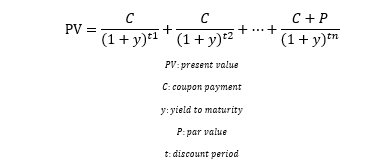

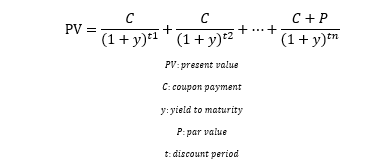

In Australia’s low-yield environment, higher-risk income securities (i.e. hybrids) tend to be more favoured for their attractive returns. However, the yield of a hybrid varies based on many factors. Perhaps most important are the assumptions of when the security will be redeemed or converted. Conventionally, hybrid securities are either called on their first call date (or each interest payment thereafter) or exchanged for common equity on the mandatory conversion date (a later date). The basic formula for these two methods is shown below:  BondAdviser’s core valuation assumptions for hybrids are based on the securities being redeemed (in full) on the optional exchange date and all interest payments being made (in full) in a timely manner. The reason for this assumption is that the price could drop significantly if the redemption does not happen on the first call date due to extension. For example, the price of ANZPF (a hybrid security issued by ANZ) was $102.89 on 21 August 2017, delivering a yield to maturity (YTM) of 5.911% based on the expected redemption of 24 March 2023 (the first optional call date). However, the price should decrease to $102.35 if not redeemed and mandatory conversion could occur (on 24 March 2025), assuming that the issuer’s credit metrics remain unchanged (the trading margin remains constant). The possible extension risks associated with holding ANZPF for the period to the first call date is reflected in the $0.54 price difference. When some companies deem repayment less cost-effective, the securities are sometimes neither redeemed nor converted and left outstanding. These would then exist in perpetuity, providing regular income streams for security holders with uncertain repayment of the capital (par value). The valuation for these perpetuity-like hybrids follows the perpetuity pricing approach shown below:

BondAdviser’s core valuation assumptions for hybrids are based on the securities being redeemed (in full) on the optional exchange date and all interest payments being made (in full) in a timely manner. The reason for this assumption is that the price could drop significantly if the redemption does not happen on the first call date due to extension. For example, the price of ANZPF (a hybrid security issued by ANZ) was $102.89 on 21 August 2017, delivering a yield to maturity (YTM) of 5.911% based on the expected redemption of 24 March 2023 (the first optional call date). However, the price should decrease to $102.35 if not redeemed and mandatory conversion could occur (on 24 March 2025), assuming that the issuer’s credit metrics remain unchanged (the trading margin remains constant). The possible extension risks associated with holding ANZPF for the period to the first call date is reflected in the $0.54 price difference. When some companies deem repayment less cost-effective, the securities are sometimes neither redeemed nor converted and left outstanding. These would then exist in perpetuity, providing regular income streams for security holders with uncertain repayment of the capital (par value). The valuation for these perpetuity-like hybrids follows the perpetuity pricing approach shown below:  Following on the ANZPF case, on the assumption that ANZPF remains outstanding in perpetuity, the price on 21 August 2017 would be $65.13. The decrease of $37.76 represents the uncertainty arising from the infinite investment horizon and impact of principal non-repayment. This is based on the going concern of the issuer (ANZ) while in reality, the price could drift further downwards for perceived credit risks over such a long horizon. In conclusion, hybrid pricing is based on many factors but a key driver are the differing valuations provide alternate maturity and conversion dates and also whether an instrument becomes perpetual.

Following on the ANZPF case, on the assumption that ANZPF remains outstanding in perpetuity, the price on 21 August 2017 would be $65.13. The decrease of $37.76 represents the uncertainty arising from the infinite investment horizon and impact of principal non-repayment. This is based on the going concern of the issuer (ANZ) while in reality, the price could drift further downwards for perceived credit risks over such a long horizon. In conclusion, hybrid pricing is based on many factors but a key driver are the differing valuations provide alternate maturity and conversion dates and also whether an instrument becomes perpetual.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.