumptions were made regarding wages, inflation, transaction costs and policy settings. Key findings:

- On average, Australians are increasing their net wealth over time but there is notable variations between age groups.

- Superannuation is the second-largest store of wealth among Australians after the primary residence.

- Soon-to-be retirees may be carrying unnecessary levels of risk in their investment portfolios represented by a relatively high weighting to equities.

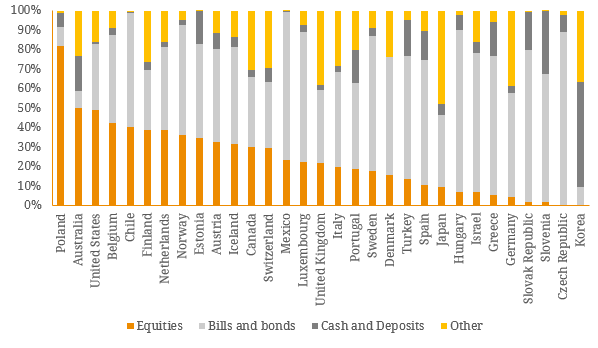

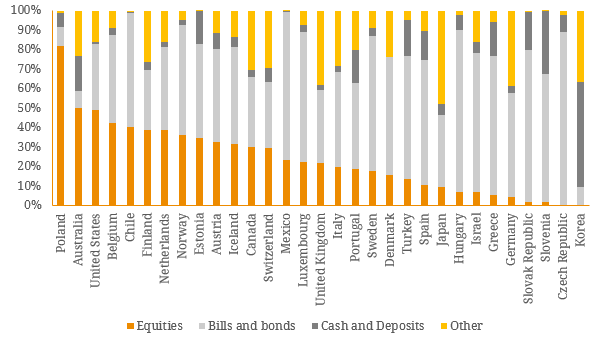

It is the third finding we believe to be of most interest. According to the Australian Prudential Regulation Authority (APRA), superannuation funds were invested approximately 50% in equities as of March 2016. This is the second highest equity weighting among global OECD pension systems, behind Poland. Figure 1. Pension fund asset allocation in selected OECD countries (2014)  Source: OECD Global Pension Statistics For Australians within 10 years of retirement, this significantly increases the risk of capital losses. While many investors will argue that fixed income returns are insufficient, the report highlighted that it is difficult for these households to now improve their financial wealth by 65. This suggests Australians close to retirement should prioritise capital preservation over wealth accumulation due to sequencing risk. Sequencing risk is the risk of retiring in a period of suppressed economic and investment environment such as the Global Financial Crisis (GFC). Australians close to retiring during this period suffered massive reductions in wealth and were forced to delay retirement. It goes without saying, this impact would have been less for those with a smaller allocation to equities relative to less volatile assets such as fixed income. Figure 2 demonstrates the difficulty for soon-to-be retirees to improve their wealth via strategic asset allocation. Figure 2. Median project inflation-adjusted financial wealth at retirement for 55-59 age group

Source: OECD Global Pension Statistics For Australians within 10 years of retirement, this significantly increases the risk of capital losses. While many investors will argue that fixed income returns are insufficient, the report highlighted that it is difficult for these households to now improve their financial wealth by 65. This suggests Australians close to retirement should prioritise capital preservation over wealth accumulation due to sequencing risk. Sequencing risk is the risk of retiring in a period of suppressed economic and investment environment such as the Global Financial Crisis (GFC). Australians close to retiring during this period suffered massive reductions in wealth and were forced to delay retirement. It goes without saying, this impact would have been less for those with a smaller allocation to equities relative to less volatile assets such as fixed income. Figure 2 demonstrates the difficulty for soon-to-be retirees to improve their wealth via strategic asset allocation. Figure 2. Median project inflation-adjusted financial wealth at retirement for 55-59 age group  Source: Australian Centre of Financial Studies What happens over the longer term? The study simulated three asset allocation scenarios – 100% equities, 100% fixed income or a 50/50 split between the asset classes – and found that wealth accumulation is driven by Superannuation contributions and long-run compounding rather than asset class weightings. In other words, consistent contributions have a greater impact on retirement wealth relative to cyclical investment returns. Figure 3. Projected median inflation-adjusted financial wealth at retirement for different age groups

Source: Australian Centre of Financial Studies What happens over the longer term? The study simulated three asset allocation scenarios – 100% equities, 100% fixed income or a 50/50 split between the asset classes – and found that wealth accumulation is driven by Superannuation contributions and long-run compounding rather than asset class weightings. In other words, consistent contributions have a greater impact on retirement wealth relative to cyclical investment returns. Figure 3. Projected median inflation-adjusted financial wealth at retirement for different age groups  Source: Australian Centre of Financial Studies Overall, this recent report reflects the current state of the Australian investment market. While the retirement risk zone (ages 55 and above) should reduce their holdings of risky assets such as equities in order to inhibit sequencing risk, the undeveloped Australian fixed income market (relative to other countries) impedes this. The current superannuation pool is estimated to be around $2 trillion but retail access to fixed-income products is minimal which is further exacerbated by many Australian companies preferring to issue debt offshore. As a result, portfolio optimisation and dynamic asset allocation is challenging. While legislative reforms and innovative investment structures are improving Australian fixed income, the retail market still remains relatively small and a major downturn in Australian equities may be needed before investors become aware that capital preservation (contributions) is equally, if not more, important than wealth accumulation.

Source: Australian Centre of Financial Studies Overall, this recent report reflects the current state of the Australian investment market. While the retirement risk zone (ages 55 and above) should reduce their holdings of risky assets such as equities in order to inhibit sequencing risk, the undeveloped Australian fixed income market (relative to other countries) impedes this. The current superannuation pool is estimated to be around $2 trillion but retail access to fixed-income products is minimal which is further exacerbated by many Australian companies preferring to issue debt offshore. As a result, portfolio optimisation and dynamic asset allocation is challenging. While legislative reforms and innovative investment structures are improving Australian fixed income, the retail market still remains relatively small and a major downturn in Australian equities may be needed before investors become aware that capital preservation (contributions) is equally, if not more, important than wealth accumulation.