Credit Performance…

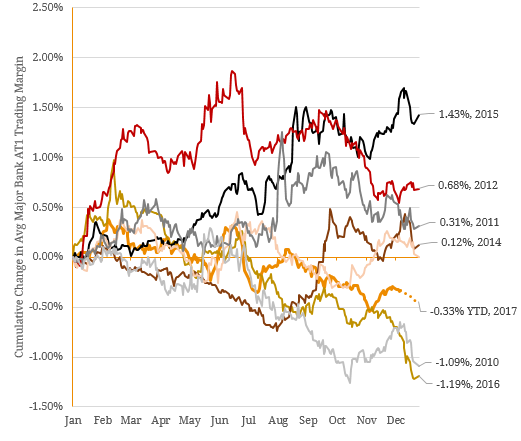

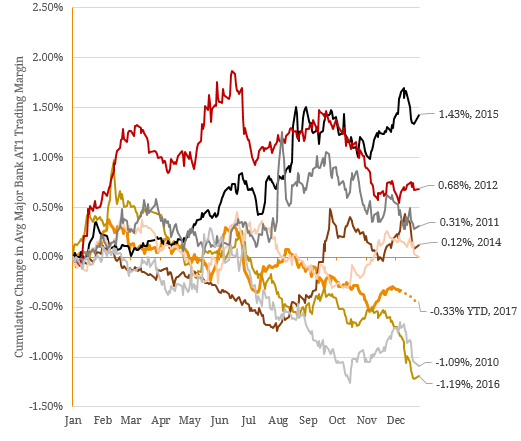

2017 has been another strong year for the ASX-Listed Debt & Hybrid market with accommodative issuer fundamentals and strong market technical factors (demand and supply). Consequently, trading margins across most securities have marched lower, which has extended the almost 2-year tightening cycle since the last severe sell-off in February 2016. As a result (figure 1), 2017 has been the third-best calendar year in terms of major bank margin compression since the Global Financial Crisis, behind 2010 (which encompassed the second leg of the post-GFC rally) and 2016 (which benefited from the above sell-off’s retracement). Figure 1. Cumulative Change in Average Major Bank Trading Margin by year post GFC  Source: BondAdviser In terms of the listed AT1 Hybrid market, which comprises 80% of ASX-Listed Debt & Hybrid universe, longer-dated securities outperformed as the credit curve flattened amidst strong primary market demand (weighted average term of new issuance was ~6 years). This resulted in the strongest compression in the 7-year curve point, which declined 56 bps over the year. With regards to dispersion, the standard deviation of trading margins in relation to the relevant credit curve declined by 11 bps, highlighting the more challenging environment to identify mispricing opportunities and to capitalise accordingly (figures 2 and 3). Figure 2. Listed AT1 Hybrid Curve Beginning of the Year to Now

Source: BondAdviser In terms of the listed AT1 Hybrid market, which comprises 80% of ASX-Listed Debt & Hybrid universe, longer-dated securities outperformed as the credit curve flattened amidst strong primary market demand (weighted average term of new issuance was ~6 years). This resulted in the strongest compression in the 7-year curve point, which declined 56 bps over the year. With regards to dispersion, the standard deviation of trading margins in relation to the relevant credit curve declined by 11 bps, highlighting the more challenging environment to identify mispricing opportunities and to capitalise accordingly (figures 2 and 3). Figure 2. Listed AT1 Hybrid Curve Beginning of the Year to Now  Source: BondAdviser Figure 3. Change in AT1 Hybrid Trading Margins by Term

Source: BondAdviser Figure 3. Change in AT1 Hybrid Trading Margins by Term  Source: BondAdviser

Source: BondAdviser

Technicals…

In late November, the Bank of Queensland (BOQ) completed the late-year surge in regional bank issuance by launching what is most likely the last Additional Tier 1 (AT1) hybrid for 2017. Like its peers (Bendigo Bank and Suncorp), the bank is in an adequate capital position and gave an indicative offer size of $325 million – $25 million higher than the maturing BOQ Convertible Preference Shares (ASX: BOQPD) in April 2018. For the above ‘outsize’ reason, it is likely the transaction will mostly facilitate reinvestments only, with limited scope for new investors. Assuming that the final issue size of the BOQ Capital Notes (ASX: BOQPE) remains at $325 million, 2017 will be the first calendar year that the ASX-listed Debt & Hybrid market has been in an aggregate net redemption state since the Global Financial Crisis (GFC), with ~$4.6 billion less in market supply (figure 4). Figure 4. ASX-Listed Debt & Hybrid Market Net Supply by Year.  Source: BondAdviser In light of already robust capital positions for issuers and the likelihood of a reinvestment offer solely for existing hybrid holders, investors begun purchasing soon-to-mature securities at negative margins (i.e. a premium to par value) to ensure portfolios receive new allocations in the reinvestment offer and effectively ‘jump the cue’. This effect can be best illustrated by the price action of the Bendigo Convertible Preference Shares (ASX Code: BENPD) before and after the launch of the recent Bendigo Converting Preference Shares 4 (ASX: BENPG) in Figure 5 below. Figure 5. BENPD Capital Price relative to days before and after BENPG Launch

