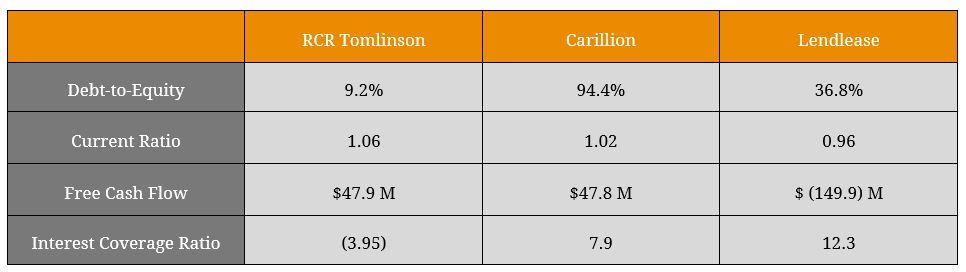

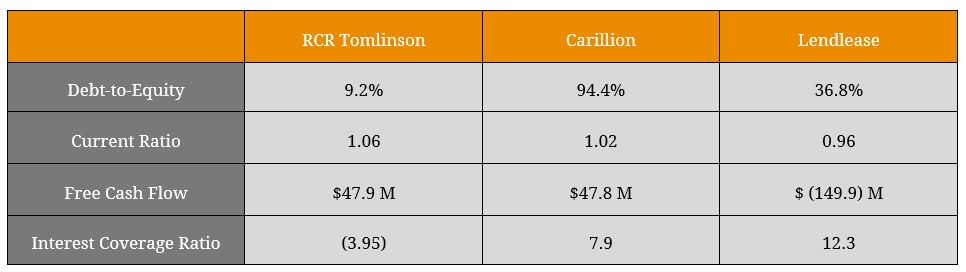

The collapse of engineering group RCR Tomlinson (ASX: RCR) into administration on 23 November capped a remarkable fall for one of the oldest engineering contractors in the country. However, whilst the appointment of administrators, that are set to carve up and sell off parts of the ailing business, surprised many in the market, company collapses in the construction industry are neither unique nor unlikely. In the same month, the much larger and venerable property developer/ construction company Lendlease (ASX: LLC) announced a $350 million writedown on several current projects including Sydney’s NorthConnex due to poor weather and lower labour productivity as it announced a review of its “risk appetite” for infrastructure projects and potential sale of its engineering business altogether. Further abroad, U.K. facilities management and construction services conglomerate Carillion (LSE: CLLN) was subjected to a similar fate at the start of 2018 when it was placed into compulsory liquidation amid rising debt and compressed profitability margins (figure 1). So how did Carillion, a company employing 43,000 people worldwide, with revenues of £5.2 billion (A$8.9 billion) in 2016 and significant government contracts fall so hard, so quickly and why are we seeing the same concerning trend start to appear on our doorstep? Figure 1. Historical Share Prices of Selected Construction and Engineering Firms  Source: BondAdviser, Bloomberg As seen in figure 1 above, in each instance, the trigger for a large adverse equity market reaction has been an unexpected and significant writedown in the value of current projects with fears of more bad news to come. Whilst share price reactions proved to be a leading indicator for both RCR Tomlinson and Carillion (figure 1 above) the same indicators of distress are not as prominent for investors analysing core solvency and liquidity metrics of the companies at the same time (figure 2). Figure 2. Key Credit Metrics by Company

Source: BondAdviser, Bloomberg As seen in figure 1 above, in each instance, the trigger for a large adverse equity market reaction has been an unexpected and significant writedown in the value of current projects with fears of more bad news to come. Whilst share price reactions proved to be a leading indicator for both RCR Tomlinson and Carillion (figure 1 above) the same indicators of distress are not as prominent for investors analysing core solvency and liquidity metrics of the companies at the same time (figure 2). Figure 2. Key Credit Metrics by Company  Source: BondAdviser, Bloomberg The key factor linking all of these engineering and construction companies is project risk. In the tender process for major government infrastructure works, Carillion and RCR Tomlinson were awarded the contracts based on their reputation and, critically, their competitive price. Concentration in these industries and the attractiveness of major government contracts places downward pressure on margins and can ultimately lead to wafer-thin levels of profitability and minimal company equity buffers for the performance of the contracts as excess cash is frittered away as dividends. Figure 3 below summarises some of the key risks in the construction and engineering industries which combined, represent the project risk for developers and builders such as RCR Tomlinson, Carillion and Lendlease. Figure 3. Components of Project Risk

Source: BondAdviser, Bloomberg The key factor linking all of these engineering and construction companies is project risk. In the tender process for major government infrastructure works, Carillion and RCR Tomlinson were awarded the contracts based on their reputation and, critically, their competitive price. Concentration in these industries and the attractiveness of major government contracts places downward pressure on margins and can ultimately lead to wafer-thin levels of profitability and minimal company equity buffers for the performance of the contracts as excess cash is frittered away as dividends. Figure 3 below summarises some of the key risks in the construction and engineering industries which combined, represent the project risk for developers and builders such as RCR Tomlinson, Carillion and Lendlease. Figure 3. Components of Project Risk  Source: BondAdviser The lesson here for all investors is that of leading and lagging indicators. As competition increases, construction and engineering firms such as RCR Tomlinson are forced to lower their tender prices in a bid to increase their chances of being awarded the contract. These low profit margins, combined with the long-term timeframe and significant scale of operations required for these contracts, requires these entities to have robust risk management and project management expertise available for delivering the contract. In the case of RCR Tomlinson, the company took a risk and committed to establishing itself as a leading engineering, procurement and construction management (EPCM) firm in the renewable energy space, having traditionally been involved in mining engineering. Whilst this may have been good from a revenue diversification and growth opportunity perspective, ultimately it appears that a lack of specific expertise in the renewable energy space and labour shortages in the industry increased project risk and was a major contributing factor in the Group’s demise. In the event of delays or cost blowouts on individual projects, thin equity buffers and potentially significant compensation claims from clients can, in aggregate, create a significant (and largely hidden) additional risk to investors. Whilst our longstanding Sell recommendation on Lendlease’s 6.00% 2020 bonds is based on a number of factors, a late-cycle construction industry combined with forecast high government infrastructure investment could prove to be a sour cocktail of low profitability and heightened project risk in the industry as a whole, and for this reason we remain wary of further credit investment in the sector at current spread levels.

Source: BondAdviser The lesson here for all investors is that of leading and lagging indicators. As competition increases, construction and engineering firms such as RCR Tomlinson are forced to lower their tender prices in a bid to increase their chances of being awarded the contract. These low profit margins, combined with the long-term timeframe and significant scale of operations required for these contracts, requires these entities to have robust risk management and project management expertise available for delivering the contract. In the case of RCR Tomlinson, the company took a risk and committed to establishing itself as a leading engineering, procurement and construction management (EPCM) firm in the renewable energy space, having traditionally been involved in mining engineering. Whilst this may have been good from a revenue diversification and growth opportunity perspective, ultimately it appears that a lack of specific expertise in the renewable energy space and labour shortages in the industry increased project risk and was a major contributing factor in the Group’s demise. In the event of delays or cost blowouts on individual projects, thin equity buffers and potentially significant compensation claims from clients can, in aggregate, create a significant (and largely hidden) additional risk to investors. Whilst our longstanding Sell recommendation on Lendlease’s 6.00% 2020 bonds is based on a number of factors, a late-cycle construction industry combined with forecast high government infrastructure investment could prove to be a sour cocktail of low profitability and heightened project risk in the industry as a whole, and for this reason we remain wary of further credit investment in the sector at current spread levels.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.