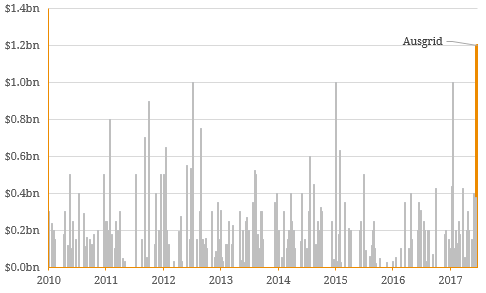

Earlier this week marked the debut of new wholesale bonds from New South Wales electricity distribution company, Ausgrid (previously known as Energy Australia). The transaction raised $1.2 billion over a fixed rate ($750 million) and floating rate tranche ($450 million), and was the largest Australian corporate issuance since Telstra’s $1 billion issuance (three tranches) in April this year. The 7-year securities are structured as senior secured obligations of Ausgrid and were priced at a margin of 1.22% over the bank bill swap rate. This equates to a coupon rate of 3.75% per annum for the fixed rate tranche. The deal follows on from December last year when the New South Wales State Government partially privatised the infrastructure through a partnership with AustralianSuper and IFM Investors. This was structured as a 99-year lease where both parties combined acquired a 50.4% interest in the utility. Figure 1. Corporate Fixed Income Primary Market Transactions  Source: BondAdviser, Bloomberg With ~$12 billion of balance sheet, Ausgrid appears high leveraged on the surface but this must be considered against the sector it operates in. Infrastructure and more specifically, utilities, generally carry high levels of debt due to large periodic, capital expenditures. While there are concerns around funding, cash inflow is typically non-discretionary and linked to long-term fixed payment contracts. For some, and as is the case for Ausgrid, earnings are also underpinned by regulated revenue streams meaning cash flow volatility is minimised and forecasts are largely transparent. Nonetheless, utilities generally refinance maturing debt, which is a risk for Ausgrid, especially in 2022 with a $6 million loan maturity.

Source: BondAdviser, Bloomberg With ~$12 billion of balance sheet, Ausgrid appears high leveraged on the surface but this must be considered against the sector it operates in. Infrastructure and more specifically, utilities, generally carry high levels of debt due to large periodic, capital expenditures. While there are concerns around funding, cash inflow is typically non-discretionary and linked to long-term fixed payment contracts. For some, and as is the case for Ausgrid, earnings are also underpinned by regulated revenue streams meaning cash flow volatility is minimised and forecasts are largely transparent. Nonetheless, utilities generally refinance maturing debt, which is a risk for Ausgrid, especially in 2022 with a $6 million loan maturity.  Source: BondAdviser, Company Reports, Moody’s Despite the natural propensity for leverage, debt securities from infrastructure-related entities such as utilities are typically secured by the underlying assets. These assets play a crucial role in the standard of living for consumers and broader economy, and sometimes even represent a natural monopoly. For this reason, it is generally in the best interest of government authorities to ensure these entities remain financially healthy. This is reflected in instances where governments will sometimes own or partially own (Ausgrid) utility assets. For this and other reasons, the global utility sector has one of the lowest default rates on a historical basis which highlights that relatively high debt levels do not always naturally result in higher probabilities of default. While this is a generalisation and corporate credit still warrants a case-by-case approach when considering investment, it does demonstrate the importance of understanding debt in the context of the underlying operating environment and broader sector. Figure 4. Weighted Average Global Corporate Default Rates (1981-2016)

Source: BondAdviser, Company Reports, Moody’s Despite the natural propensity for leverage, debt securities from infrastructure-related entities such as utilities are typically secured by the underlying assets. These assets play a crucial role in the standard of living for consumers and broader economy, and sometimes even represent a natural monopoly. For this reason, it is generally in the best interest of government authorities to ensure these entities remain financially healthy. This is reflected in instances where governments will sometimes own or partially own (Ausgrid) utility assets. For this and other reasons, the global utility sector has one of the lowest default rates on a historical basis which highlights that relatively high debt levels do not always naturally result in higher probabilities of default. While this is a generalisation and corporate credit still warrants a case-by-case approach when considering investment, it does demonstrate the importance of understanding debt in the context of the underlying operating environment and broader sector. Figure 4. Weighted Average Global Corporate Default Rates (1981-2016)  Source: BondAdviser, S&P

Source: BondAdviser, S&P

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.