In Australia, the fixed income market, especially the exchange-traded part that is available to retail investors, is dominated by well-established, household name issuers such as the major banks and other large financial services companies. Whilst retail investors are usually quick to identify an issuance from a household name issuer, many, if not all, tend to overlook a fundamental question: Who exactly is the issuer? Are you really as familiar with the issuer as you think you are? Given that the issuer is ultimately the entity you are lending your money to and which will ultimately be responsible for your coupon and principal repayments, it would be prudent to have a complete understanding of this seemingly trivial issue. More seasoned investors would not be unfamiliar with the term Non-Operating Holding Companies (NOHCs) but it is by no means an everyday term in fixed income parlance. Thankfully, it is also not too difficult to find examples of such. Most recently, Macquarie (as most retail investors would generally, and simply, refer to the company) was in the market issuing a new Tier 1 instrument – Macquarie Group Capital Notes 3, potentially raising up to $1 billion from retail and institutional investors. The legal issuer is Macquarie Group Limited, as opposed to “Macquarie the bank”, which most retail investors tend to assume. It also may not be immediately obvious to many retail investors that “Macquarie” is a lot more than just “Macquarie the bank”. In fact, the legal issuer in this case, Macquarie Group, a typical Non-Operating Holding Company, is a collection of all of the business activities of “Macquarie”, and one that is a lot more complex than “Macquarie the bank”. Lending money to Macquarie Group carries very different risk-return profiles than lending to Macquarie Bank (the main operating and regulated entity). In Australia, NOHCs tend to be prevalent amongst financial services organisations regulated and authorised by the prudential regular APRA, under the Banking Act, the Insurance Act and the Life Insurance Act respectively, as shown in Table 1 below. Organisations wishing to establish NOHCs need to apply to APRA and meet specific requirements. Table 1. APRA-Authorised Non-Operating Holding Companies (under)  Note: highlighted are names covered by BondAdviser Source: APRA The primary function of NOHCs is to invest in its subsidiaries which are the main operating entities and that carry out the day-to-day business activities of the group that NOHCs themselves do not usually get involved in. NOHCs instead lend initial or ongoing financial support via cash reserves or stock sales and may assist in restructuring the operational model to ensure ongoing viability. NOHCs are normally structured as corporations to protect assets, absorb financial losses and limit liability. Operating companies are owned by NOHCs, and their net profits after expenses are paid to NOHCs as dividends. NOHCs are however allowed to conduct certain, although limited, business activities such as issuing own debt — especially if they are profitable from operating company dividends. From a fixed income investor’s perspective, NOHCs represent a rather unique risk-return profile. Fundamentally, the source of repayment of a bond issued by a NOHC do not come from day-to-day operating income of the main operating entities, but rather indirectly from the dividends paid by operating entities. In a distressed scenario, this also means that NOHC bond investors usually get repaid from the residual profits after creditors of operating entities have been satisfied – a form of structural subordination, which is an extra risk for investors. Secondly, the capital requirements of operating entities and NOHCs are different under APRA rules. The two are required to separately hold adequate capital, and that capital impost contains different terms. For example, in the aforementioned “Macquarie” example, Macquarie Bank Limited (the operating entity) is subject to APRA’s prudential capital adequacy requirements applicable to all ADIs, and capital instruments issued by Macquarie Bank Limited (and other comparable operating entities) usually contain both CET1 capital and non-viability trigger terms. Whereas capital instruments issued by Macquarie Group Limited (the NOHC), contains only the non-viability term, despite the fact that the proceeds of NOHC-issued instruments may be channelled to operating entities to support operations via parent-subsidiary transactions. Investors to Macquarie Group thus face the possibility of effectively lending funds to Macquarie bank yet ranking behind Macquarie bank investors in a non-viability event, albeit having a theoretical immunity from a capital trigger event which would be applicable only to Macquarie bank investors. We note that there are many possible nuances arising from the group structure and in a stress scenario, all securities are likely to suffer price pressure. Lastly, the upstreaming of dividends from operating entities to NOHCs are usually subject to approval by APRA, which may or may not be given if APRA deems the operating entities as being in distress. Mitigating the risks, investors of NOHC debts do benefit from diversity of earnings – a group such as Macquarie has multiple revenue streams from multiple operating entities which may include an ADI, a wealth management arm, a capital-light advisory business and a proprietary trading arm. As a result, investors of NOHCs get exposure to the entire business risks of the group, rather than that of a stand-alone operating entity (usually the bank). In this respect, NOHCs offer an appealing exposure to certain cohorts of investors. The nature of NOHCs and the relative scarcity of NOHC debt in the Australian market mean that it can be difficult to find straightforward comparable securities when it comes to pricing. The universe of issuances from NOHCs in the domestic market consists of only Macquarie, AMP, Challenger and Suncorp, with varying risk profiles. Nonetheless, the NOHCs have traded roughly in line with “pure-play” operating entity issuers in the last 12 months or so. See Figure 1 and 2. Figure 1. NOHC ASX-Listed Hybrid Historical Average Trading Margin

