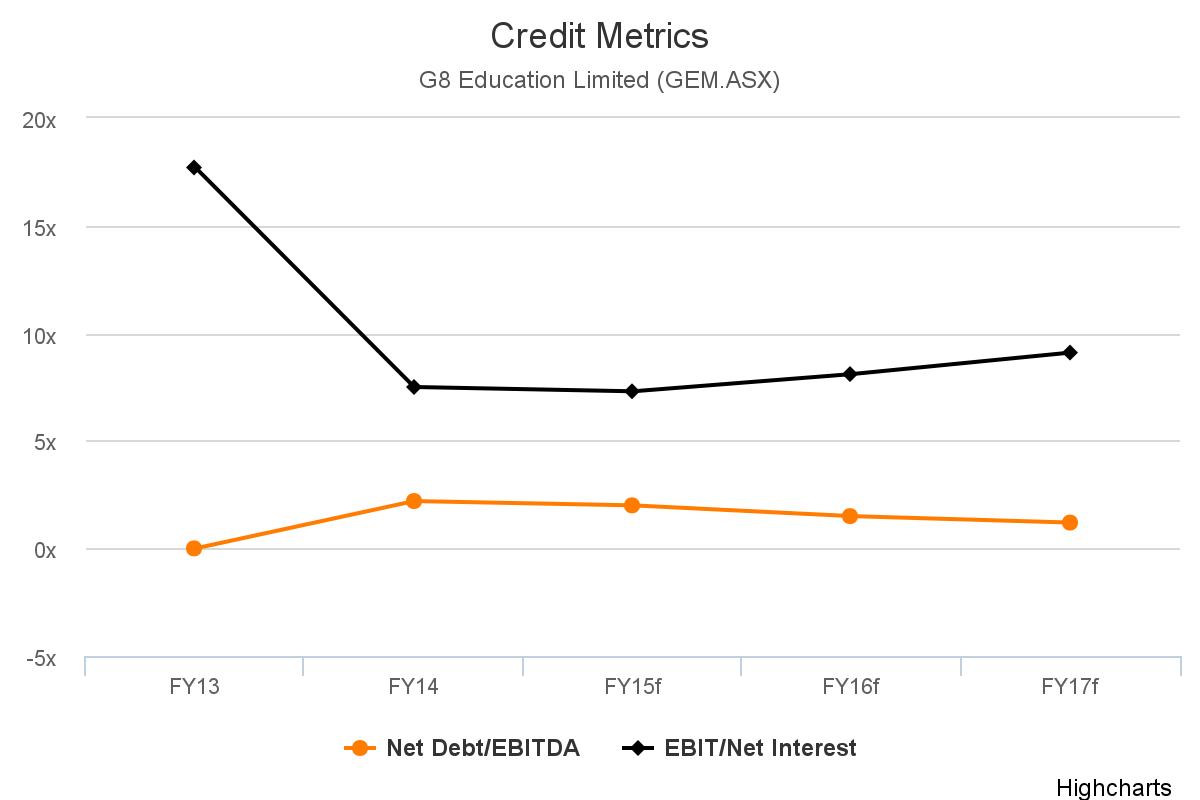

G8 Education Limited has announced the early redemption of $155m of Singapore Dollar Notes. These notes will be redeemed on 29 February 2016. The purpose of issuing these notes was predominantly for the acquisition for Affinity Education which subsequently did not proceed. In our last update we reiterated that downside risks to investors comes from increased debt to fuel an aggressive acquisition program (this was clearly illustrated by the attempted take-over of Affinity Education Group). This was going hand in hand with a trend of G8 paying greater than 4.0x multiples for established child care centers and major acquisitions (i.e AFJ’s) being at 7x 2015 estimated EBITDA. This would effectively means the credit metrics of G8 will deteriorate as is grows. However, this doesn’t change our opinion on the the earnings profile of G8 as evidenced by favourable government funding, an undersupply of centers and decent key performance indicators. We believe that investors are not rewarded for what we anticipate to be a debt-funded acquisition profile over the near term and a deterioration in credit metrics. Ultimately G8 still has the capacity to tap additional debt under its debt program and will continue to do so in 2016. But on current metrics (Net Leverage to decline to 0.78x from 2.5x (based on Bloomerg FY15 estimate of ~$160m EBITDA and gearing to decrease from 40% to 27%.) the credit profile of the group is arguably strong and we expect the group’s full year results (22nd February 2016) to reiterate this thesis.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.