Source: BondAdviser In light of already robust capital positions for issuers and the likelihood of a reinvestment offer solely for existing hybrid holders, investors begun purchasing soon-to-mature securities at negative margins (i.e. a premium to par value) to ensure portfolios receive new allocations in the reinvestment offer and effectively ‘jump the cue’. This effect can be best illustrated by the price action of the Bendigo Convertible Preference Shares (ASX Code: BENPD) before and after the launch of the recent Bendigo Converting Preference Shares 4 (ASX: BENPG) in Figure 5 below. Figure 5. BENPD Capital Price relative to days before and after BENPG Launch  Despite this, the evident strong technical environment made primary market participation a winning strategy in 2017 with every new issue met with heightened oversubscriptions. This was further reflected with each 2017 new issue tightening by ~30 bps and appreciating by ~$1.44 in price (on average) following the first day of trading on the ASX (figure 6). Given the outlook for limited supply, we expect this theme to persist in the near term. Figure 6. Change in Price and Margin following first day of trading for AT1 Hybrid 2017 Issuance

Despite this, the evident strong technical environment made primary market participation a winning strategy in 2017 with every new issue met with heightened oversubscriptions. This was further reflected with each 2017 new issue tightening by ~30 bps and appreciating by ~$1.44 in price (on average) following the first day of trading on the ASX (figure 6). Given the outlook for limited supply, we expect this theme to persist in the near term. Figure 6. Change in Price and Margin following first day of trading for AT1 Hybrid 2017 Issuance  Source: BondAdviser

Source: BondAdviser

Fundamentals…

Our view on fundamentals for 2017 stems from the idea that the top-down macroeconomic climate continues to diverge from the bottom-up condition of Australian financial institutions. Specifically, Australian banks have continued to produce steady earnings growth, meet capital requirements set out by APRA and achieve robust asset quality despite rising risks in the economic environment. We concede that this threat, largely encompassed in the residential housing market represents a tail-risk but one that cannot be discounted in the current benign conditions. Figure 7 below shows the current state of Australian household leverage versus banks’ asset quality. Figure 7. Household Leverage vs Australian Banking System Asset Quality  Source: BondAdviser, RBA, APRA Nonetheless, from a bottom-up perspective, it was broadly difficult to fault Australian banks and insurers in the latest reporting season. Lower provisioning is persistent, asset quality remains strong and banks are still accreting capital. As a result, participants are meeting every new item on APRA’s checklist and achieving steady earnings growth in the background. Compliance remains a contentious issue in equity markets and has been the most prominent theme of late but the end outcome will likely have a limited impact from a credit perspective. For insurers, revenue remains steady and reinsurance programs are solid to combat most catastrophe events. This was additionally noted by the broadly positive results from APRA’s recent stress test of the general insurance sector (figure 8). Figure 8. Australian Bank CET1 Capital Ratios

Source: BondAdviser, RBA, APRA Nonetheless, from a bottom-up perspective, it was broadly difficult to fault Australian banks and insurers in the latest reporting season. Lower provisioning is persistent, asset quality remains strong and banks are still accreting capital. As a result, participants are meeting every new item on APRA’s checklist and achieving steady earnings growth in the background. Compliance remains a contentious issue in equity markets and has been the most prominent theme of late but the end outcome will likely have a limited impact from a credit perspective. For insurers, revenue remains steady and reinsurance programs are solid to combat most catastrophe events. This was additionally noted by the broadly positive results from APRA’s recent stress test of the general insurance sector (figure 8). Figure 8. Australian Bank CET1 Capital Ratios  Source: BondAdviser, APRA

Source: BondAdviser, APRA

Market Reaction…

If we look to what the market is saying, investors were rightly indifferent to credit rating agencies and their downgrades as concerns have been brushed aside amidst strong technicals. Despite the downgrades, trading margins have continued to grind tighter, reflecting the present benign fundamental backdrop. Arguably a more pertinent driver of trading margins was the bail-in of Spanish Bank, Banco Popular which, in our opinion, was the main reason for the notable sell-off in June 2017. This was following in July by commentary from outgoing ASIC chairman, Greg Medcraft who condemned hybrid allocations in retail portfolios having of course previously condoned such compositions in his many years of public office. AT1 hybrid securities sold off in both cases (figure 9), which suggests investors remain cautious and responsive to ‘shocks’. However, as we expected, redemptions in the second half of 2017 provided sufficient protection against any significant market selloff. For this reason, the current demand and supply imbalance will continue to drive price action over currently benign economic factors. Figure 9. 2017 Major Bank AT1 Avg Trading Margin with Major 2017 Fundamental Drivers  Source: BondAdviser

Source: BondAdviser

Outlook…

Optically, supply conditions will remain soft in 2018. From trends established this year, Tier 2 capital instruments and corporate securities are unlikely to be refinanced in the listed market and account for ~42% of maturities next year. As a result, ~$2.9 billion of additional issuance will be required for the market to end the year supply neutral. This is by no means unachievable given the average size of a major bank Basel-III AT1 hybrid is ~$1.5 billion, but would likely require one or more of the majors to locally issue a new instrument, which is not linked to refinancing / reinvestment. The last listed security of this nature was the ~$1.5 billion NAB Capital Notes (ASX: NABPD) issued in June 2016 but we note since then both ANZ and Westpac have issued AT1 capital instruments into the US market. As a result, CBA and NAB may follow suit, which would further dampen supply prospects. Either way, we believe a significant shift in the current regulatory landscape would be required to give the banks an incentive to issue new instruments. Nonetheless, this shortfall ($2.9 billion) is ~40% lower than what will be experienced in 2017 ($4.6 billion), which suggests the technical environment may weaken slightly moving forward. This could equate to slower margin compression or even a sideways trend. In terms of fundamentals, we believe the risk profile is broadly balanced between strengthening capital positions and the present threat to asset quality from a top-down perspective. We believe the risk of systemic shock to be moderate for the foreseeable future and any downside risk to current valuations to remain protected by rampant demand and our expectation of limited supply in 2018.