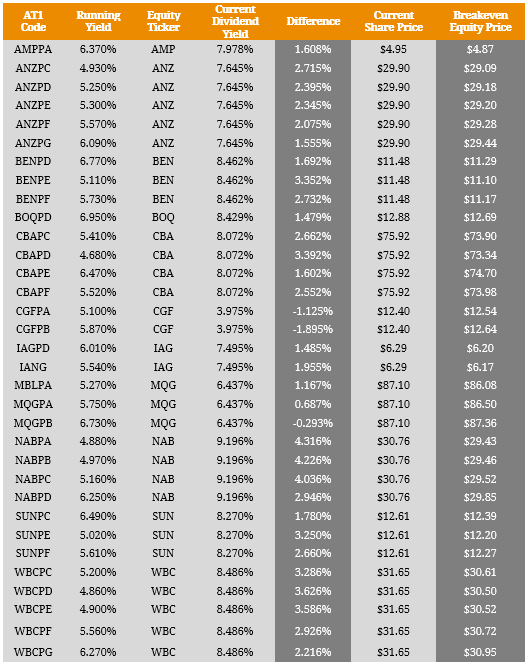

Investors often ask the question, should I buy a company’s equity or its hybrid? Given the full payment discretion and deep subordination for both securities, this argument has its merit but as we pointed out in our article, The Risk in Using Shares for Income, capital volatility for hybrids is relatively tame in normal market conditions. While this is how we expect a fixed income instrument to behave, the inherent equity-like traits of hybrids take over periods of market distress (i.e. capital downside) which highlights the ongoing “are hybrids debt or equity?” argument. Given this risk of capital loss without the mirrored probability of a capital gain (i.e. capital returns for hybrids are skewed), this arguably raises a positive argument for equity which can experience capital upside and typically a higher distribution rate in the form of a dividend yield. However, understanding this difference in risk-reward profiling is a necessary skill for any investor. On a like-for-like basis, the most comparable performance measures between hybrids and equity are the running yield and the dividend yield. These metrics are calculated by dividing the projected income over the coming year by the current price. Using these calculations, we illustrate the ‘Breakeven Equity Price’ which is the share price at which the 1-year yield (running yield) on a hybrid equates to a 1-year yield (dividend yield) on the underlying equity. In other words, the yield differential between a hybrid and the underlying issuer’s equity represents the maximum loss an investor can incur before equity becomes an inferior investment over a 1-Year horizon. However, this assumes that the capital price of the hybrid, and income streams for both instruments remains stable over the course of the year. Given hybrids are generally associated with ‘Buy and Hold’ strategies, it would be more appropriate to conduct this analysis on a yield-to-maturity basis but this would require a number of assumptions on uncertain variables hence rendering a more uncertain conclusion. Table 1. Running Yield v Equity Yield  Source: BondAdviser, Bloomberg On this basis, if we look at yields on an outright basis, equities appear attractive but this can easily be eroded by small percentage moves in the share price. As Figure 1 shows the trailing 1-year maximum drawdown (the percentage change from peak to bottom) for each issuer exceeds the share price breakeven point which highlights the instability of the return profile. While we concede hybrids are not immune to significant capital losses, this would most likely only be in an extreme risk scenario. Figure 1. 1-Year Equity Maximum Drawdowns

Source: BondAdviser, Bloomberg On this basis, if we look at yields on an outright basis, equities appear attractive but this can easily be eroded by small percentage moves in the share price. As Figure 1 shows the trailing 1-year maximum drawdown (the percentage change from peak to bottom) for each issuer exceeds the share price breakeven point which highlights the instability of the return profile. While we concede hybrids are not immune to significant capital losses, this would most likely only be in an extreme risk scenario. Figure 1. 1-Year Equity Maximum Drawdowns  Source: BondAdviser, Bloomberg This notion is further demonstrated in Figure 2 which shows the percentage downside and upside from the ‘breakeven’ point. This illustrates that comparing hybrids and equity on a yield basis is a highly ambiguous task given the inherent capital volatility of equity. This range was calculated off the 52-week high and low of the underlying equity price and by doing so, we have no view on the future performance of underlying equity. Figure 2. Upside and Downside to from 1-Year Breakeven Equity Price

Source: BondAdviser, Bloomberg This notion is further demonstrated in Figure 2 which shows the percentage downside and upside from the ‘breakeven’ point. This illustrates that comparing hybrids and equity on a yield basis is a highly ambiguous task given the inherent capital volatility of equity. This range was calculated off the 52-week high and low of the underlying equity price and by doing so, we have no view on the future performance of underlying equity. Figure 2. Upside and Downside to from 1-Year Breakeven Equity Price  Source: BondAdviser, Bloomberg Overall, this simple analysis shows the complexities in selecting a hybrid or the underlying equity. While both exhibit similarities, they are still worlds apart and should be treated as such. Although high-dividend paying stocks are treated as an income proxy in many portfolios, they are inevitably a growth asset with the majority of performance driven by capital returns. We advocate that successful asset allocation must be backed by a solid investment framework and understanding the risk-reward profile across an issuer’s capital structure. This allows investors to preserve capital against while generating an adequate return.

Source: BondAdviser, Bloomberg Overall, this simple analysis shows the complexities in selecting a hybrid or the underlying equity. While both exhibit similarities, they are still worlds apart and should be treated as such. Although high-dividend paying stocks are treated as an income proxy in many portfolios, they are inevitably a growth asset with the majority of performance driven by capital returns. We advocate that successful asset allocation must be backed by a solid investment framework and understanding the risk-reward profile across an issuer’s capital structure. This allows investors to preserve capital against while generating an adequate return.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.