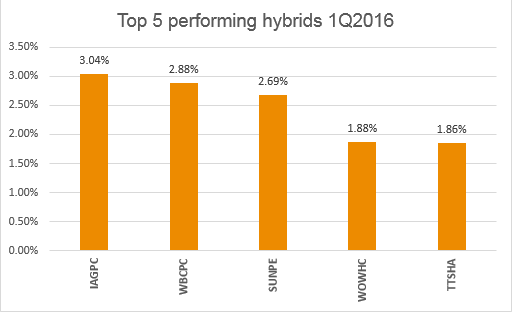

The first quarter of 2016 was a tale of two halves for the ASX listed hybrid universe. January started poorly as the Australian share market followed their global peers as a risk-off tone permeated the financial markets. ASX listed hybrids followed suit with corporate issued hybrids faring much worse than their bank issued peers. The risk-off tone continued into February and it was into this environment that the CBA announced the PERLS VIII (ASX code: CBAPE) issue to replace the PERLS III (ASX code: PCAPA) that have been called as expected. The book-build for the CBAPE hybrid was announced on the 15th February and was the catalyst for investors to reassess the hybrid market. The initial margin for the CBAPE issue was set at the 90-day bank bill swap (90BBSW) rate plus a margin of 5.20%, touted as the biggest margin ever offered for these types of securities. Investors agreed and saw value in the secondary hybrid market causing a sustained rally in both short and mid dated hybrids for the remainder of the quarter. The main beneficiaries of this were the IAG Convertible Preference Shares (ASX: IAGPC), Westpac Convertible Preference Shares (ASX: WBCPC) and Suncorp Convertible Preference Shares III (ASX: SUNPE). On the corporate front, Tatts Bonds (ASX: TTSHA) and Woolworths Subordinated Notes (ASX: WOWHC) were the major standouts for the first quarter. Tatts continues to have a strong balance sheet while Woolworth’s decision to cut its homewares division (Masters) was a major turning point in the credit profile of the group. Chart 1: Top 5 performing hybrids during the first quarter of 2016.  Source: BondAdviser Despite the renewed interest in hybrids over the second half of the quarter, there were some notable exceptions as not all securities recovered. Both the NAB Income Securities (ASX code NABHA) and Macquarie Income Securities (ASX code MBLHB) fared poorly during the quarter as investor sentiment towards securities with a perpetual maturity date waned. The Seven Group TELYS4 (ASX code SVWPA) and the Crown Subordinated Notes II (ASX code CWNHB) were the worst two performing hybrids for the quarter and sold for differing reasons, primarily relating to issues with their underlying issuers. For Crown Resorts, the poor performance can be attributable to ongoing speculation regarding the possibility of privatisation as well insufficient funding for the scale and ambition of their current projects. On the other hand, the Seven Group TELYS4 has been subject to risk of dividend cuts in order for the group to increase capital. Seven’s business segments have performed poorly and the group’s current share buy-back scheme is increasing common equity leverage for the company. All of these factors have contributed to the sell-off in the TELYS4. Chart 2: Bottom 5 performing hybrids during the first quarter of 2016.

Source: BondAdviser Despite the renewed interest in hybrids over the second half of the quarter, there were some notable exceptions as not all securities recovered. Both the NAB Income Securities (ASX code NABHA) and Macquarie Income Securities (ASX code MBLHB) fared poorly during the quarter as investor sentiment towards securities with a perpetual maturity date waned. The Seven Group TELYS4 (ASX code SVWPA) and the Crown Subordinated Notes II (ASX code CWNHB) were the worst two performing hybrids for the quarter and sold for differing reasons, primarily relating to issues with their underlying issuers. For Crown Resorts, the poor performance can be attributable to ongoing speculation regarding the possibility of privatisation as well insufficient funding for the scale and ambition of their current projects. On the other hand, the Seven Group TELYS4 has been subject to risk of dividend cuts in order for the group to increase capital. Seven’s business segments have performed poorly and the group’s current share buy-back scheme is increasing common equity leverage for the company. All of these factors have contributed to the sell-off in the TELYS4. Chart 2: Bottom 5 performing hybrids during the first quarter of 2016.  Source: BondAdviser

Source: BondAdviser

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.