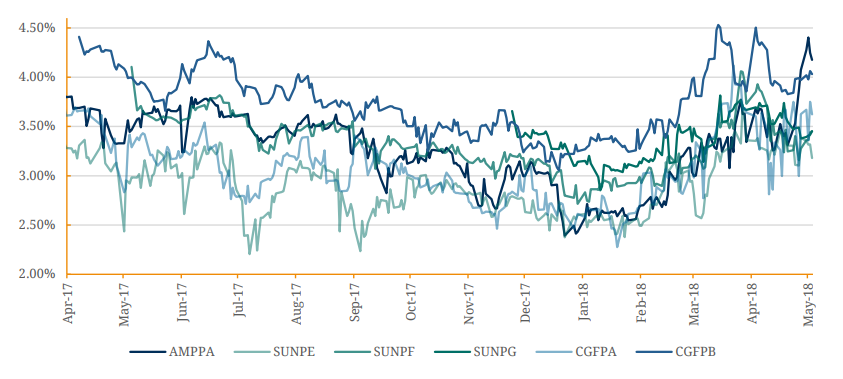

Note: highlighted are names covered by BondAdviser Source: APRA The primary function of NOHCs is to invest in its subsidiaries which are the main operating entities and that carry out the day-to-day business activities of the group that NOHCs themselves do not usually get involved in. NOHCs instead lend initial or ongoing financial support via cash reserves or stock sales and may assist in restructuring the operational model to ensure ongoing viability. NOHCs are normally structured as corporations to protect assets, absorb financial losses and limit liability. Operating companies are owned by NOHCs, and their net profits after expenses are paid to NOHCs as dividends. NOHCs are however allowed to conduct certain, although limited, business activities such as issuing own debt — especially if they are profitable from operating company dividends. From a fixed income investor’s perspective, NOHCs represent a rather unique risk-return profile. Fundamentally, the source of repayment of a bond issued by a NOHC do not come from day-to-day operating income of the main operating entities, but rather indirectly from the dividends paid by operating entities. In a distressed scenario, this also means that NOHC bond investors usually get repaid from the residual profits after creditors of operating entities have been satisfied – a form of structural subordination, which is an extra risk for investors. Secondly, the capital requirements of operating entities and NOHCs are different under APRA rules. The two are required to separately hold adequate capital, and that capital impost contains different terms. For example, in the aforementioned “Macquarie” example, Macquarie Bank Limited (the operating entity) is subject to APRA’s prudential capital adequacy requirements applicable to all ADIs, and capital instruments issued by Macquarie Bank Limited (and other comparable operating entities) usually contain both CET1 capital and non-viability trigger terms. Whereas capital instruments issued by Macquarie Group Limited (the NOHC), contains only the non-viability term, despite the fact that the proceeds of NOHC-issued instruments may be channelled to operating entities to support operations via parent-subsidiary transactions. Investors to Macquarie Group thus face the possibility of effectively lending funds to Macquarie bank yet ranking behind Macquarie bank investors in a non-viability event, albeit having a theoretical immunity from a capital trigger event which would be applicable only to Macquarie bank investors. We note that there are many possible nuances arising from the group structure and in a stress scenario, all securities are likely to suffer price pressure. Lastly, the upstreaming of dividends from operating entities to NOHCs are usually subject to approval by APRA, which may or may not be given if APRA deems the operating entities as being in distress. Mitigating the risks, investors of NOHC debts do benefit from diversity of earnings – a group such as Macquarie has multiple revenue streams from multiple operating entities which may include an ADI, a wealth management arm, a capital-light advisory business and a proprietary trading arm. As a result, investors of NOHCs get exposure to the entire business risks of the group, rather than that of a stand-alone operating entity (usually the bank). In this respect, NOHCs offer an appealing exposure to certain cohorts of investors. The nature of NOHCs and the relative scarcity of NOHC debt in the Australian market mean that it can be difficult to find straightforward comparable securities when it comes to pricing. The universe of issuances from NOHCs in the domestic market consists of only Macquarie, AMP, Challenger and Suncorp, with varying risk profiles. Nonetheless, the NOHCs have traded roughly in line with “pure-play” operating entity issuers in the last 12 months or so. See Figure 1 and 2. Figure 1. NOHC ASX-Listed Hybrid Historical Average Trading Margin  Source: BondAdviser Figure 2. Recent Non-Major Bank Hybrid AT1 Trading Margins

Source: BondAdviser Figure 2. Recent Non-Major Bank Hybrid AT1 Trading Margins  Source: BondAdviser As the market appears to be valuing NOHC debts as proxies for pure-play bank debts, it indicates that the market perceives the NOHC debts’ structural weakness is roughly offset by its income diversification benefits, leaving risks inherent to the main operating entity (the bank in most cases) as the main source of risk and return. Whist this may well be justified in the last 12 months, it remains to be seen whether this valuation rationale will change following Basel III finalisation and the royal commission. As bank regulations tighten further, arguably lessening the structural risk of NOHCs, will the income diversification benefit enjoyed by NOHCs play a more dominant role in overall pricing? The answer should be revealed in the next few years.

Source: BondAdviser As the market appears to be valuing NOHC debts as proxies for pure-play bank debts, it indicates that the market perceives the NOHC debts’ structural weakness is roughly offset by its income diversification benefits, leaving risks inherent to the main operating entity (the bank in most cases) as the main source of risk and return. Whist this may well be justified in the last 12 months, it remains to be seen whether this valuation rationale will change following Basel III finalisation and the royal commission. As bank regulations tighten further, arguably lessening the structural risk of NOHCs, will the income diversification benefit enjoyed by NOHCs play a more dominant role in overall pricing? The answer should be revealed in the next few years.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.