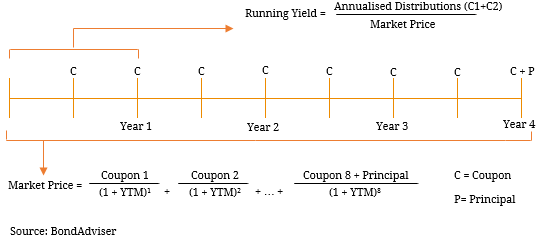

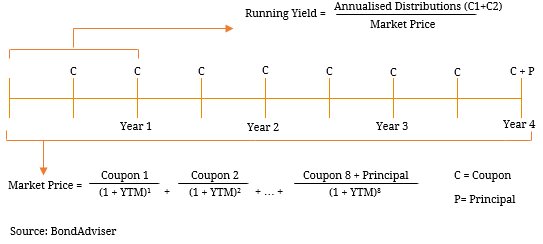

When describing yield, investors typically use two measures: the running yield and the yield-to-maturity (yield-to-call). Running yield is calculated by dividing a security’s most recent distribution by its capital price. On the other hand, yield-to-maturity (call) is determined by taking into account all future cashflows such as the present value of all coupon payments and the discount or premium paid on purchase or received at maturity. As a result, the yield-to-maturity (call) is the more accurate measure of a security’s return. Figure 1. Running Yield Vs Yield-to-Maturity (Call).  As illustrated above, the yield-to-maturity (call) is calculated by computing the discount rate that equates all cashflows to the current market price. This is known as the time value of money and is essentially the process of earning interest in reverse. For example, if you were to earn 10% interest on $100, you would receive $110 at the end of the investment period and your return would be 10%. From this you can work backwards to find the present value (i.e. $110/(1+interest rate)) of the investment (which is what you begun with, $100). Therefore, the future value is $110, the present value is $100 and the interest rate that allows you to move between these values is 10%. Although this a simplified example, it demonstrates the same though-process behind the yield-to-maturity (call). The cashflows earnt from a security are discounted back to their present value (which is the market price investors are willing to pay) by the rate of return. This rate of return is the yield-to-maturity (call) and is commonly used as a comparison tool in the security selection process. For the rest of the series, we will refer to the yield-to-maturity (call) as the ‘yield’.

As illustrated above, the yield-to-maturity (call) is calculated by computing the discount rate that equates all cashflows to the current market price. This is known as the time value of money and is essentially the process of earning interest in reverse. For example, if you were to earn 10% interest on $100, you would receive $110 at the end of the investment period and your return would be 10%. From this you can work backwards to find the present value (i.e. $110/(1+interest rate)) of the investment (which is what you begun with, $100). Therefore, the future value is $110, the present value is $100 and the interest rate that allows you to move between these values is 10%. Although this a simplified example, it demonstrates the same though-process behind the yield-to-maturity (call). The cashflows earnt from a security are discounted back to their present value (which is the market price investors are willing to pay) by the rate of return. This rate of return is the yield-to-maturity (call) and is commonly used as a comparison tool in the security selection process. For the rest of the series, we will refer to the yield-to-maturity (call) as the ‘yield’.

An employee-owned financial services provider focused on the Debt Capital Markets.

© Bond Adviser Pty Ltd ‧ ASFL 456783 ‧ ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

© Bond Adviser Pty Ltd ‧ ASFL 456783

ABN 31 164 148 467 ‧ Important Information

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.