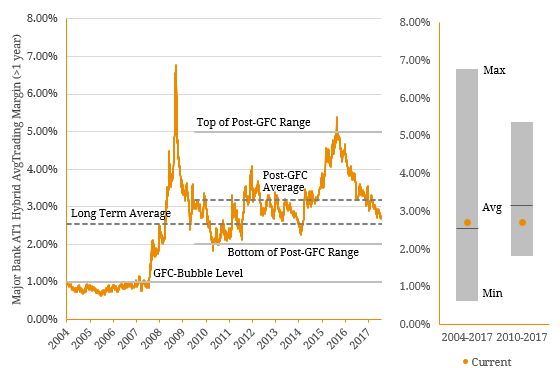

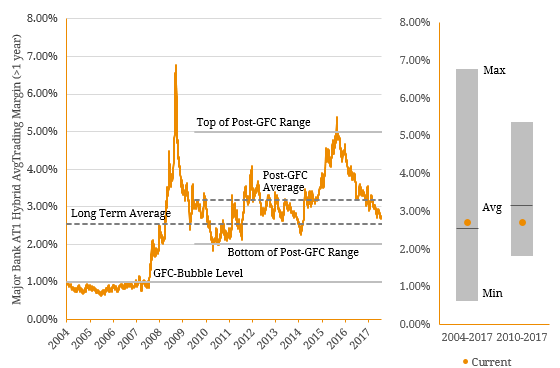

Following a two-year long rally in trading margins, there has been increasing debate around the valuation (expensiveness) of Additional Tier 1 (AT1) hybrids. This notion refers to the true intrinsic value of these instruments which can be highly subjective among investors. There are many lenses that can be used in deciding whether an asset is either trading at fair value, is overvalued or is undervalued and AT1 hybrids are no different. As a result, we outline the following perspectives that investors should consider when assessing the current state of the ASX-listed AT1 hybrid market. 1. Relative to History… Understanding Major Bank AT1 hybrid valuations in the context of both history and future regulatory evolution is a key factor is assessing fair value. Although the market is still in its adolescence relative to other asset classes, it has transformed immensely since ANZ’s inaugural hybrid issue in 1991. The Global Financial Crisis (GFC) exposed the ‘safe haven’ perception of large banks and hybrid margins have never retraced to their pre-GFC levels. If we examine the post-GFC period, current hybrid valuations still appear cheap relative to the immediate GFC rally. However, non-viability trigger event terminology was only introduced in January 2013 and from a structural standpoint, today’s Major Bank AT1 hybrid market is arguably more ‘equity-like’ than ever before (in part reflective of the credit rating notching process). To put this in perspective, in 2014 there was approximately a 50-50% split between Basel III compliant and non-compliant Major Bank AT1 hybrids. This split has now shifted to 90-10% as old-style securities have rolled off. Although the implied premium for non-viability is yet to be accurately quantified academically and is still highly subjective (as seen in the case of failed Spanish Bank Banco Popular), theoretically, it should always be positive. On this basis, there should always be a divide between current margin levels and the post-GFC low (~2.00%) but this gap is evidently waning. Figure 1. Historical Major Bank AT1 Hybrid Average Trading Margin  Source: BondAdviser It is also important to point out that credit margins are generally mean reverting. Although Australia has relatively limited publicly available data to support this, Figure 2 illustrates US trading margins over a 50-year period and the tendency for valuations to trend around an average throughout recurring credit cycles. However, unlike AT1 hybrids, the structural elements of corporate bonds have not differed materially in this time. As a result, the long-term average of AT1 trading margins is arguably unusable for fair value assessment and rather a short-term average should be considered. In doing so, current margins are below the post-GFC mean – further suggesting valuations are becoming increasingly stretched and skewed from a historical viewpoint. Figure 2. Long-Term US Corporate Trading Margins1

