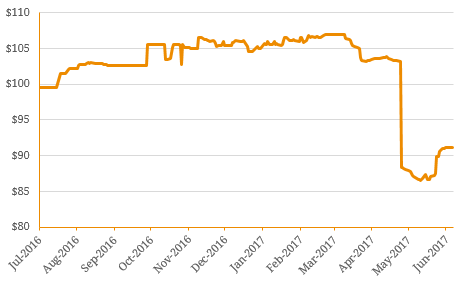

At the end of May 2017, sandalwood farming company Quintis Limited (ASX: QIN) was downgraded by Standard & Poor’s into the rarely seen ‘C’ section of the credit rating spectrum indicating immediate danger of credit default. Quintis (which formerly traded as Tree Management Services) is the world’s biggest owner and manager of Indian sandalwood which is a timber used in perfume and incense. The trouble started in March 2017 when US activist fund Glaucus Research began aggressively short-selling the company’s stock questioning management’s production figures and forecasts. While this was initially speculation, the credit rating agencies soon added to this negative sentiment citing uncertainty over the resignation of the company’s managing director and failure of Quintis’ largest customer to place any orders in 2017. Sale delays continued and as a result, a myriad of credit rating downgrades occurred in the months that followed with S&P stating it “believes it will be more challenging for the company to attract investor inflows (through its agriculture managed investment scheme) over the last two weeks of June, when typically, most investor cash flows occur. Should all these events transpire, we believe the company will face significant liquidity pressure.” Figure 1. Historical Price History of Quintis Secured USD 8.85% 2023 Notes  Source: Bloomberg The company has had its shares in suspension since the 17th of May amidst desperate attempts to recapitalise the business. The company experienced its latest credit rating downgrade on the 23rd of June by S&P to CCC- as Quintis fast approaches itss next interest payment on its senior secured notes (scheduled for the 1st of August 2017). Figure 2. Quintis Credit Rating Action

Source: Bloomberg The company has had its shares in suspension since the 17th of May amidst desperate attempts to recapitalise the business. The company experienced its latest credit rating downgrade on the 23rd of June by S&P to CCC- as Quintis fast approaches itss next interest payment on its senior secured notes (scheduled for the 1st of August 2017). Figure 2. Quintis Credit Rating Action  Source: S&P, Moody’s The latest trading update by Quintis at the beginning of June highlighted the concerning issues embroiling the company. Following management’s belated announcement that it lost a major customer contract in which the board claimed it was “unaware”, the company reduced its $45-55 million revenue guidance (which it signalled back in February) to $25-35 million. As a result of this inaction, several law firms are now exploring class actions on behalf of shareholders as Quintis was in clear violation of ASX disclosure procedures. Further adding to Quintis’ financial woes is its outstanding put options incorporated in the company’s agricultural managed investment scheme. Under this agreement, investors can elect to sell their trees back to the group at the lower of market value or a predetermined price. According to S&P, the next potential exercise date for one of these put options is in July 2017 putting additional liquidity pressure on Quintis. Overall, Quintis demonstrates that looks can be deceiving. While the board continues to believe it has avoided wrongdoing, both bond and equity investors have experienced significant capital losses due to the company’s disclosure failure. To avoid credit default, the company will need to disclose quarterly financial statements before the 8th of July 2017 but we expect the figures will just confirm the earnings deterioration. Although we believe there is more to story given the mysterious and sudden departure of the managing director before the lost contract was made public, investors will need to wait for more information but if history is anything to go by, speculation has held true in the case of Quintis.

Source: S&P, Moody’s The latest trading update by Quintis at the beginning of June highlighted the concerning issues embroiling the company. Following management’s belated announcement that it lost a major customer contract in which the board claimed it was “unaware”, the company reduced its $45-55 million revenue guidance (which it signalled back in February) to $25-35 million. As a result of this inaction, several law firms are now exploring class actions on behalf of shareholders as Quintis was in clear violation of ASX disclosure procedures. Further adding to Quintis’ financial woes is its outstanding put options incorporated in the company’s agricultural managed investment scheme. Under this agreement, investors can elect to sell their trees back to the group at the lower of market value or a predetermined price. According to S&P, the next potential exercise date for one of these put options is in July 2017 putting additional liquidity pressure on Quintis. Overall, Quintis demonstrates that looks can be deceiving. While the board continues to believe it has avoided wrongdoing, both bond and equity investors have experienced significant capital losses due to the company’s disclosure failure. To avoid credit default, the company will need to disclose quarterly financial statements before the 8th of July 2017 but we expect the figures will just confirm the earnings deterioration. Although we believe there is more to story given the mysterious and sudden departure of the managing director before the lost contract was made public, investors will need to wait for more information but if history is anything to go by, speculation has held true in the case of Quintis.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.