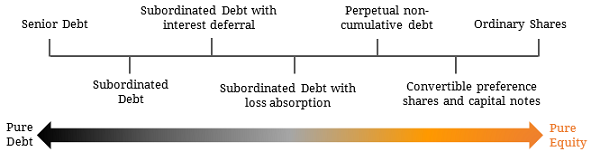

As discussed in a recent nabtrade interview with BondAdviser Director Nick Yaxley, the combination of equity market volatility and a low-yielding credit environment has caused investors to re-examine opportunities with the domestic ASX-listed hybrid market. Hybrids are a broad classification of securities issued by corporations that structurally contain both debt and equity characteristics, sitting below subordinated debt and above equity in the capital structure with a tendency to offer higher yields than senior bonds. When used correctly, hybrids can provide an efficient diversification across a broader portfolio depending on the security’s structure, inherent risk and underlying issuer. Figure 1. Hybrid Security Spectrum  Source: ASIC, BondAdviser The relative attractiveness of hybrid securities is two-fold, with both risk and return factors determining if an opportunity exists or not. In terms of return, the base rate for these instruments, being the Bank Bill Swap Rate (BBSW), has been trending steadily upwards throughout mid-February and March as shown in Figure 2 below. On the other hand, trading margins have widened over the period and AT1 hybrid valuations have returned to arguably a more reasonable level. Figure 2. The 90-Day BBSW steadily increased while capital value of AT1 hybrids declined in Q118

Source: ASIC, BondAdviser The relative attractiveness of hybrid securities is two-fold, with both risk and return factors determining if an opportunity exists or not. In terms of return, the base rate for these instruments, being the Bank Bill Swap Rate (BBSW), has been trending steadily upwards throughout mid-February and March as shown in Figure 2 below. On the other hand, trading margins have widened over the period and AT1 hybrid valuations have returned to arguably a more reasonable level. Figure 2. The 90-Day BBSW steadily increased while capital value of AT1 hybrids declined in Q118  Source: BondAdviser, Bloomberg The combination of BBSW increases and a widening in trading margins has pushed major bank hybrid yields up to the 5.5-6.5% mark seen in Figure 3 below. Given the largely benign economic environment seen in Australia with the RBA continuing to keep rates at historically-low levels, cheaper valuations could prove to be an opportune time for yield-chasing investors to add these securities to their portfolio. Figure 3. ASX-Listed Major Bank Additional Tier 1 Hybrids: Current Yields on Instruments with a call date between 1-5 years

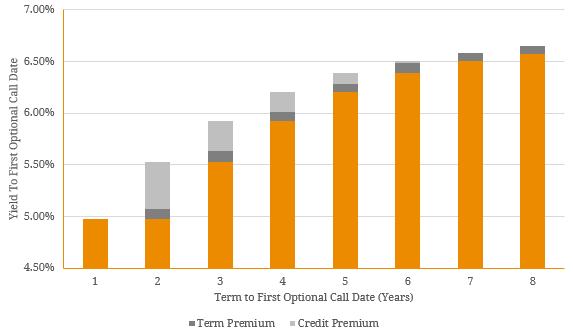

Source: BondAdviser, Bloomberg The combination of BBSW increases and a widening in trading margins has pushed major bank hybrid yields up to the 5.5-6.5% mark seen in Figure 3 below. Given the largely benign economic environment seen in Australia with the RBA continuing to keep rates at historically-low levels, cheaper valuations could prove to be an opportune time for yield-chasing investors to add these securities to their portfolio. Figure 3. ASX-Listed Major Bank Additional Tier 1 Hybrids: Current Yields on Instruments with a call date between 1-5 years  Source: BondAdviser, 3rd of April 2018 Hybrid pricing is a function of risk, and being a more complex class of securities, require more unique evaluation than some of the more vanilla investment options available to investors. The risks involved in hybrids are many and varied, and sometimes security specific. Factors including redemption date, non-viability triggers, individual security structure, call options and convertibility into shares all represent additional risks to an investor. Despite its inherent complexity, historical figures show the hybrids sector to have a long-tail risk, meaning the probability of loss is generally low across all securities the majority of the time. Importantly, the variable nature of hybrid securities means investors should think in terms of units of risk per year. This allows investors to compare hybrid security returns to that of more traditional instruments such as bonds, as well as compare structurally different securities to each other. For instance, why would one invest in a 4-year hybrid security with the same return per unit of risk as a 1-year security, given the term risk of holding a security for longer? Figure 4 below separates the yield to first optional call in terms of marginal return per unit of risk, demonstrating that investors in longer-term hybrids receive almost no extra credit risk compensation despite being priced-in for shorter-term securities. Figure 4. Major Bank Hybrids: Additional Return per Unit of Term Risk

Source: BondAdviser, 3rd of April 2018 Hybrid pricing is a function of risk, and being a more complex class of securities, require more unique evaluation than some of the more vanilla investment options available to investors. The risks involved in hybrids are many and varied, and sometimes security specific. Factors including redemption date, non-viability triggers, individual security structure, call options and convertibility into shares all represent additional risks to an investor. Despite its inherent complexity, historical figures show the hybrids sector to have a long-tail risk, meaning the probability of loss is generally low across all securities the majority of the time. Importantly, the variable nature of hybrid securities means investors should think in terms of units of risk per year. This allows investors to compare hybrid security returns to that of more traditional instruments such as bonds, as well as compare structurally different securities to each other. For instance, why would one invest in a 4-year hybrid security with the same return per unit of risk as a 1-year security, given the term risk of holding a security for longer? Figure 4 below separates the yield to first optional call in terms of marginal return per unit of risk, demonstrating that investors in longer-term hybrids receive almost no extra credit risk compensation despite being priced-in for shorter-term securities. Figure 4. Major Bank Hybrids: Additional Return per Unit of Term Risk  Source: BondAdviser, 3rd of April 2018 Whilst there is an undeniable link to equity markets, our view remains that fundamentally the risk involved in the hybrid market remains, to a large extent, unchanged. Recent volatility has altered prices and changed valuation of hybrid securities, but overall the broader economic and regulatory environment including the Banking Royal Commission will, in our view, prove to be a positive in tightening and improving lending restrictions as well shoring up equity capital in the future (a first defence to hybrid investors). In a benign credit environment, combined with a recent increase in yields, it is our view that the right instruments can effectively complement a fixed income portfolio to provide high-yield, diversified alternatives. To view the nabtrade interview with Nick Yaxley, please click here.

Source: BondAdviser, 3rd of April 2018 Whilst there is an undeniable link to equity markets, our view remains that fundamentally the risk involved in the hybrid market remains, to a large extent, unchanged. Recent volatility has altered prices and changed valuation of hybrid securities, but overall the broader economic and regulatory environment including the Banking Royal Commission will, in our view, prove to be a positive in tightening and improving lending restrictions as well shoring up equity capital in the future (a first defence to hybrid investors). In a benign credit environment, combined with a recent increase in yields, it is our view that the right instruments can effectively complement a fixed income portfolio to provide high-yield, diversified alternatives. To view the nabtrade interview with Nick Yaxley, please click here.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.