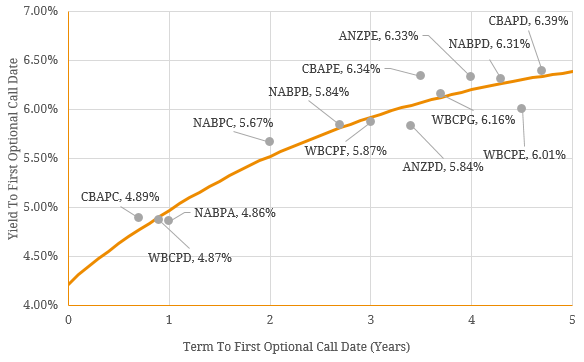

Source: BondAdviser It is also important to point out that credit margins are generally mean reverting. Although Australia has relatively limited publicly available data to support this, Figure 2 illustrates US trading margins over a 50-year period and the tendency for valuations to trend around an average throughout recurring credit cycles. However, unlike AT1 hybrids, the structural elements of corporate bonds have not differed materially in this time. As a result, the long-term average of AT1 trading margins is arguably unusable for fair value assessment and rather a short-term average should be considered. In doing so, current margins are below the post-GFC mean – further suggesting valuations are becoming increasingly stretched and skewed from a historical viewpoint. Figure 2. Long-Term US Corporate Trading Margins1  1Represents Moody’s Baa Corporate Bond Yield Relative to Yield over 10-Year Treasury Constant Maturity Source: BondAdviser, Moody’s. 2. Relative to Geography… In June 2016, ANZ tested the US market with the first AT1 capital instrument issued offshore since 2009. ANZ raised $1 billion from the issue which was met by heightened demand from global investors both in primary and secondary markets. In fact, demand was so strong during the launch that the initial fixed rate pricing estimate of 7.25% tightened 50 bps to 6.75%. Media outlets reported that there was in excess of US$18 billion of bids during the offer period. Westpac became the second major bank to issue a $US Additional Tier 1 (AT1) hybrid raising $US1.25 billion (~$A1.56 billion) in later 2017. The fixed-rate 10-year hybrid was initially guided to price at a coupon of 5.375% p.a. but again strong demand ($US11 billion in initial bids) saw this tighten to 5.00%. In domestic currency terms, this translated to a margin of ~3.28% p.a. Figure 3. Domestic Major Bank AT1 Credit Curve versus Offshore AT1 instruments at time of Westpac USD Issuance

1Represents Moody’s Baa Corporate Bond Yield Relative to Yield over 10-Year Treasury Constant Maturity Source: BondAdviser, Moody’s. 2. Relative to Geography… In June 2016, ANZ tested the US market with the first AT1 capital instrument issued offshore since 2009. ANZ raised $1 billion from the issue which was met by heightened demand from global investors both in primary and secondary markets. In fact, demand was so strong during the launch that the initial fixed rate pricing estimate of 7.25% tightened 50 bps to 6.75%. Media outlets reported that there was in excess of US$18 billion of bids during the offer period. Westpac became the second major bank to issue a $US Additional Tier 1 (AT1) hybrid raising $US1.25 billion (~$A1.56 billion) in later 2017. The fixed-rate 10-year hybrid was initially guided to price at a coupon of 5.375% p.a. but again strong demand ($US11 billion in initial bids) saw this tighten to 5.00%. In domestic currency terms, this translated to a margin of ~3.28% p.a. Figure 3. Domestic Major Bank AT1 Credit Curve versus Offshore AT1 instruments at time of Westpac USD Issuance  Source: BondAdviser, Bloomberg On a global scale, the Australian regulatory framework is perceived as highly robust relative its Asian and European peers. As a result, foreign investors are extremely receptive to debt and hybrid securities from Australian banks which results in an attractive funding alternative for the majors. Consequently, the tight valuations of these long-tenor offshore securities shine an attractive light on the domestic AT1 market providing a positive argument for current ASX-listed AT1 valuations. However, we concede there are some structural differences between the offshore and onshore AT1 instruments (i.e. fixed rate, franked coupons). Given that pre-Basel III Tier 1 hybrid securities were well received by global markets prior the Global Financial Crisis (GFC), we could see this comfort re-emerge as the regulatory landscape matures (and in some sense, it already has). This will likely be in the best interests of APRA as it allows foreign investors to also bear the burden of a non-viability scenario, ultimately decreasing the likelihood of a tax-payer bail-out and lessening the impact of a capital bail-in for Australian investors. Figure 4. Major Bank AT1 Issuance by Currency Denomination

Source: BondAdviser, Bloomberg On a global scale, the Australian regulatory framework is perceived as highly robust relative its Asian and European peers. As a result, foreign investors are extremely receptive to debt and hybrid securities from Australian banks which results in an attractive funding alternative for the majors. Consequently, the tight valuations of these long-tenor offshore securities shine an attractive light on the domestic AT1 market providing a positive argument for current ASX-listed AT1 valuations. However, we concede there are some structural differences between the offshore and onshore AT1 instruments (i.e. fixed rate, franked coupons). Given that pre-Basel III Tier 1 hybrid securities were well received by global markets prior the Global Financial Crisis (GFC), we could see this comfort re-emerge as the regulatory landscape matures (and in some sense, it already has). This will likely be in the best interests of APRA as it allows foreign investors to also bear the burden of a non-viability scenario, ultimately decreasing the likelihood of a tax-payer bail-out and lessening the impact of a capital bail-in for Australian investors. Figure 4. Major Bank AT1 Issuance by Currency Denomination  Source: BondAdviser 3. Relative to Fundamentals… In a tight margin and arguably overvalued environment, fundamental factors are becoming increasingly important. Despite a string of Australian banks being downgraded by both S&P and Moody’s, trading margins have marched lower amidst the global search for yield for the most part of 2017. With margins approaching established lows, do valuations truly reflect the current fundamental risk profiles of issuers? Although Australia was arguably insulated from the full impact of the GFC, financial data from 2007 shows Australian banks at the end of the last credit cycle. We are probably nearing the end of the current credit cycle but there has been a vast transformation of the economic climate over the past decade. However, based on 2017 financial results, the credit profiles of Australian banks are undeniably stronger than just before the onset of the GFC. For this reason, we believe banks in general are in a broadly sound position to combat the most adverse fundamental scenarios. For AT1 hybrid holders, the revolution of global banking regulation has resulted in a substantial improvement in the the capital adequacy of the banks. Tier 1 and Total Capital ratios have risen by ~5.6% and ~4.4% of Risk-Weighted Assets (RWA) respectively. We acknowledge we are comparing Basel III and Basel II frameworks with the former using the new Common Equity Tier 1 (CET1) Capital Ratio from 2012/13 – further (optically) supporting the improvement in credit quality for the Australian banking system. With this in mind, current valuations appear relatively cheap if we solely consider the underlying credit quality of banks. Figure 5. 10-Year Change in Capital Adequacy of Major Banks and Historical CET1 Capital Accumulation

