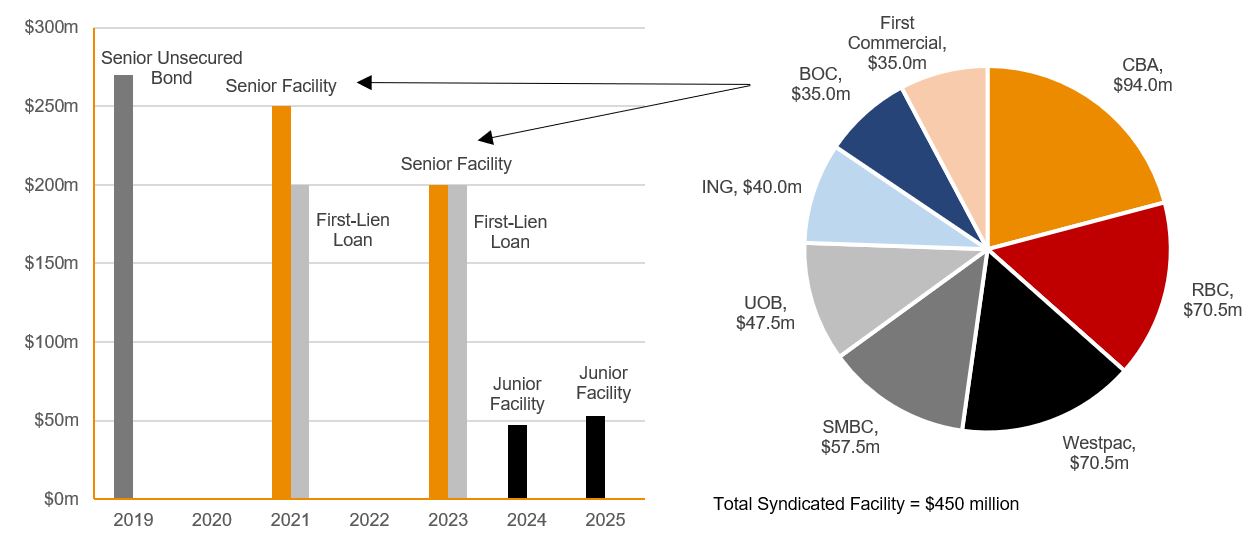

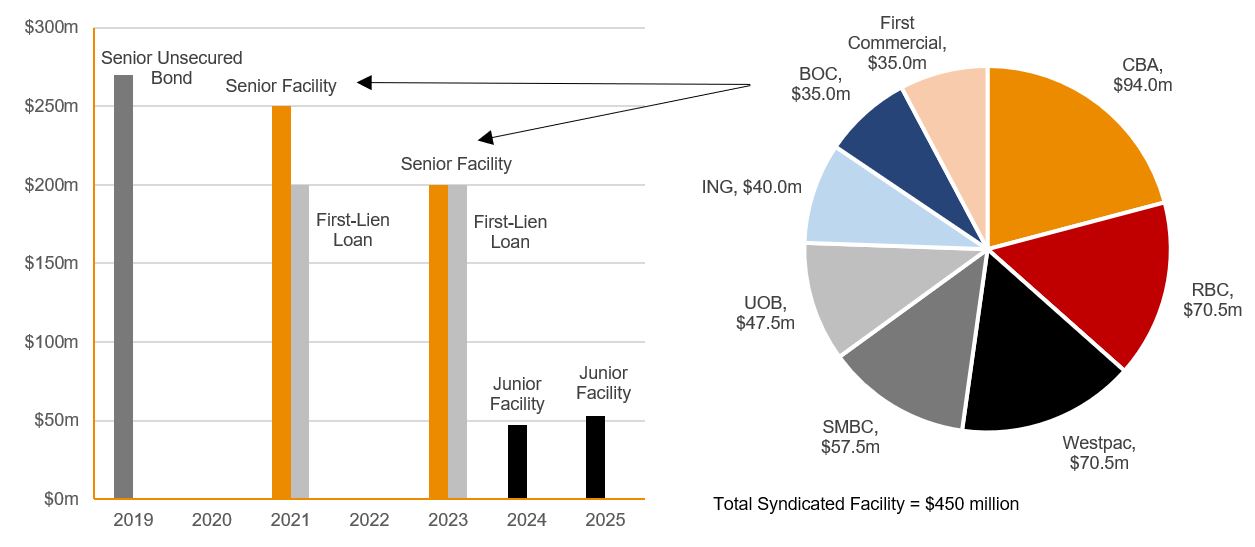

The decision by G8 Education (ASX: GEM) to redeem and refinance its $50 million senior unsecured bonds in March 2018 was reasonably standard practice as far as corporate bond markets are concerned given a company in reasonable financial health. However, the $450 million syndicated bank facility announced in October was an interesting development in the long-running trend of Australian companies shunning the domestic corporate bond markets in favour of alternative financing via offshore issuance or bank lending facilities. The new senior facility, comprising loans from a syndicate of eight banks, and $100 million junior facility from CBA has been entered into for the purpose of increasing capacity, refinancing GEM’s SGD$270 (A$276) million May 2018 Singapore Notes and to extend and improve its maturity profile. However, it is hard to escape the fact that G8 Education’s decision to seek out these facilities rather than seek financing via the local bond markets may be an indication that, in the current environment, the Australian corporate bond market is experiencing a period of significant decline. Whilst this is obviously bad news for local supply in this format, we are also seeing the rise of another fixed income asset class: the Australian private debt market. Figure 1. G8 Education Pro-Forma Debt Maturity Profile  Source: BondAdviser, Bloomberg Australian billionaire Anthony Pratt has been a staunch advocate of supporting the development of the Australian private debt market, and more specifically, the corporate loan market. Pratt, whose Visy brand signed a landmark 10-year, $150 million corporate lending deal with AustralianSuper and IFM Investors in March 2017, has been repeatedly vocal in his desire for establishing a liquid secondary market for Australian corporate loans. The Australian corporate loan market is relatively underdeveloped in comparison to peers in the US and Europe (figure 2), and one of the key factors has been due to the lack of a secondary liquid market. Corporate loans as an asset class are an attractive proposition for private debt investors, offering significant risk-adjusted returns compared to traditional fixed income instruments. However, the current illiquidity of loans (beyond primary origination by the banks) has, to this point, prevented significant growth and capital inflows to the sector. This is because investors, such as the Australian super funds, with an estimated ~$1.7 trillion in funds under management (FUM), require an allocation to liquid investments primarily to manage possible funding commitments from members drawing on their funds at short notice. At present, corporate loans are viewed as an illiquid asset allocation, akin to the much higher-yielding (but riskier) asset classes such as commercial real estate and other alternative investments, thus making them an unattractive proposition for investors with the largest capacity. Figure 2. Global Corporate Loan Volumes by Country

