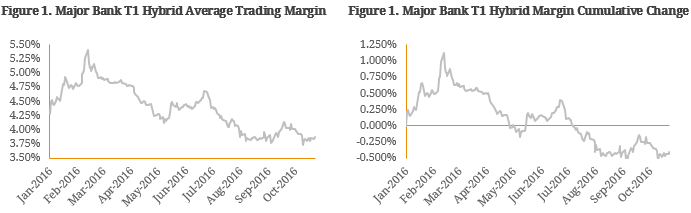

Back in February 2016, trading margins of ASX-listed hybrid securities widened significantly. As a result, there were a number of attractive investment opportunities and following a relatively stable reporting season and shift in sentiment, margins began to retrace. While on the surface it appears margins are still tracking well relative to February, a more suitable performance measure would be to calculate the cumulative change to see if investors have recovered the losses endured at start of the year. To demonstrate this analysis, we utilise the largest sub-set of the ASX-listed hybrid market, Major Bank Tier 1 Hybrids. Figure 1. Major Bank T1 Hybrid Average Trading Margin  Source: BondAdviser Figure 2. Major Bank T1 Hybrid Average Trading Margin Cumulative Change

Source: BondAdviser Figure 2. Major Bank T1 Hybrid Average Trading Margin Cumulative Change  Source: BondAdviser As we can see, the cumulative data gives us a much clearer picture regarding security performance year-to-date. For example, Major Bank Tier 1 hybrids have recovered strongly since anything pooled as bank equity (including hybrids) sold-off prior to mid-February and investors are up ~0.40% for the year on a cumulative basis. We note that this sell-off correlation is an anomaly which is unique to Australia and has little to do with the associated hybrid security risk. How has this fared against other hybrid classes? If we compare performance against 2nd Tier Bank issuers, we can see Major Bank Tier hybrids have underperformed other Tier 1 hybrids by ~0.45% year-to-date. We expect this has been a function of supply-side factors as three new Major Bank Tier 1 Hybrids have been upsized in 2016 while 2nd Tier bank issuance has been limited. In defining 2nd Tier Banks with include AMP, Suncorp, Macquarie, Bendigo & Adelaide Bank and Bank of Queensland. Figure 3. Major Bank Vs 2nd Tier Bank T1 Hybrid Average Trading Margin Cumulative Change

Source: BondAdviser As we can see, the cumulative data gives us a much clearer picture regarding security performance year-to-date. For example, Major Bank Tier 1 hybrids have recovered strongly since anything pooled as bank equity (including hybrids) sold-off prior to mid-February and investors are up ~0.40% for the year on a cumulative basis. We note that this sell-off correlation is an anomaly which is unique to Australia and has little to do with the associated hybrid security risk. How has this fared against other hybrid classes? If we compare performance against 2nd Tier Bank issuers, we can see Major Bank Tier hybrids have underperformed other Tier 1 hybrids by ~0.45% year-to-date. We expect this has been a function of supply-side factors as three new Major Bank Tier 1 Hybrids have been upsized in 2016 while 2nd Tier bank issuance has been limited. In defining 2nd Tier Banks with include AMP, Suncorp, Macquarie, Bendigo & Adelaide Bank and Bank of Queensland. Figure 3. Major Bank Vs 2nd Tier Bank T1 Hybrid Average Trading Margin Cumulative Change  Source: BondAdviser To further extend our analysis, we can compare financial and corporate security performance. Due to minimal government support and more volatile earnings and cashflow, the February breakout was much more significant for non-financial corporate issuers. Energy companies such as AGL, Origin and APA Group were all hit hard by the sharp fall in the oil price, there were fears that Seven Group would slash dividends on its hybrid and there was growing uncertainty around Crown’s motives regarding timely redemption. As commodity prices began to stabilise and more internal information came to light, corporate hybrids began to recover but have underperformed their financial counterparts by ~0.30%. Overall, corporate hybrids are almost flat since the start of the year. However, this is primarily due to the greater degree of volatility inherent in corporate hybrid trading margins. Figure 4. Financial Vs Corporate Hybrid Average Trading Margin Cumulative Change

Source: BondAdviser To further extend our analysis, we can compare financial and corporate security performance. Due to minimal government support and more volatile earnings and cashflow, the February breakout was much more significant for non-financial corporate issuers. Energy companies such as AGL, Origin and APA Group were all hit hard by the sharp fall in the oil price, there were fears that Seven Group would slash dividends on its hybrid and there was growing uncertainty around Crown’s motives regarding timely redemption. As commodity prices began to stabilise and more internal information came to light, corporate hybrids began to recover but have underperformed their financial counterparts by ~0.30%. Overall, corporate hybrids are almost flat since the start of the year. However, this is primarily due to the greater degree of volatility inherent in corporate hybrid trading margins. Figure 4. Financial Vs Corporate Hybrid Average Trading Margin Cumulative Change  Source: BondAdviser Since March, hybrid performance has been well supported by the ongoing search for yield. With two cuts to the cash rate this year, investors have invested further down the capital structure into hybrids and we expect this to continue. However, we reiterate the risk inherent in these types of security is asymmetric. In other words, these types of securities will be correlated to ordinary equity when markets are volatile but behave more like traditional fixed income instruments when conditions stabilise, eliminating the upside achieved in equities. For this reason, investors are not fully compensated for the risk of equity-like breakouts (as seen in February) and it could be months (even years) before investors recover the capital losses.

Source: BondAdviser Since March, hybrid performance has been well supported by the ongoing search for yield. With two cuts to the cash rate this year, investors have invested further down the capital structure into hybrids and we expect this to continue. However, we reiterate the risk inherent in these types of security is asymmetric. In other words, these types of securities will be correlated to ordinary equity when markets are volatile but behave more like traditional fixed income instruments when conditions stabilise, eliminating the upside achieved in equities. For this reason, investors are not fully compensated for the risk of equity-like breakouts (as seen in February) and it could be months (even years) before investors recover the capital losses.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.