Source: BondAdviser 3. Relative to Fundamentals… In a tight margin and arguably overvalued environment, fundamental factors are becoming increasingly important. Despite a string of Australian banks being downgraded by both S&P and Moody’s, trading margins have marched lower amidst the global search for yield for the most part of 2017. With margins approaching established lows, do valuations truly reflect the current fundamental risk profiles of issuers? Although Australia was arguably insulated from the full impact of the GFC, financial data from 2007 shows Australian banks at the end of the last credit cycle. We are probably nearing the end of the current credit cycle but there has been a vast transformation of the economic climate over the past decade. However, based on 2017 financial results, the credit profiles of Australian banks are undeniably stronger than just before the onset of the GFC. For this reason, we believe banks in general are in a broadly sound position to combat the most adverse fundamental scenarios. For AT1 hybrid holders, the revolution of global banking regulation has resulted in a substantial improvement in the the capital adequacy of the banks. Tier 1 and Total Capital ratios have risen by ~5.6% and ~4.4% of Risk-Weighted Assets (RWA) respectively. We acknowledge we are comparing Basel III and Basel II frameworks with the former using the new Common Equity Tier 1 (CET1) Capital Ratio from 2012/13 – further (optically) supporting the improvement in credit quality for the Australian banking system. With this in mind, current valuations appear relatively cheap if we solely consider the underlying credit quality of banks. Figure 5. 10-Year Change in Capital Adequacy of Major Banks and Historical CET1 Capital Accumulation  Source: BondAdviser, Company Reports 4. Relative to the Capital Structure… Lastly, another factor for consideration is relative trading margins across the capital structure. For the major banks, we illustrate the 5-year point for AT1, T2 and Senior Floating Rate Notes (FRNs) since the introduction of Basel III (2013). Assuming margins are normally distributed and mean reverting (an imperfect but reasonable assumption as we showed previously), our analysis suggests T2 is the most stretched instrument class from a valuation perspective. This could suggest that AT1 margins could still continue to grind tighter (i.e. capital upside) on a relative basis given the historical correlation of major bank instruments (i.e. they tend to move in the same direction over time). However, we note this analysis was conducted with a small sample of adolescent Basel III instruments. Figure 6. Post Basel-III Major Bank Trading Margins Across the Capital Structure

Source: BondAdviser, Company Reports 4. Relative to the Capital Structure… Lastly, another factor for consideration is relative trading margins across the capital structure. For the major banks, we illustrate the 5-year point for AT1, T2 and Senior Floating Rate Notes (FRNs) since the introduction of Basel III (2013). Assuming margins are normally distributed and mean reverting (an imperfect but reasonable assumption as we showed previously), our analysis suggests T2 is the most stretched instrument class from a valuation perspective. This could suggest that AT1 margins could still continue to grind tighter (i.e. capital upside) on a relative basis given the historical correlation of major bank instruments (i.e. they tend to move in the same direction over time). However, we note this analysis was conducted with a small sample of adolescent Basel III instruments. Figure 6. Post Basel-III Major Bank Trading Margins Across the Capital Structure  Source: BondAdviser, Bloomberg Overall, our analysis shows that there are many different perspectives in deciding the fair value of a particular security or asset class and all factors should be taken into consideration. For AT1 hybrid instruments, there are arguments for overvaluation and undervaluation and it is a really up to the interpretation of the investors. For this reason, an estimate of true intrinsic value is subjective with various evidence leading to inconclusive results as demonstrated. While we have not disclosed our views around current valuations in this article, we continuously monitor key themes and trends identified with other factors in making investment recommendations and this should form the basis for credit analysis in all fixed income segments.

Source: BondAdviser, Bloomberg Overall, our analysis shows that there are many different perspectives in deciding the fair value of a particular security or asset class and all factors should be taken into consideration. For AT1 hybrid instruments, there are arguments for overvaluation and undervaluation and it is a really up to the interpretation of the investors. For this reason, an estimate of true intrinsic value is subjective with various evidence leading to inconclusive results as demonstrated. While we have not disclosed our views around current valuations in this article, we continuously monitor key themes and trends identified with other factors in making investment recommendations and this should form the basis for credit analysis in all fixed income segments.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.