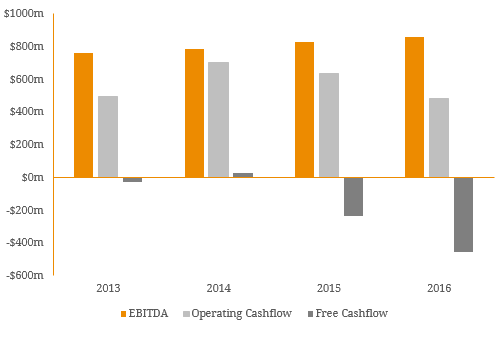

In the world of credit analysis, investors are often misled by EBITDA as it is sometimes used as a proxy for cashflow. EBITDA refers to a company’s earnings before interest expense, taxation, depreciation and amortisation of certain capital expenses. While it is commonly used as a benchmark between peers, the measure does not account for capital expenditures, fails to accurately capture a firm’s liquidity and is subject to varying accounting decisions. On the other hand, free cashflow represents the actual surplus cash a company has to meet short term liquidity requirements. This measure incorporates changes in working capital and capital expenditures and is much harder to adjust with different accounting standards. Changes in working capital include adjustments to balance sheet items such as accounts receivables, payables, inventories, prepaid expenses and deferred revenue. These adjustments are typically calculated on varying accounting standards and assumptions and recognised in the income statement. This filters through to EBITDA. However, as they are non-cash movements they are removed from cashflow metrics to accurately pinpoint movements in cash over the reporting period. This can result in major discrepancies between a company’s earnings versus its actual cashflow. By way of example, Figure 1 illustrates this concept for an ASX200 Corporate issuer. As depicted, EBITDA has slowly risen year on year but cashflow has deteriorated. Figure 1. Example of Corporate EBITDA v Cashflow  Source: BondAdviser, Company Reports As the old saying goes, revenue is vanity, profit is sanity but cash is reality. This is one of the major pillars of credit analysis and reflects the importance of the cashflow statement when analysing a debt issuer’s financials. If earnings are not aligned with operating cashflows, this is generally a red light and should signal to an investor to take a deeper look.

Source: BondAdviser, Company Reports As the old saying goes, revenue is vanity, profit is sanity but cash is reality. This is one of the major pillars of credit analysis and reflects the importance of the cashflow statement when analysing a debt issuer’s financials. If earnings are not aligned with operating cashflows, this is generally a red light and should signal to an investor to take a deeper look.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.