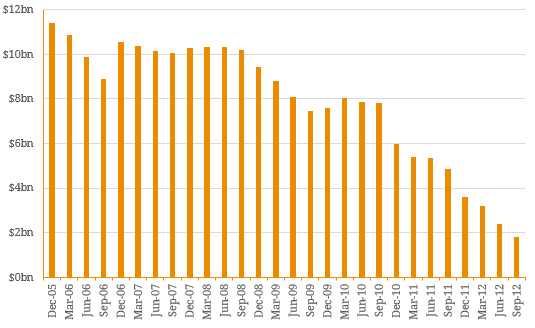

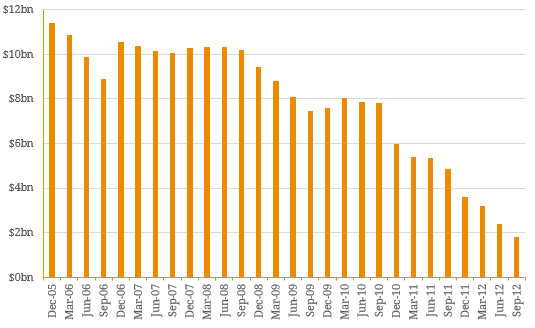

As history has shown, technological advancement is inevitable. Facebook invented the concept of social media advertising, Amazon’s rise of e-commerce power is currently revolutionising the retail industry and share-ride app Uber has permanently altered people’s transport options. History has also shown that companies who fail to adapt to technological transitions generally become obsolete. A stark example of this is the demise of Eastman Kodak, once one of the world’s largest photography and imagery company which failed to adjust to the rise of the digital camera and subsequently, the smartphone. Instead, the complacency of management and its decision to hang onto their once-strong core film business rendered the company defunct. Figure 1. Kodak Trailing 12 Months Revenue  Source: BondAdviser, Company Reports Although Kodak made a strong push into the digital industry in 2001, it was arguably too late. With a market share of 27% in 1999, this slowly deteriorated to 7% by 2010 as Asian technology giants such as Canon, Sony and Nikon flocked to the US market with the ability to severely undercut incumbents. To compete, the company engaged in the pricing environment and hence, operated with negative margins. As a result, Kodak gradually depleted its cash reserves and after a failed attempt to reinvigorate the company as a printing business (another industry which has been structurally challenged), in January 2012, management filed for bankruptcy. To add to Kodak’s woes, the group had a legacy of significant unfunded pension schemes. Figure 2. Kodak USD 7.25% 2013 Bond Price History

Source: BondAdviser, Company Reports Although Kodak made a strong push into the digital industry in 2001, it was arguably too late. With a market share of 27% in 1999, this slowly deteriorated to 7% by 2010 as Asian technology giants such as Canon, Sony and Nikon flocked to the US market with the ability to severely undercut incumbents. To compete, the company engaged in the pricing environment and hence, operated with negative margins. As a result, Kodak gradually depleted its cash reserves and after a failed attempt to reinvigorate the company as a printing business (another industry which has been structurally challenged), in January 2012, management filed for bankruptcy. To add to Kodak’s woes, the group had a legacy of significant unfunded pension schemes. Figure 2. Kodak USD 7.25% 2013 Bond Price History  Source: BondAdviser, Company Reports In terms of credit, the Kodak story is interesting to highlight due to the perceived strength it once had. In 1996, the company was rated AA- by Standard and Poor’s (S&P) but by 2012 the group reached default status (‘D’). To put this credit strength in perspective, the median credit rating of the top 20 companies listed on the ASX is ‘A’ demonstrating the ‘blue chip’ credit quality Kodak once had. Figure 3. Kodak Credit Rating History

Source: BondAdviser, Company Reports In terms of credit, the Kodak story is interesting to highlight due to the perceived strength it once had. In 1996, the company was rated AA- by Standard and Poor’s (S&P) but by 2012 the group reached default status (‘D’). To put this credit strength in perspective, the median credit rating of the top 20 companies listed on the ASX is ‘A’ demonstrating the ‘blue chip’ credit quality Kodak once had. Figure 3. Kodak Credit Rating History  Source: Bloomberg, BondAdviser Although a credit deterioration such as Kodak’s is fairly rare, the company’s fall illustrates the critical importance of management. While the photography industry has structurally shifted over two-decades, the company’s closest competitor, Fujifilm, successfully navigated itself through a period of unprecedented change. This highlights the emphasis of qualitative factors in the credit analysis process such as strategy, culture and management attitudes. Nonetheless, Kodak demonstrates that even the strongest companies can falter and credit investors should ensure they do not allow their analysis to become complacent, or to only focus on the numbers and not the wider story.

Source: Bloomberg, BondAdviser Although a credit deterioration such as Kodak’s is fairly rare, the company’s fall illustrates the critical importance of management. While the photography industry has structurally shifted over two-decades, the company’s closest competitor, Fujifilm, successfully navigated itself through a period of unprecedented change. This highlights the emphasis of qualitative factors in the credit analysis process such as strategy, culture and management attitudes. Nonetheless, Kodak demonstrates that even the strongest companies can falter and credit investors should ensure they do not allow their analysis to become complacent, or to only focus on the numbers and not the wider story.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.