With the September bank reporting season now complete, several common themes have emerged across the sector that we expect to continue to play out over the next twelve months.

Earnings increase but margins remain under pressure and growth targets lowered.

Although cash earnings for Australian banks remained robust during 2016 revenue growth is becoming difficult, suggesting the earnings cycle may have peaked. As a result, previous earnings and profit growth assumptions have been challenged and in some instances lowered.

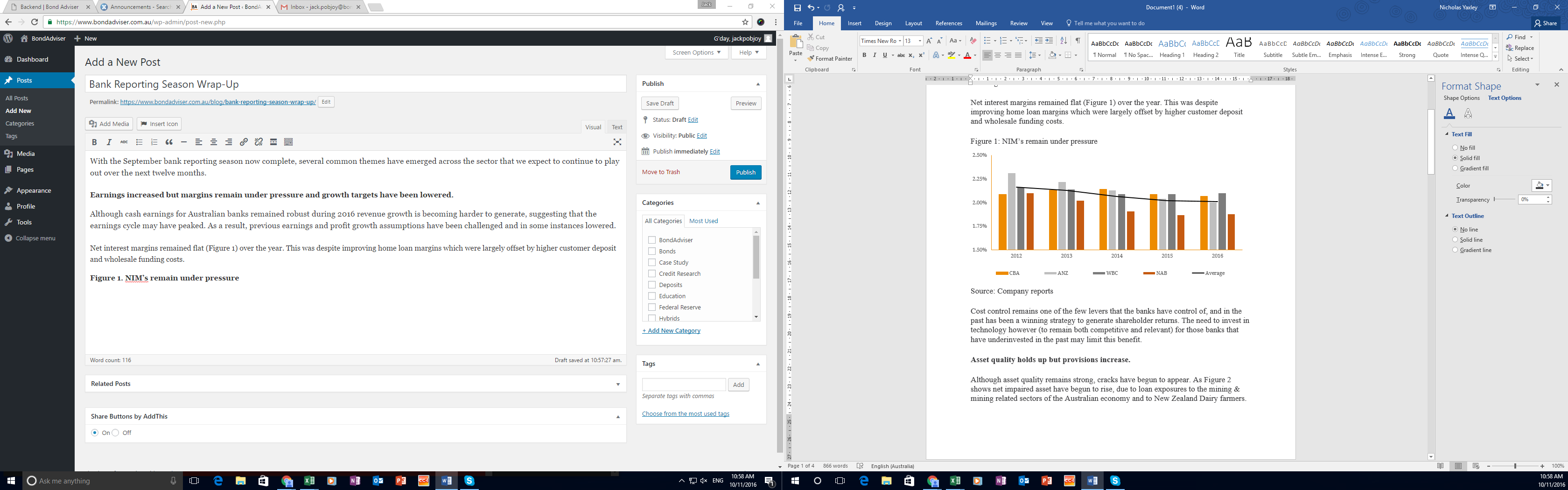

Net interest margins (NIM) remained flat (Figure 1) over the year. Improving home loan margins were largely offset by higher customer deposit and wholesale funding costs.

Figure 1. NIM’s remain under pressure

Source: Company Reports

Cost control remains one of the few levers the banks have left. In the past this has been a winning strategy to generate shareholder returns. Operating expenditure cuts is at odds however for those banks needing to invest in technology.

Although asset quality remains strong, cracks have begun to appear. Figure 2 shows net impaired assets have begun to rise, due to loan exposures to Australian mining related sectors and to New Zealand Dairy farmers.

Figure 2. Impairments starting to rise

Source: Company Reports

High levels of Australian household debt also remain a concern, with the credit rating agencies warning that if house price growth does not moderate there is a 1 in 3 chance of the banking sector being downgraded over the next year. The true test will come if Australian long term interest rates grind higher (following the trend of higher long term global interest rates) and/or Australian unemployment rises, in turn diminishing the ability of households to meet loan repayments.

Common Equity Tier 1 (CET1) capital ratios are flat and now reflected the new Australian mortgage risk weights. The banking sector awaits Basel Committee deliberations. The banks (Figure 3) moved early to raise additional capital required due to APRA increasing the risk weighting for Australian residential mortgages. Figure 3. Average major bank CET1 capital ratios over last 5 years  Source: Company Reports

Source: Company Reports

On an international comparable basis, our major banks reported improved CET1 capital ratios, remaining well positioned to meet the Australian Financial Sector Inquiry recommendation that they remain unquestionably strong.

Figure 4. Reported CET1 capital ratios as at 30 September 2016

Source: Company Reports

While the overall level of additional capital required remains unknown, the sector awaits the final deliberations of the Basel Committee (global regulator) which is expected to be announced by the end of 2016. APRA are then expected to carefully consider how to apply these deliberations in an Australian context over 2017.

The banks are aware of this and as a result are expected to continue to divest non-core businesses where it makes sense to free up capital to meet future capital requirements.

The return to a simpler banking franchise will also allow bank management to refocus on providing quality banking solutions at a reasonable cost to customers.

Liquidity & funding on track

In September 2016 APRA released the findings from the industry consultation paper on the Net Stable Funding Ratio (NSFR). A ratio of at least 100% is proposed for regulatory purposes from 1 January 2018. All banks reported they have made considerable progress towards satisfying NSFR requirements (i.e. have increased the stability of the funding profile) based upon draft APRA rules.

As a result, the major banks issued (cheap) one year debt in September to ‘tide funding requirements over’. This was a short term fix with the aim of issuing longer-dated (more expensive) debt to maximise the benefit from an NSFR ratio point of view (as debt begins to lose regulatory effectiveness with less than one year to maturity). A secondary reason for doing this was the US money-market fund change that came into effect on 14 October 2016, effectively closing this market to our major banks as a source of funding.

Although Australian banks have ~$90 billion of funding tied to this source they have already begun to prefund 2017 maturities this year.

Figure 5. Estimated weighted average term maturity (WAM) funding profile

Source: Company Reports Conclusion Overall the Australian banking sector remains in good shape from a credit investor’s perspective. Any increase in regulatory capital resulting from the Basel Committee that are endorsed by APRA means the risks between equity investors and credit investors are diverging (improving credit outlook but deteriorating equity outlook). The increased regulatory scrutiny upon bank operations is a long term positive and will help to ensure our banking sector remains stronger throughout the economic cycle.

Source: Company Reports Conclusion Overall the Australian banking sector remains in good shape from a credit investor’s perspective. Any increase in regulatory capital resulting from the Basel Committee that are endorsed by APRA means the risks between equity investors and credit investors are diverging (improving credit outlook but deteriorating equity outlook). The increased regulatory scrutiny upon bank operations is a long term positive and will help to ensure our banking sector remains stronger throughout the economic cycle.