A few weeks ago, ANZ caught investors by surprise by announcing a potential on-market buy-back offer for its $1.3 billion of its Convertible Preference Shares (CPS3, ASX code: ANZPC), issued in September 2011. As per the original terms and conditions, ANZ has a right to redeem (formally “exchange”) the CPS3 on 1 September 2017 but ANZ will not be exercising this right. Click here for the announcement. A new hybrid capital instrument is expected to be announced in conjunction with confirmation of the buy-back (after 15 August 2017 – ANZ’s Third Quarter Update) and we will provide a full research report in due course. If it does so choose, we estimate that ANZ could issue between $1.0 and $1.5 billion in a new capital security at a margin of at least 3.50%. For income investors, this compares favourably to relative liquidity and margin (3.10%) of ANZPC. ANZ outlined three eventual elective options for existing noteholders:

- to reinvest CPS3 into the new hybrid capital instrument;

- for CPS3 to be bought back at their face value for cash; or

- to do nothing, in which case the relevant CPS3 will remain listed on the ASX (until redeemed or converted at a future date in accordance with the CPS3 terms).a

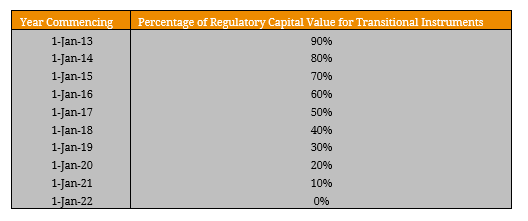

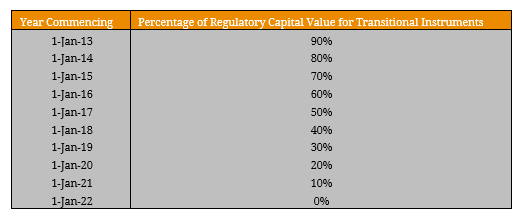

Investors do not have to take any action at this stage, with further details to be provided after ANZ’s third quarter trading update on 15 August 2017. But what are the implications of this unusual action? For us, ANZ’s actions are uncanny and ultimately raises questions around the standard valuation conventions of Additional Tier 1 (AT1) hybrids. In line with market conventions, AT1 hybrid instruments are typically priced assuming redemption on the first optional call date and all interest payments being made in a timely manner (i.e. no interest deferral). However, the outcome of ANZPC conflicts with the former and raises the question whether will other banks repeat? ANZPC was issued with both Basel II and Basel III features and APRA had granted it transitional capital treatment until 1 September 2019, its mandatory conversion date. This transitional treatment progressively amortises the amount of non-Basel III compliant, non-common equity capital instruments which are allowed to be included by an Authorised Depository Institution (ADI) for regulatory capital purposes. Figure 1. Transitional Arrangement for Capital Instruments  Source: APRA Although redemption/replacement is not absolutely necessarily, retaining the ANZPC notes with a further 10% cut to regulatory value (to 40%) in the allowable amount of total non-compliant instruments (1 January 2018) is perhaps manageable in the current regulatory landscape. However, there are ultimately too many factors at play to deliver a concise reason behind the bank’s decision without further detail which may come with ANZ’s Q3 Update. Figure 2. Transitional Regulatory Value of ANZPC

Source: APRA Although redemption/replacement is not absolutely necessarily, retaining the ANZPC notes with a further 10% cut to regulatory value (to 40%) in the allowable amount of total non-compliant instruments (1 January 2018) is perhaps manageable in the current regulatory landscape. However, there are ultimately too many factors at play to deliver a concise reason behind the bank’s decision without further detail which may come with ANZ’s Q3 Update. Figure 2. Transitional Regulatory Value of ANZPC  Source: BondAdviser The Westpac Convertible Preference Shares (ASX Code: WBCPC) are the only other major bank AT1 securities which are eligible for this capital treatment but our base-case assumption remains that all AT1 hybrid securities will be redeemed at the first optional call date. As a result, we consider ANZPC as an outlier and unlikely to become the custom with these types of instruments. It is important to recognise that ANZPC noteholders clearly retain the flexible upper-hand in this situation as outlined by the options above. For this reason, we are comfortable with the situation from a credit perspective despite being highly unanticipated.

Source: BondAdviser The Westpac Convertible Preference Shares (ASX Code: WBCPC) are the only other major bank AT1 securities which are eligible for this capital treatment but our base-case assumption remains that all AT1 hybrid securities will be redeemed at the first optional call date. As a result, we consider ANZPC as an outlier and unlikely to become the custom with these types of instruments. It is important to recognise that ANZPC noteholders clearly retain the flexible upper-hand in this situation as outlined by the options above. For this reason, we are comfortable with the situation from a credit perspective despite being highly unanticipated.