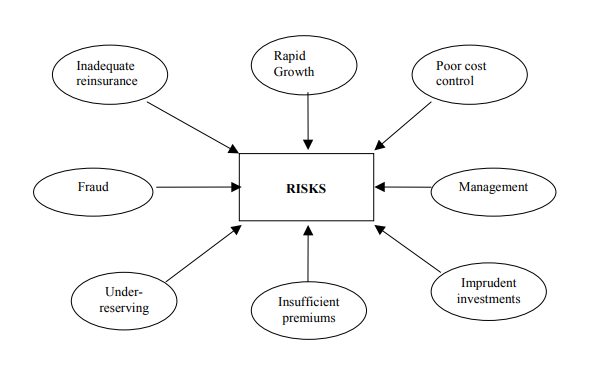

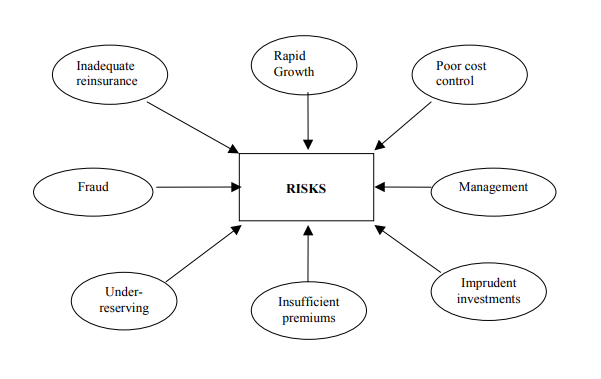

CBL Insurance (CBL) is the largest and oldest provider of credit surety and financial risk insurance in New Zealand and has been operating for over 40 years. CBL provides a range of property-related insurance and reinsurance products. Although based in New Zealand, it has an extensive international presence in Europe, Malaysia and Latin America. CBL is not rated by the major ratings agencies, although the company had been rated by A.M. Best at B++ (Good) until early February 2018. On 8 February 2018, shares of CBL was suspended following concerns from the Financial Markets Authority New Zealand, Reserve Bank of New Zealand, and a number of overseas regulators with prudential oversight of CBL’s international insurance business, on whether the company has given complete and true material information to the market. On 23 February 2018, the high court of New Zealand ordered CBL Insurance to be put into interim liquidation, after the company made payments of $55 million in breach of directions by the regulator. The payments to overseas companies were made in the context of significant doubts about CBL Insurance’s solvency and without RBNZ’s prior approval as the payments may provide some creditors of CBL insurance with an advantage over other creditors. Even as recently as 30 June 2017, in its solvency disclosure submission to RBNZ, CBL’s Actual Solvency Capital was 132% of the minimum requirement set by RBNZ, although it was down from 189% in 31 Dec 2016. RBNZ later raised CBL’s minimum solvency ratio to 170%, making it, on paper, insolvent from a regulatory perspective. Although some further details will likely become clearer, it appears that CBL’s woes stemmed from its French construction insurance business, which consumed a high level of capital for a long time and involved significant estimations of future claims by independent actuaries – a disproportionate risk for the group as it turned out. CBL only bought into the French operations in January 2017 through a NZ$150 million acquisition of a 71% stake. CBL had hoped the acquisition would provide it with stronger market positions in Europe but it became apparent that reality was very different only a year post the acquisition. CBL warned of a loss of between $75 million and $85 million in calendar 2017 and said it would need to make a $100 million adjustment to strengthen the future claims reserve for the French unit and would write off $44 million of receivables from broker/insurer/reinsurer reconciliations, prompting a credit downgrade by A.M Best and a prospective capital raising to plug the reserve hole. Figure 1: Key Factors Behind Insolvency of Non-Life Insurers  Source: BondAdviser Whilst the reasons for insurer failures are many (Figure 1), CBL’s case appears to be rooted in its rapid expansion, poor forecasts of claim events and delegated underwriting for which it had little control over standards. Solvency could be easily put at risk by drops in asset values too, although in this particular instance, it doesn’t appear to be an asset issue. It turns out that CBL’s French misadventure is not its first – from 2005 to 2007, CBL faced issues with regulators in the US state of Georgia that ultimately resulted in it returning premiums and being banned from operating in the US for 10 years. Later in 2015, CBL used its IPO proceeds to acquire an Australian insurer. The company had over the years expanded into so many overseas markets such that only 1% of premiums originated from its home base of New Zealand. This should perhaps have rung alarm bells for stakeholders. The company had effectively abandoned its most-familiar home market of New Zealand and transformed into an international business in far-flung jurisdictions normally reserved for much larger and more experienced insurers like AXA, Zurich and Prudential. Questions should certainly have been raised around whether CBL had the expertise to manage such a diverse operation across jurisdictions. CBL’s troubles illustrate that, apart from the usual risk assessment tools at investors’ disposal, sometimes a commonsense check on the ambitions of management can be just as important for prudent investors and particularly so for Australian and New Zealand entities expanding offshore.

Source: BondAdviser Whilst the reasons for insurer failures are many (Figure 1), CBL’s case appears to be rooted in its rapid expansion, poor forecasts of claim events and delegated underwriting for which it had little control over standards. Solvency could be easily put at risk by drops in asset values too, although in this particular instance, it doesn’t appear to be an asset issue. It turns out that CBL’s French misadventure is not its first – from 2005 to 2007, CBL faced issues with regulators in the US state of Georgia that ultimately resulted in it returning premiums and being banned from operating in the US for 10 years. Later in 2015, CBL used its IPO proceeds to acquire an Australian insurer. The company had over the years expanded into so many overseas markets such that only 1% of premiums originated from its home base of New Zealand. This should perhaps have rung alarm bells for stakeholders. The company had effectively abandoned its most-familiar home market of New Zealand and transformed into an international business in far-flung jurisdictions normally reserved for much larger and more experienced insurers like AXA, Zurich and Prudential. Questions should certainly have been raised around whether CBL had the expertise to manage such a diverse operation across jurisdictions. CBL’s troubles illustrate that, apart from the usual risk assessment tools at investors’ disposal, sometimes a commonsense check on the ambitions of management can be just as important for prudent investors and particularly so for Australian and New Zealand entities expanding offshore.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.