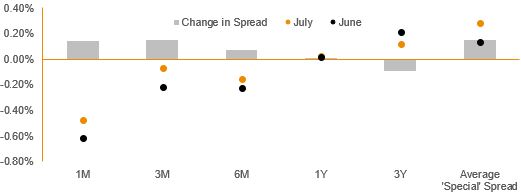

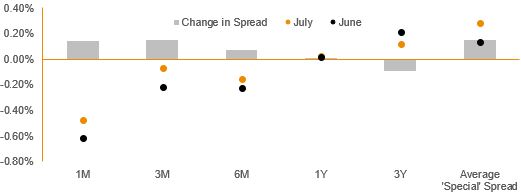

Globally, the US-China trade war rages on with US President Donald Trump threatening additional tariff measures on a further $US200 billion of Chinese imports as tensions continue to soar. However, US-European relations have improved with both parties agreeing to work together to avert a trade war. Meanwhile, it is widely anticipated that the Fed will keep rates on hold at its end of month meeting after a 25bps rate hike to 1.75% last month. On the domestic front, the RBA has unsurprisingly left the official cash rate on hold at 1.50%, with a below consensus core inflation figure of 2.1% indicating this may be the case for the foreseeable future. Low wage growth is expected to continue over the short-term horizon due to spare capacity in the labour market and Dealogic data indicates the housing market is cooling at the fastest rate since February 2009. As monetary policy between the Fed and RBA continues to diverge, the spread between each country’s respective 10-year Treasury yields has widened to 31bps. The swap curve has seen tightening across all short-term tenors after ballooning last month. With Term Deposit (TD) offerings continuing to reflect the stance of the RBA, the tightening spread in Figure 1 below is primarily a function of movements in the swap curve. Figure 1. Term Deposit Spread Over Relevant BBSW: July 2018 v June 2018  Source: RBA, BondAdviser For full details, charts and commentary, please click here for the full pdf version.

Source: RBA, BondAdviser For full details, charts and commentary, please click here for the full pdf version.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.