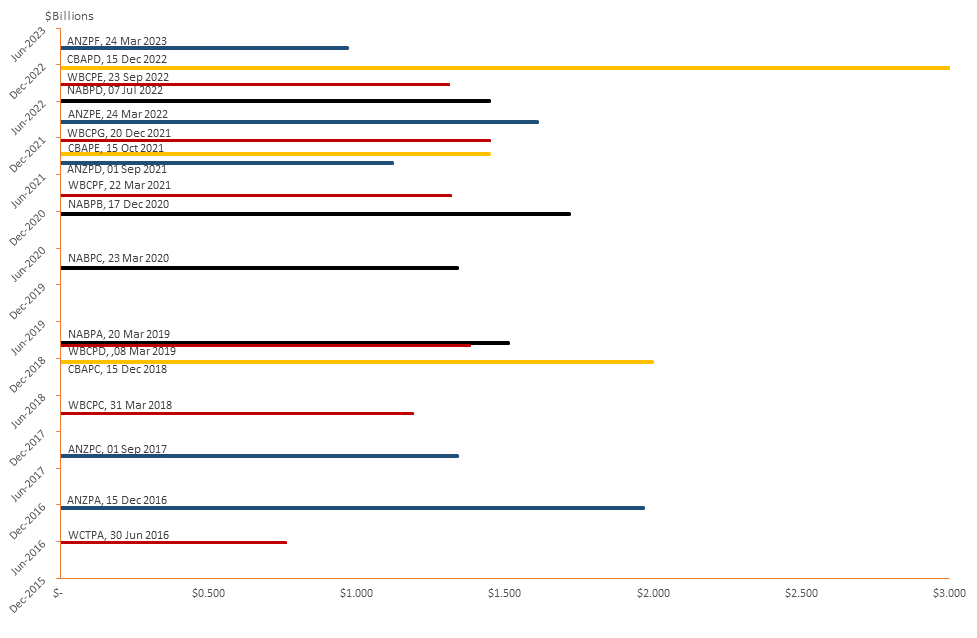

With the successful closure of the second major bank Tier 1 hybrid book build of 2016, now is a good time revisit why these securities are issued and look at how these securities dominate the overall ASX listed interest rate securities universe. Generally speaking, the banks, insurance and diversified financial sector issue these securities to satisfy regulatory capital requirements (Figure 1 shows that Tier 1 & 2 regulated capital make up 82.4% of all issuance). The other sectors (See Figure 2) do so mainly as: • A source of funding, that is usually designed to support senior debt investors; and • To gain some equity credit from the rating agencies and thereby enhance their credit rating profile. Figure 1. ASX listed interest rate securities capital structure positioning Source: BondAdviser It is therefore not surprising when looking at total issuance on a sector basis, using the Global Industry Classification Standard (GICS), that the banks (including the non-majors) represent 72.6% of total issuance with the insurance sector a distant second with 8.3% of issuance as Figure 2 shows. Figure 2. ASX Listed Interest Rate Securities – Issuer Sector Breakdown by Market Cap Source: BondAdviser When they were first issued the current WCTPA, ANZPA, ANZPC & WBCPC hybrids did qualify as Tier 1 regulatory capital for the banks. However, these securities no longer met Basel III eligibility criteria when the regulator APRA introduced new rules that became effective on 1st January 2013. As a result these four securities have been in a regulatory value transition phase since that date and are in the process of being called at their first optional call dates to be gradually replaced with securities that are Basel III compliant, i.e. they contain the loss absorbing terms and conditions known in the documentation as Capital and Non-Viability Trigger Events. The first truly Basel III eligible Tier 1 hybrid issued was the CBA’s PERLS VI hybrid (ASX Code: CBAPC) that was issued on 18th October 2012 ($2 billion) ahead of the new rules coming into effect. Since this first issue the segment has grown to represent just over $20 billion of issuance and is expected to grow further as evidenced by recent issuance (See Figure 3). Figure 3. Basel III Major Bank Tier 1 Hybrid Issuance Source: BondAdviser Finally, while there are approximately 60 securities currently listed on the ASX, the top ten transactions represent over 82% of all issuance (based upon current market capitalisation), with the four major Australian banks making up 67.8% when including the recent Westpac Capital Notes 4 issue as Figure 4 shows. The total market capitalisation of these securities is currently over $46 billion. Figure 4. Top Ten ASX Listed Interest Rate Security Issuers (82.34% of total issuance) Source: BondAdviser So where to from here? With both the CBA & Westpac having successfully issued Tier 1 hybrids, we are expecting the ANZ to issue into this market between now and closer to the first optional conversion date of the ANZ Convertible Preference Shares 2 (ASX Code: ANZPA) on the 15th of December 2016. Whilst an article in the Australian Financial Review on the 13th of May 2016 speculated that the CBA was looking a launching another PERLS hybrid issue, we believe that this is not the case and it is more likely that the CBA will look to issue a Tier 2 (or subordinated bond issue) to the wholesale market during the second half of 2016. However, when looking at the banks’ 2016 half year results announcements during early May, we do note that the NAB stated in the ASX Announcements that: “As part of NAB’s ongoing commitment to maintaining a strong and efficient capital position, NAB is considering issuance of a new ASX listed Additional Tier 1 capital security, subject to market conditions, including any competing supply.” We believe that the market would be supportive of a NAB issue should they decide to do so shortly after Westpac closed their book build. The Westpac issue was over 2.5x oversubscribed as investors continue to seek yield in a low interest rate environment. To date, this is also supported by the fact that the average trading margin for major bank Tier 1 hybrids have not widened significantly since the Westpac transaction was announced on the 17th of May as shown in Figure 5. Figure 5. Major Bank Tier 1 Hybrid (With a first optional call date between 5-7 years) Average Trading Margin Source: BondAdviser We also note that there is only one Tier 1 hybrid with a first optional call date during 2017, that being the ANZ Convertible Preference Shares 3 (ASX Code: ANZPC). This lends further support that supply to this market may be more limited going forward (See Figure 6). Figure 6. Major Bank Tier 1 Hybrids, First Optional Call Dates  Source: BondAdviser

Source: BondAdviser

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.