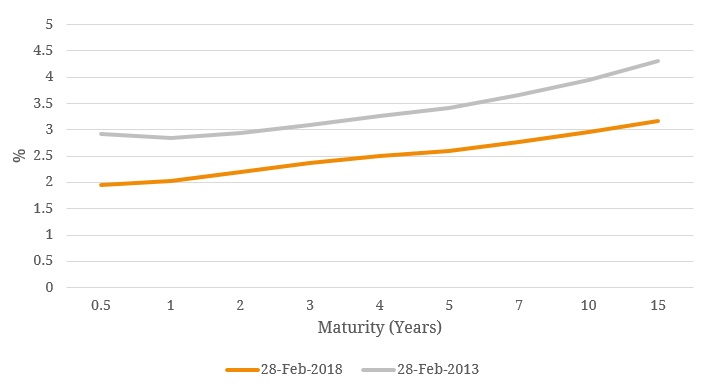

The term structure of interest rates is the relationship between interest rates or bond yields and different terms or maturities, which is also commonly known as the yield curve (Figure 1). The term structure of interest rates is the single most important benchmark in the fixed income world, central to all debt securities and plays a vital role in the economy. In essence, the term structure reflects market participants’ collective expectations about future changes in interest rates, inflation and their assessment of monetary policy conditions. In other words, it has been argued that long-term interest rates are determined, at least in part, by current and future expected short-term rates (known as forward rates), in such a way that investors are indifferent between investing in long term bonds and investing in a sequence of short-term bonds, since the options return the same for the investor. Figure 1: Australian Term Structure  Source: BondAdviser, Bloomberg Apart from investor expectations, term risk premia, which compensates investors for deferring consumption today also influences the term structure of interest rates. A change in yields could reflect changes in term risk expectations or due to the changes in future uncertainty of inflation (which impacts purchasing power). This makes the modelling and interpretation of the term structure of interest rates more difficult. Moreover, prices of coupon-bearing or zero-coupon bonds, inter-bank interest rates, index-linked bonds, together with derivatives such as options or futures on these instruments, all provide clues about the term structure, so it’s not surprising that there are many different models of the term structure of interest rates. Generally speaking, one would prefer a model that is flexible, simple, well-specified, realistic and a good fit to data. One of the models that could separate the risk premia from the “pure” expectations component, whilst still retain the general attributes of good modelling, is the “Affine Term Structure Model (ATSM)”, which has been widely used by policymakers and academics in a broad range of countries. This includes the Reserve Bank of Australia, who recently applied the ATSM model to domestic data and found that:

Source: BondAdviser, Bloomberg Apart from investor expectations, term risk premia, which compensates investors for deferring consumption today also influences the term structure of interest rates. A change in yields could reflect changes in term risk expectations or due to the changes in future uncertainty of inflation (which impacts purchasing power). This makes the modelling and interpretation of the term structure of interest rates more difficult. Moreover, prices of coupon-bearing or zero-coupon bonds, inter-bank interest rates, index-linked bonds, together with derivatives such as options or futures on these instruments, all provide clues about the term structure, so it’s not surprising that there are many different models of the term structure of interest rates. Generally speaking, one would prefer a model that is flexible, simple, well-specified, realistic and a good fit to data. One of the models that could separate the risk premia from the “pure” expectations component, whilst still retain the general attributes of good modelling, is the “Affine Term Structure Model (ATSM)”, which has been widely used by policymakers and academics in a broad range of countries. This includes the Reserve Bank of Australia, who recently applied the ATSM model to domestic data and found that:

- While expectations for future short-term nominal, real and inflation rates vary over time, changes in risk premia tend to have a greater influence than changes in expectations on movements in observed yields, at least over short time horizons. This emphasises the importance of not taking changes in observed yields at face value when trying to infer market expectations.

- Medium- to -long-term expectations for real interest rates, have declined in recent years.

- Long-term inflation expectations have fallen over the 1990s as the RBA’s inflation-targeting framework gained credibility, and have remained reasonably stable within the RBA’s 2% – 3% target band.

- A large portion of the decline in yields on Australian government securities (AGS) (Figure 1) since the global financial crisis has reflected lower real term premia, rather than declines in inflation expectations. The decline may reflect overseas factors such as the US quantitative easing programs and associated portfolio rebalancing flows, given it has coincided with declines in US term premia.

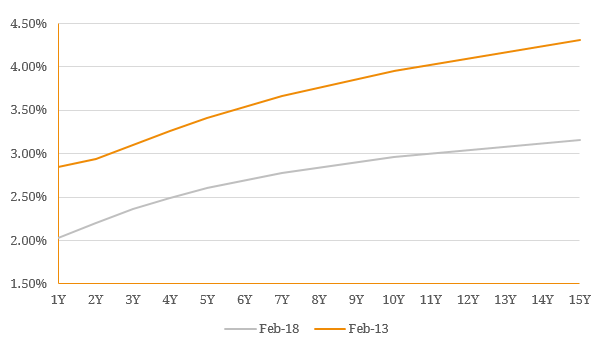

Figure 2. US, Australian Term Structures  Source: BondAdviser, Bloomberg As the US Federal Reserve and other global central banks reduce their balance sheets and reverse their quantitative easing programs, we could in turn see a reverse of the model’s findings – a return to the driver’s seat of the “pure” expectations component of the term premia.

Source: BondAdviser, Bloomberg As the US Federal Reserve and other global central banks reduce their balance sheets and reverse their quantitative easing programs, we could in turn see a reverse of the model’s findings – a return to the driver’s seat of the “pure” expectations component of the term premia.