Source: BondAdviser, Bloomberg Australian billionaire Anthony Pratt has been a staunch advocate of supporting the development of the Australian private debt market, and more specifically, the corporate loan market. Pratt, whose Visy brand signed a landmark 10-year, $150 million corporate lending deal with AustralianSuper and IFM Investors in March 2017, has been repeatedly vocal in his desire for establishing a liquid secondary market for Australian corporate loans. The Australian corporate loan market is relatively underdeveloped in comparison to peers in the US and Europe (figure 2), and one of the key factors has been due to the lack of a secondary liquid market. Corporate loans as an asset class are an attractive proposition for private debt investors, offering significant risk-adjusted returns compared to traditional fixed income instruments. However, the current illiquidity of loans (beyond primary origination by the banks) has, to this point, prevented significant growth and capital inflows to the sector. This is because investors, such as the Australian super funds, with an estimated ~$1.7 trillion in funds under management (FUM), require an allocation to liquid investments primarily to manage possible funding commitments from members drawing on their funds at short notice. At present, corporate loans are viewed as an illiquid asset allocation, akin to the much higher-yielding (but riskier) asset classes such as commercial real estate and other alternative investments, thus making them an unattractive proposition for investors with the largest capacity. Figure 2. Global Corporate Loan Volumes by Country  Source: BondAdviser Estimates, BIS, Bloomberg (September 2017) With Australian super funds forecast to hold collective FUM of circa $9 trillion by 2035 (figure 3), perhaps Anthony Pratt is correct in saying that a secondary liquid market is the key to unlocking the full capital potential of the Australian corporate loan market. Additionally, one of the keys to growth and development is investor education, both for retail clients as well as institutional, to fully understand the potential benefits and risks of investing in “non-traditional” asset classes. At BondAdviser, we will shortly be releasing a comprehensive primer for potential loan investors. Figure 3. Australian Superannuation Funds’ Forecast Funds Under Management

Source: BondAdviser Estimates, BIS, Bloomberg (September 2017) With Australian super funds forecast to hold collective FUM of circa $9 trillion by 2035 (figure 3), perhaps Anthony Pratt is correct in saying that a secondary liquid market is the key to unlocking the full capital potential of the Australian corporate loan market. Additionally, one of the keys to growth and development is investor education, both for retail clients as well as institutional, to fully understand the potential benefits and risks of investing in “non-traditional” asset classes. At BondAdviser, we will shortly be releasing a comprehensive primer for potential loan investors. Figure 3. Australian Superannuation Funds’ Forecast Funds Under Management  Source: BondAdviser, Deloitte, ABS The G8 Education syndicated loan facility could well foreshadow what is to come in the changing landscape of Australian corporate debt funding. Ultimately, whilst domestic corporate bonds remain an attractive proposition for portfolio allocation amongst many investors, this latest development should show that the Australian private debt train is quietly gathering pace as it transitions to the mainstream, investible universe.

Source: BondAdviser, Deloitte, ABS The G8 Education syndicated loan facility could well foreshadow what is to come in the changing landscape of Australian corporate debt funding. Ultimately, whilst domestic corporate bonds remain an attractive proposition for portfolio allocation amongst many investors, this latest development should show that the Australian private debt train is quietly gathering pace as it transitions to the mainstream, investible universe.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.